Money, Power and Wall Street

April 24, 2012

59m

In a special investigation, FRONTLINE goes inside the struggles to rescue and repair a shattered economy

Money, Power and Wall Street

Part One

April 24, 2012

59m

NOW PLAYING

Part Two

April 24, 2012

54m

Part Three

May 1, 2012

57m

Part Four

May 1, 2012

56m

Share

In the special four-hour investigation, Money, Power and Wall Street, FRONTLINE tells the inside story of the struggles to rescue and repair a shattered economy, exploring key decisions, missed opportunities, and the unprecedented and uneasy partnership between government leaders and titans of finance that affects the fortunes of millions of people around the world.

In partnership with:

Transcript

Credits

Journalistic Standards

Support provided by:

Learn More

Most Watched

The FRONTLINE Newsletter

Related Stories

S.&P. to Pay $1.38 Billion for Once Rave Ratings of Toxic Mortgages

Pioneer Behind Credit Derivatives is Leaving JPMorgan

The Financial Crisis Five Years Later — How It Changed Us

JPMorgan To Lose $842 Million In Toxic Ala. Sewer Deal

Financial Regulators Turn Their Focus To Non-Banks

U.S. Sues Bank of America for $1 Billion Over Mortgage Sales

New Mortgage Task Force Charges JPMorgan With “Systemic Fraud”

Deadlines Loom To Bring Financial Crisis Cases

Neil Barofsky on the “Broken Promises” of the Bank Bailouts

The State of Reform: Dodd-Frank at Two Years Old

Do Credit Ratings Still Matter?

Trouble At UBS For Obama’s Favorite Banker?

Home Foreclosure Rates on the Rise Again

Sheila Bair: From Regulator To Watchdog

Small Banks Under Pressure From New Capital Requirements

How Much Did the Financial Crisis Cost?

Shadow Banking Down From Crisis, But for How Long?

Watch Now: Six Billion Dollar Bet

Is the U.S. Economy Prepared for the Fallout From Greece?

JPMorgan Loss Poses Early Test For Dodd-Frank Pay Rules

What Can We Learn from JPMorgan’s $2 Billion Loss?

What’s the Status of the Dodd-Frank Financial Overhaul?

The Financial Crisis Is Like… Sangria?

Live Chat 1 p.m. ET: Can Wall Street Change?

