FEMA Announces Reforms to National Flood Insurance Program

May 24, 2016

Share

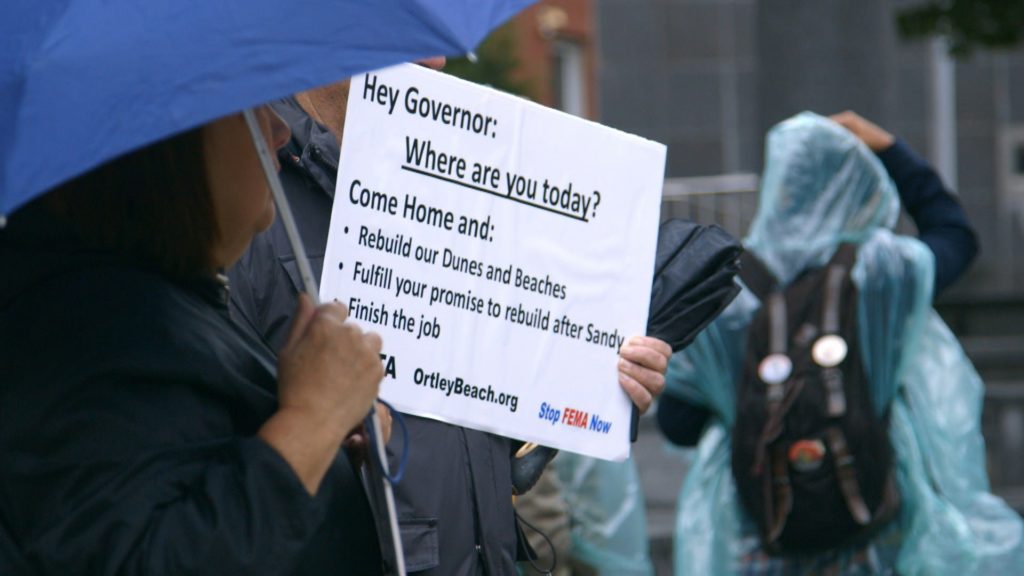

The Federal Emergency Management Agency announced changes to the nation’s flood insurance program on Monday, responding to complaints from Superstorm Sandy survivors that the private insurers participating in the federally-backed program underpaid their claims and dragged out lawsuits.

As FRONTLINE and NPR investigate in the new documentary Business of Disaster, thousands of homeowners affected by Sandy are still not home after the storm devastated stretches of New Jersey and New York in 2012. In the wake of the disaster, insurance companies in the program faced allegations that they systematically underpaid thousands of homeowners on their flood insurance claims.

The proposed changes are meant to provide FEMA with more oversight over the insurance companies that handle the claims of homeowners through the flood program. This would happen through a restructuring of what’s known as “the arrangement” between the government and insurers. The aim is to make it easier for FEMA to renegotiate contracts with the 79 firms participating in the program.

“This will help,” said Amy Bach, executive director of the consumer advocacy group United Policyholders. “But it’s not going to be a solution as long as you’ve got this public-private hybrid with a lot of private executives having a say in how it’s run.”

FEMA will also roll out changes to the appeals process over the next several months, which will allow any homeowner who is disputing a flood insurance claims to see the files, the analysis and how a decision was reached on their claim. Anyone in the appeals process will also be given a contact at FEMA — whereas before insurance companies were the ones communicating directly with policyholders.

“Before these changes were made, frankly, the process was too opaque and not clear to the survivors we work for,” said Rafael LeMaitre, a FEMA spokesman. The changes will give “policyholders who do appeal a fair shake, and they’ll have full visibility on how the process is working to adjudicate their claim.”

Bach said, “The fact that they’re publicly admitting that they didn’t really have a good [appeals process], and they’re working to set something up is a step in the right direction.”

FEMA also announced the creation of a team in the Office of Chief Counsel to monitor lawsuits in an effort to reduce litigation costs. Currently, the taxpayer — through FEMA — foots the bill for insurance companies when homeowners sue to recover their claims.

“On occasion, a claim will not be formally resolved until after litigation and FEMA is committed to ensuring the litigation process for our policyholders is respectful, reasonable, and transparent,” Roy Wright, deputy associate administrator for insurance and mitigation at FEMA, said in a memo detailing the plans.

Last Friday, FEMA also revised its guidelines to allow Sandy survivors who were facing financial difficulties to receive the part of their claim that wasn’t disputed while they pursued appeals.

“By withholding payments for undisputed claims amounts for those who felt they deserved more, FEMA discouraged those struggling to rebuild their lives from appealing,” said Sen. Robert Menendez, D-N.J., in a statement. “I am pleased that FEMA has fixed this injustice and I will continue to hold their feet to the fire until every Sandy survivor recovers.”

As for the reforms to the claims appeals process, Bach said, “I’m inclined to say let’s give them the benefit of the doubt that they’ve heard loud and clear what the problems are with the program and this is their attempt to use the tools they have available at their disposal to be responsive to those complaints.”

Digital Editor, FRONTLINE

Related Documentaries

Latest Documentaries

Related Stories

Business of Disaster

Related Stories

Business of Disaster

Explore

Policies

Teacher Center

![]()

Jon and Jo Ann Hagler on behalf of the Jon L. Hagler Foundation

Koo and Patricia Yuen

FRONTLINE is a registered trademark of WGBH Educational Foundation. Web Site Copyright ©1995-2025 WGBH Educational Foundation. PBS is a 501(c)(3) not-for-profit organization.

Funding for FRONTLINE is provided through the support of PBS viewers and by the Corporation for Public Broadcasting, with major support from Ford Foundation. Additional funding is provided the Abrams Foundation, Park Foundation, John D. and Catherine T. MacArthur Foundation, Heising-Simons Foundation, and the FRONTLINE Trust, with major support from Jon and Jo Ann Hagler on behalf of the Jon L. Hagler Foundation, and additional support from Koo and Patricia Yuen. FRONTLINE is a registered trademark of WGBH Educational Foundation. Web Site Copyright ©1995-2025 WGBH Educational Foundation. PBS is a 501(c)(3) not-for-profit organization.