The Buzz Around That Tim Geithner Scene…

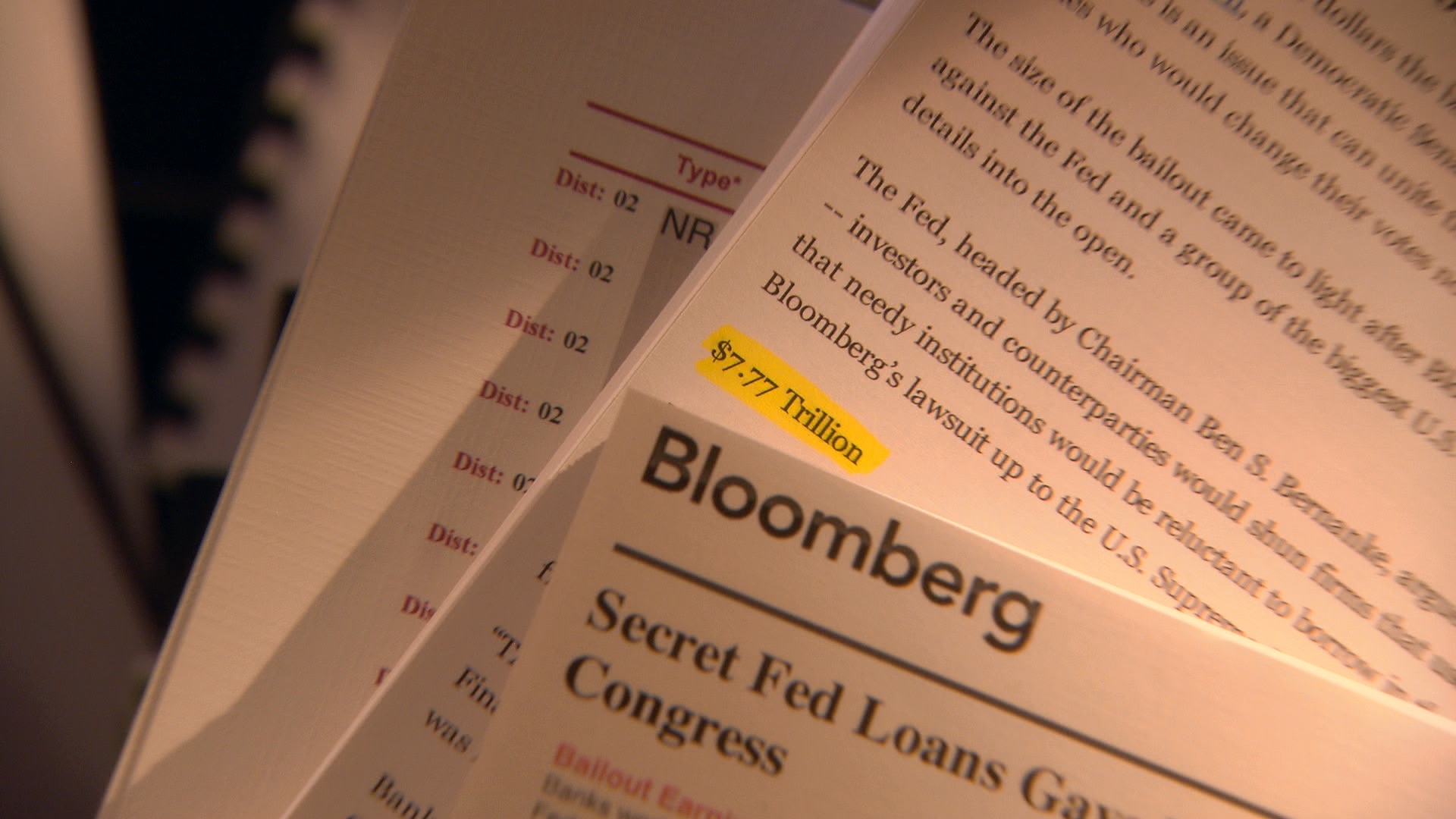

Did the Fed’s Emergency Lending Prop Up “Too Big to Fail”?

Live Chat 1 p.m ET: The Battles Behind Closed Doors

Lessons Not Learned at MF Global

What Has Occupy Wall Street Been Up To?

From Bear to Lehman: Documents Reveal an Alternate History

Live Chat 2:30 p.m. ET: How Do You Stop A Financial Meltdown? (Hour 2)

The Buzz Around “Money, Power and Wall Street”

Live Chat 1 p.m. ET: Down the Financial Rabbit Hole (Hour 1)

Next Week: How the Financial Crisis Never Ended

Introducing “The FRONTLINE Interviews”

Bloomberg: “Money, Power & Wall Street” “Takes No Prisoners”

Dig Deeper: What You Need to Know About the Financial Crisis

Top Fed Official: “The Moment Is Now” to Break Up Big Banks

Abacus: Small Enough to Jail

Related Stories

S.&P. to Pay $1.38 Billion for Once Rave Ratings of Toxic Mortgages

Pioneer Behind Credit Derivatives is Leaving JPMorgan

The Financial Crisis Five Years Later — How It Changed Us

JPMorgan To Lose $842 Million In Toxic Ala. Sewer Deal

Financial Regulators Turn Their Focus To Non-Banks

U.S. Sues Bank of America for $1 Billion Over Mortgage Sales

New Mortgage Task Force Charges JPMorgan With “Systemic Fraud”

Deadlines Loom To Bring Financial Crisis Cases

Neil Barofsky on the “Broken Promises” of the Bank Bailouts

The State of Reform: Dodd-Frank at Two Years Old

Do Credit Ratings Still Matter?

Trouble At UBS For Obama’s Favorite Banker?

Home Foreclosure Rates on the Rise Again

Sheila Bair: From Regulator To Watchdog

Small Banks Under Pressure From New Capital Requirements

How Much Did the Financial Crisis Cost?

Shadow Banking Down From Crisis, But for How Long?

Watch Now: Six Billion Dollar Bet

Is the U.S. Economy Prepared for the Fallout From Greece?

JPMorgan Loss Poses Early Test For Dodd-Frank Pay Rules

What Can We Learn from JPMorgan’s $2 Billion Loss?

What’s the Status of the Dodd-Frank Financial Overhaul?

The Financial Crisis Is Like… Sangria?

Live Chat 1 p.m. ET: Can Wall Street Change?

The Buzz Around That Tim Geithner Scene…

Did the Fed’s Emergency Lending Prop Up “Too Big to Fail”?

Live Chat 1 p.m ET: The Battles Behind Closed Doors

Lessons Not Learned at MF Global

What Has Occupy Wall Street Been Up To?

From Bear to Lehman: Documents Reveal an Alternate History

Live Chat 2:30 p.m. ET: How Do You Stop A Financial Meltdown? (Hour 2)

The Buzz Around “Money, Power and Wall Street”

Live Chat 1 p.m. ET: Down the Financial Rabbit Hole (Hour 1)

Next Week: How the Financial Crisis Never Ended

Introducing “The FRONTLINE Interviews”

Bloomberg: “Money, Power & Wall Street” “Takes No Prisoners”

Dig Deeper: What You Need to Know About the Financial Crisis

Top Fed Official: “The Moment Is Now” to Break Up Big Banks

Abacus: Small Enough to Jail

Part One

PRODUCED BY Martin Smith Marcela Gaviria

PRODUCER Thomas Jennings

CO-PRODUCERS Linda Hirsch Ben Gold

WRITTEN BY Martin Smith and Marcela Gaviria

NARRATOR: Every day, tens of thousands of workers make their way to Wall Street. They work for banks, brokerages, hedge funds, insurance companies and mortgage lenders. It is the largest single sector of the American economy, an industry that is almost double the size of America’s manufacturing sector, a business with enormous power and global reach.

It is the industry that led America and the world into its worst economic crisis since the Great Depression.

The banks say they exist to create wealth, holding in trust our collective worth, promising to invest the trillions of dollars that stream in from businesses, pension funds and savings accounts that belong to all of us.

One morning in the fall of 2011, bankers arriving in Lower Manhattan were caught by surprise.

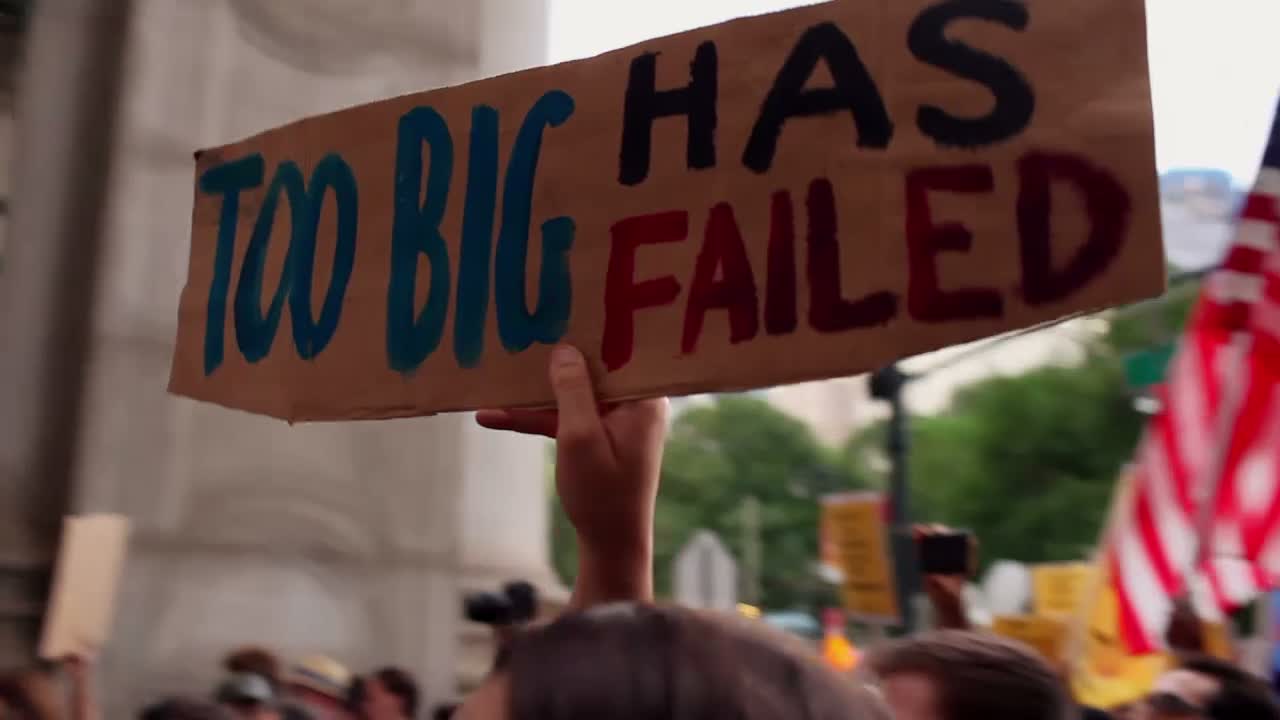

OCCUPY WALL STREET DEMONSTRATORS: This is what democracy looks like! We got sold out, banks got bailed out!

POLICE OFFICER: On the sidewalk! You must go on the sidewalk!

NARRATOR: The recession had destroyed $11 trillion of Americans’ net worth. A recovery seemed far off. Occupy Wall Street wanted bankers held responsible.

DAVID WESSEL, The Wall Street Journal: Most Americans think, and with good reason, that Wall Street got bailed out and Main Street didn’t. We have very high unemployment. We lost 8.5 million jobs in the recession. People’s houses aren’t worth what they paid for them. A lot of them don’t have jobs. Their kids are graduating from college and are moving back in.

DEMONSTRATORS: This is what democracy looks like!

NARRATOR: Some protesters were calling for bankers to be prosecuted.

DENNIS KELLEHER, Financial Reform Advocate: It is pretty clear, actually, that there was massive illegality going on. And if somebody with subpoena power was intent on prosecuting that, I don’t think there’s really much doubt that they would be quite successful in criminal prosecutions.

DEMONSTRATORS: We are the 99 percent! We are the 99 percent!

[Twitter #frontline]

NARRATOR: In a matter of weeks, Occupy demonstrations spread to scores of cities across America and the world, calling for radical changes in the banking system. Bankers responded by saying that the answer is to move on and get back to business.

STEVE BARTLETT, Financial Services Roundtable: Some of our companies made a series of bad mistakes, and— and— and— and we all paid for them, including— and— and— and it lead to the economic crisis.

MARTIN SMITH, Correspondent: But what makes people upset is that — I mean, what— you know, a lot of the people that are on the streets demonstrating, Occupy Wall Street — is that the economy hasn’t recovered but banks have.

STEVE BARTLETT: If you want a strong economy, you have to have financial services companies that are safe and sound and able to lend and able to finance their— their customers. Now, if you want to have a recession, then go ahead and— and— and hammer the banks, and you know, make sure that they’re— that they fail because then you’ll have another recession.

REPORTER: [to bankers] Do you understand why they’re angry? Do you have any comment? Mr. Blankfein, can we ask you a question, sir? Can you give the American people an accounting of how you spent their money? And do you understand why it is they’re are angry at bankers? Do you have any regrets about the way you spent the taxpayers’ money?

NARRATOR: Since the meltdown of 2008, there have been dozens of hearings.

LLOYD BLANKFEIN, Goldman Sachs CEO & Chairman: —and we regret that people have lost money. And whatever we did, whatever the standards of the time were, it didn’t work out well.

BROOKSLEY BORN, Financial Crisis Inquiry Commission: I would like to ask your opinion of the role that over-the-counter derivatives played—

NARRATOR: Many questions have been asked—

BROOKSLEY BORN: —in contributing to the financial crisis.

NARRATOR: —but there have been few satisfying answers.

DENNIS KELLEHER: What goes on at Wall Street and exactly what caused the crisis and how did we get where we are— it’s difficult to understand even for professionals.

BYRON GEORGIOU, Financial Crisis Inquiry Commission: I’m not sure I understand that point. Maybe you could elaborate.

JOHN MACK, Morgan Stanley CEO and Chairman: Well, I think that it’s— in many ways, is very simple. I think our regulators and the industry have to focus on complexity.

DENNIS KELLEHER: But at the end of the day, people usually have a pretty good ability to tell when something’s wrong.

JAMIE DIMON, JP Morgan Chairman, Pres. & CEO: Somehow, we just missed, you know, that home prices don’t go up forever.

Sen. JOHN McCAIN (R-AZ), Permanent Subcommittee on Investigations: What is a synthetic CDO?

LLOYD BLANKFEIN: A CDO is a pool of assets—

FRANK PARTNOY, Morgan Stanley, 1994-95: I think finance may have gotten too complicated for anyone to understand—

LLOYD BLANKFEIN: —that are pooled together and then can be sliced. In a synthetic, you pool reference securities that are indexed to specific more pools of mortgage.

FRANK PARTNOY: —and that the managers of these large financial institutions in some ways have been given an impossible task, that they won’t be able to comprehend what it is their institutions are doing. And that is really, really scary.

Rep. MICHAEL CAPUANO (D-MA), Financial Services Committee: You created the mess we’re in, and now you’re saying, “Sorry. Trust us.” You created CDOs. You created credit default swaps that never existed a few years ago. Who was the brilliant person who came and said, “Let’s do credit default swaps?” Find him! Fire him!

NARRATOR: It’s hard to pinpoint the origins of America’s financial crisis, but one weekend at this resort in Boca Raton, Florida, is a good place to start. Assembled here in June 1994 were a group of young bankers from JP Morgan. At the time, it all seemed innocent enough.

BLYTHE MASTERS, JP Morgan, 1991-Present: Boca Raton was a gathering of people that were part of the Global Derivative Group at JP Morgan, in part as a celebration, in part as an opportunity to relax, but perhaps much more importantly, as an opportunity to get creative, innovative people together in a room to discuss a whole variety of different topics.

GILLIAN TETT, Author, Fool’s Gold: And since they were young, mostly in their 20s, and since there was plenty of money floating around and they were full of high spirits, they did what any young bunch of kids would do and they got drunk. They had parties. They threw each other in pools. You know, this is the normal stuff that happens at conferences.

BILL WINTERS, JP Morgan, 1983-09: Yes, I went into the pool fully clothed, as did— as did my boss. Some people drank, some people didn’t. And I’m happy to say that, like, most people stayed reasonably sober.

NARRATOR: They played hard. But they also worked hard. They were striving to address an age-old problem in banking, how to reduce risk.

BILL WINTERS: The defining problem was that banks were unable to adequately deal with their own credit risks.

MARK BRICKELL, JP Morgan, 1976-01: We’re thinking about how to manage risk. We were thoughtful and deliberate and careful. We had a responsibility not just to make a profit for the shareholders, but to look after the financial system as a whole.

NARRATOR: Over two days of meetings, they looked at whether they could find a way to make their loans less risky. The first journalist to tell the full story was Gillian Tett.

GILLIAN TETT: They began to look for ways to enable financial institutions to pass risk between them. One way to do that was to sell loans. Another way, though, was to separate out the risk of a loan going bad from the loan itself. And out of that came this drive to develop credit default swaps.

NARRATOR: Credit default swaps, a kind of derivative that insures a loan against default.

This was a very new concept. Traditionally, derivatives were a way to bet on the future value of something. For hundreds of years, farmers have traded derivatives to protect themselves against fluctuating crop prices. It is this type of derivative that has been traded on the Commodities Exchange in Chicago, along with the futures of fuels, currencies and precious metals.

In Boca Raton, the JP Morgan team realized that they could use credit derivatives to trade their loan risks.

GILLIAN TETT: Bankers borrowed one set of ideas that had been developed in the commodities market and applied it to loans for the first time. This idea was essentially created under the banner of making the financial system safer.

NARRATOR: The first big credit default swap was engineered by Blythe Masters and involved Exxon.

BLYTHE MASTERS: Exxon was the client at the bank, and we had credit exposure associated with that relationship.

NEWSCASTER: The Exxon Valdez spewed almost 11 million gallons of oil into Prince William Sound.

NARRATOR: In the wake of the Exxon Valdez oil spill and a rash of lawsuits, Exxon took out a multi-billion dollar letter of credit with JP Morgan.

BLYTHE MASTERS: A letter of credit creates credit risk. If Exxon were to fail on their obligations, then JP Morgan would have to step in and make good on those obligations on their behalf. There was a large amount of exposure, and there was a significant amount of risk associated with that.

NARRATOR: And that risk is a big drain on a bank.

SATYAJIT DAS, Fmr. Derivatives Trader: Every time a bank makes a loan, under banking regulations, they’re required to set aside certain reserves of capital for the loan. So JP Morgan, when they made the loan to Exxon, would have had to set aside some capital.

DENNIS KELLEHER: JP Morgan has to hold a certain capital relative to the size of that loan in the event the loan is not paid off at 100 percent as you expect. Well, of course, if you don’t have to do that and you’re a bank, you— you’d prefer not to do that.

MARTIN SMITH: Because then you can finance more freely? You can take on more debt?

DENNIS KELLEHER: Right.

NARRATOR: So Masters started looking at who could take on their loan risk and free up JP Morgan’s capital. She found a taker in London, the European Bank for Reconstruction and Development, the EBRD.

BLYTHE MASTERS: EBRD would receive compensation from JP Morgan for taking on or assuming credit risk, and felt that that was a good risk/reward proposition. And so risk was essentially dispersed. And why did JP Morgan do that? Because we wanted to free up our capacity to do more business.

NARRATOR: This was a major financial innovation. Credit derivatives made it possible for a bank to skirt capital requirements.

SATYAJIT DAS: And that’s what actually happened, is the amount of capital that banks had to hold got less. And so banks became able to create more and more credit. They could make more loans.

MARK BRICKELL: The innovative element of swaps is that they allow companies, financial institutions, governments, to shed the risks that they don’t want to take and take on other risks that they would prefer to be exposed to.

NARRATOR: The Exxon deal was just the beginning, demonstrating that risk could be off-loaded and capital freed up. JP Morgan had struck gold. In 1998, they decided to ramp up their credit derivatives operation. That year, another young banker joined the team, Terri Duhon.

TERRI DUHON, JP Morgan, 1994-02: Part of my job was to come in as a trader and to build a credit derivative trading book, including all the risk management around the more exotic products. That was what I was brought in to do.

NARRATOR: Previously JP Morgan had written credit swaps on single companies like Exxon. Duhon was asked to write swaps on bundles of debt.

TERRI DUHON: The idea was, “Let’s put together a portfolio of credit risk, a portfolio of names.”

NARRATOR: Her first trade was a credit default swap on 306 corporate names on JP Morgan’s books.

TERRI DUHON: And that list of 306 entities, they were very highly rated. They had very low credit risk.

MARTIN SMITH: And the credit default swap was ensuring JP Morgan against default by those 306 entities—

TERRI DUHON: That’s correct.

MARTIN SMITH: —many of them Fortune 500 companies or other—

TERRI DUHON: It would have been— it would have been your— some of your most well known household names. And so we were giving investors an opportunity to, in effect, invest in our loan portfolio.

BILL WINTERS: JP Morgan did a lot of work, did a lot of due diligence to assemble this portfolio of loans. And you can get it in one easy bite-sized piece.

NARRATOR: And the bank facilitated this by slicing up the portfolio into different risk levels, or tranches. Investors could choose how much risk they were willing to take.

BILL WINTERS: Different investors wanted different levels of risk. There were some investors that wanted to earn a big return on really risky stuff, and there were some investors that wanted to earn a little return on stuff that wasn’t risky at all.

NARRATOR: From there, the bank looked to expand their business even further.

BLYTHE MASTERS: So along comes this idea. What if we could create a market where people were able to buy and sell freely, independently of the companies themselves, the risk associated with lending to those companies?

NARRATOR: And so they began selling derivatives that were simply bets on any and all portfolios, whether the bank owned them or not. These products came to be known as synthetic collateralized debt obligations, synthetic CDOs.

TERRI DUHON: There were investors who were able to invest in some entities that they had not had access to before.

MARTIN SMITH: By buying a credit default swap.

TERRI DUHON: By investing in a credit default swap because it was a name that they hadn’t previously had access to. So there was a lot of— a lot of very positive reinforcement of the market. And it just grew. It grew very naturally. Once the seed was planted, there wasn’t any stopping it.

NARRATOR: It was the beginning of an unfettered brave new world of banking.

MARTIN SMITH: This was pretty new stuff.

TERRI DUHON: This was— [laughs] This was incredibly new stuff. It was amazing. It was clearly a product that was in need. We had identified a need.

NARRATOR: Most of the members of the global derivatives group at JP Morgan were in their 20s, including Masters and Duhon. But with the creation of the credit default swap market, they had made banking history.

BLYTHE MASTERS: What in the long run this all meant was that credit, which is a vital part of the lifeblood of any economy, the global economy, became a more readily available asset. And the thinking was that that would be an unambiguously positive thing. Credit helps drive growth, helps companies deploy capital, helps employment, et cetera. It wasn’t any longer just an idea in a room in Florida, it was the creation of an entire marketplace.

[www.pbs.org: More from Duhon and Masters]

NARRATOR: Risk could now be easily traded. It fueled a worldwide credit boom. Soon other banks got excited about the money to be made writing credit derivatives.

Paul LeBlanc was a derivative salesman at Morgan Stanley who remembers the pressure to get more deals done.

PAUL LeBLANC, Morgan Stanley, 1983-04: The volume of transactions was just exploding. I mean, I used to know all the statistics because they used to talk about it every meeting, how this is a growing market and you have to get your customers involved. They can make money. We can make money. It was a massively important sector for us to focus on, derivatives.

NARRATOR: And importantly, it was a private market, unregulated, and out of view.

NEWSCASTER: —the Dow up just about two and three quarters of—

CHRISTOPHER WHALEN, Investment Banker: See, unlike an exchange-traded market where all the banks can see all the positions, there’s no public market for these derivatives. You can’t look in the newspaper and get a price for them. These are all private off-exchange markets. And nobody else in the market knows what’s going on.

NARRATOR: And because this market was opaque, the spreads — the difference between what banks could charge for derivatives and what it cost to provide them — could be huge.

MARTIN SMITH: How much were these things making for the bankers that were selling them?

CHRIS WHALEN: The spreads on derivatives are several times larger than on comparable cash securities, just as a general rule. And that’s why the banks trade them.

MARTIN SMITH: Cash securities being those that are—

CHRIS WHALEN: Equities, bonds—

MARTIN SMITH: Well, paint some picture of that and the kind of money that people were making.

CHRIS WHALEN: The best reference that you could give is that if you look at, say, the spread that a bank might earn doing an IPO for FaceBook, they’re going to maybe make 1 percent to bring out that IPO, a very hot IPO. If you were doing the same size deal in a derivative security, you might make 10 times the fee.

SATYAJIT DAS: And the basic business that they created was immensely profitable. But there’s a problem with all of this. Most people in finance assume risk can be eliminated, but all you can do is to move it around from one party to another party.

NARRATOR: There was growing concern in Washington.

Sen. BYRON DORGAN (D-ND), 1981-11: [1999] We are moving towards greater risk. We must do something to address the regulation of hedge funds and especially derivatives in this country, $33 trillion, a substantial amount of it held by the 25 largest banks in this country, a substantial amount being traded in proprietary accounts of those banks. That kind of risk overhanging the financial institutions of this country one day, with a thud, will wake everyone up.

NARRATOR: Proposals circulated to rein in the banks and to regulate derivatives.

Rep. SPENCER BACHUS (R-AL), Financial Services Committee: What are you trying to protect?

BROOKSLEY BORN, Commodity Futures Trading Commission Chair, 1996-99: We’re trying to protect the money of the American public, which is at risk in these markets.

NARRATOR: The head of the Commodity Futures Trading Commission, Brooksley Born, led the charge.

BROOKSLEY BORN: Certainly, we are the regulator which has been given the authority to oversee the major derivatives markets—

DENNIS KELLEHER, Chief Counsel, Sen. Dorgan, 2006-10: Brooksley Born was absolutely right because what she said is if you don’t have transparency and regulation of derivatives, the risk is going to build up and they’re going to lead to a financial crisis that’s going to cause massive taxpayer bailouts.

NARRATOR: The banks lobbied hard for no derivative regulation.

FRANK PARTNOY, Author, Infectious Greed: The banks didn’t want anyone to know how much risk they were taking on. They didn’t want to have to quantify it on their balance sheet. They wanted to be able to push it off and hide it. And that was why they lobbied so hard to make sure that swaps and derivatives would be treated differently from other kinds of financial products.

NARRATOR: Others wanted them to be regulated like insurance.

DENNIS KELLEHER: One of the most heavily regulated products in the country are insurance products, for all the obvious reasons. If you’re going to— if you’re going to write insurance, you have to have enough money to pay off that insurance.

MARTIN SMITH: But if you write a credit default swap, you don’t have to have that same amount of money on hand.

DENNIS KELLEHER: Or anything else, including, importantly, no disclosure.

MARTIN SMITH: So you’re saying it’s a kind of under-the-table insurance agreement that avoids regulation.

DENNIS KELLEHER: It’s an insurance product designed not to be regulated as an insurance product and designed to avoid regulation at all. And one thing we do know is that when a product of any type is designed with minimal regulation, capital and activity moves into that area and it expands dramatically.

ALAN GREENSPAN, Federal Reserve Chairman, 1987-2006: Regulation of derivatives transactions that are privately negotiated by professionals is unnecessary.

NARRATOR: The chairman of the Fed, Alan Greenspan, sided with the banks.

SIMON JOHNSON, Economist, MIT: Alan Greenspan was coming from a very libertarian tradition. Keep your hands off everything. The markets will sort themselves out. And if there’s a problem, then we’ll clean up afterwards. And now that— that really was the way the Federal Reserve operated under— under his leadership for almost 20 years.

NARRATOR: On Capitol Hill, supporters of bank deregulation made urgent, stark pleas.

Sen. CHARLES SCHUMER (D), New York: [1999] The future of America’s dominance as the financial center of the world is at stake.

NARRATOR: Before them was legislation to lift restrictions on how banks could do business.

Sen. CHARLES SCHUMER: If we didn’t pass this bill, we could find London or Frankfurt or Shanghai becoming the financial capital of the world.

Sen. PHIL GRAMM (R), Texas: This bill is going to make America more competitive on the world market, and that’s important.

NARRATOR: And legislation to prevent oversight of credit derivatives.

Sen. PHIL GRAMM: —high-paying jobs not just on Wall Street in New York City, but it affects every business in America and it benefits every consumer in America. And we do it by repealing Glass-Steagall.

NARRATOR: The campaign to roll back Glass-Steagall, a Depression-era set of reforms was led by the country’s biggest bank, CitiCorp.

SIMON JOHNSON: They felt it was in their way and persuaded lawmakers, both Democratic and Republican, that Glass-Steagall should be repealed. It also symbolized when everything really started to go wrong.

[www.pbs.org: CitiGroup & repeal of Glass-Steagall]

Pres. BILL CLINTON: It’s the most important example of our efforts here in Washington to maximize the possibilities of the new information age global economy.

NARRATOR: In the end, banks would get larger and derivatives would remain in the shadows.

DENNIS KELLEHER: The derivatives market went into darkness, almost no transparency and no regulation. And what you see is this explosion in the growth of derivatives in the United States and throughout the world.

NARRATOR: The banks had won the day. Credit default swaps would now be introduced to new markets.

BLYTHE MASTERS: The next application of this same technology was to portfolios of consumer credit risk, and in particular. mortgage-related credit risk.

NARRATOR: And the higher the risk, the better.

FRANK PARTNOY: What everyone is trying to create is something that has a high rating and a high yield. That’s the holy grail, that’s the goal, is to mix together assets in some way so that you come out with a AAA, and a big return.

NARRATOR: And so Wall Street discovered the rewards of funding the American dream. Just as they had bundled corporate loans, bankers now bundled mortgages.

PAUL LeBLANC: You would buy these big pools of mortgages, and these credit default swaps enabled you to bundle all this stuff together, bring it in-house, in order to get it ready to put through the sausage-making machine and create these securities.

NARRATOR: Bankers spread their investing dollars across the country, but especially in states seeing historic levels of population growth, places like Florida, Nevada, California, and here, in Georgia.

ROY BARNES, (D) Governor of Georgia, 1999-03: Well, Atlanta was one of the hottest markets in the country, the Atlanta region.

NARRATOR: Roy Barnes is the former governor of Georgia.

ROY BARNES: Georgia was the fourth fastest growing state at the turn of this last century, and the fastest growing state east of the Mississippi. So it was a hot market to start with.

WOMAN: I put my house on the market on a Tuesday, and it was gone Thursday.

[www.pbs.org: More on the housing bubble]

NARRATOR: Elected in 1998, Barnes is renowned for having taken on Wall Street over subprime lending, a market the Street had traditionally avoided.

VINCENT FORT, State Senator, Georgia: Subprime lending has been around for a long time and is supposed to be lending done to people whose credit is inferior.

ROY BARNES: And in the ‘80s, there was no place for subprime. Nobody wanted it. The banks wouldn’t buy it because there was a higher risk.

[television commercial]

— City Mortgage. May I help you?

— I’ve been having trouble with my credit.

— That’s no problem. We’ll give you the best rate possible.

ANNOUNCER: 688-CITY.

FRANK ALEXANDER, Emory Univ. Law School: The subprime market was originally a niche market. Originally, it was not the major banks, it was the mortgage brokers who were specialists in this market.

NEWSCASTER: Subprime loans in Atlanta jumped by more than 500 percent during a five-year period.

ROY BARNES: What really changed the appetite for subprime mortgages was you could securitize them. And you could sell it on Wall Street. They do it in tranches, and then they wrap it up so they could be packaged together and have an overall higher yield.

NEWSCASTER: Nearly half of all new single-family home construction is in the South, now more than 50,000 a month.

ROY BARNES: And of course, Moody’s says AAA. So it was just a feeding frenzy. I mean, it was just an absolute feeding frenzy for subprime mortgages.

NEWSCASTER: With the economy strong, home buyers are willing and able to spend double what they did just two decades ago.

ROY BARNES: And you could just about drive by a bank, and they’d throw a loan paper in your car as you passed by. It became very loose. Became very loose.

NARRATOR: But what big banks on Wall Street did not or would not see was what was happening on the ground around the U.S., a wave of lending abuses.

NEWSCASTER: It’s a phrase you’re likely to hear in the future—

NEWSCASTER: —predatory lending—

1st WOMAN: We trusted mortgage companies—

2nd WOMAN: We say that we were swindled.

3rd WOMAN: The situation have caused me to go into the state of bankruptcy.

4th WOMAN: This is what you call robbing somebody without a gun!

FRANK ALEXANDER: The Wild West experience in home mortgages was well under way.

NEWSCASTER: Forty one year old Hessiemay Hector, mother of three, agreed to a second mortgage at 27.5 percent.

FRANK ALEXANDER: We were creating mortgages that we had never seen before. And they were being created faster and faster.

MAN: The interest rate on these loans was as high as 42 percent.

FRANK ALEXANDER: We saw borrowers given loans that were greater than the value of their home. Home buyers were getting loans that had no income. The borrower, particularly the elderly or the low income, had no clue as to what they signed. There was a tremendous growth of mortgages that we knew made no sense financially.

VINCENT FORT: When you have a high interest rate, then you have high points. Then you have pre-payment penalties, when you have balloon payments, when you have adjustable-rate mortgages and when you layer those bad practices on top of a high interest rate, it becomes predatory.

NEWSCASTER: Black home owners in Atlanta have become such frequent targets of unscrupulous lenders that councillors regularly hold community meetings to issue warnings.

WOMAN: —monthly payments that you can’t afford.

VINCENT FORT: And why did they sell them to people that they were not good for? They did it because they could.

WOMAN AT COMMUNITY MEETING: We’ve got to fight, fight, fight, fight!

NARRATOR: Housing advocates around the country took on predatory lenders. But one of the fiercest fights was here in Georgia, over what was called the Georgia Fair Lending Act.

VINCENT FORT: But we don’t need rhetoric, we need—

NARRATOR: The bill was sponsored by State Senator Vincent Fort—

VINCENT FORT: —we need action now!

Gov. ROY BARNES: People are tricked into owing more money than they could ever dream—

NARRATOR: —and backed by Governor Roy Barnes.

Gov. ROY BARNES: —talked into believing there’s a way out.

NEWSCASTER : Governor Barnes and others are making a last ditch effort—

NARRATOR: The bill targeted high-cost loans and predatory lenders with a series of rules and prohibitions.

NEWSCASTER: It’s up right now on the House floor, a governor’s bill to crack down on—

NARRATOR: The mortgage lenders and the banks struck back.

MORTGAGE LENDER: None of these people have a clue of what’s going on! Nobody here understands the business, and they didn’t let us speak!

ROY BARNES: You would have thought I had recommended that we repeal the plan of Salvation. Why were they so opposed to it? Money. Money.

MORTGAGE LENDER: This bill will cripple the mortgage business! It’s going to cripple real estate sales! It’s going to absolutely devastate the home market in Georgia, I can guarantee you!

FRANK ALEXANDER (Prof. of Law, Emory University): There were threats that the residents in Georgia wouldn’t be able to get mortgages anymore because investors would not buy the mortgages in Georgia. And if that were true, no bank would create a mortgage in Georgia.

NARRATOR: Despite the efforts of the mortgage lobby, Barnes and Fort got the bill passed in April 2002.

NEWSCASTER: Georgia now has the toughest predatory lending law in the nation—

NARRATOR: The mortgage lobby feared that similar legislation could pass in other markets, like California. They opposed Barnes’s reelection, they funded his challenger, and lobbied to rescind the law.

FRANK ALEXANDER: Right after the Governor Barnes’s defeat in November, one of the top legislative priorities for the new governor and the new legislature was to gut the Georgia Fair Lending Act. I think it was about two weeks into the new legislative session, and it was gutted.

NARRATOR: But for a seven-month period, predatory lending in Georgia declined. It may have been the last chance to slow the housing boom.

ROY BARNES: I would like to sit up here and tell you that I was like Nostradamus, that I saw that the world was going to come to an end because of all this. But I could never have foreseen the difficulty that existed, never have— could I have foreseen that.

FRANK ALEXANDER: I think we still would have seen an unrealistic bubble, but it wouldn’t have gone up as fast and it wouldn’t have collapsed as fast. We would not have been in as deep a hole today as we are if we hadn’t had these funny mortgage products.

NEWSCASTER: No let-up in the housing boom, which is good for the economy. Homes were selling last month at a record clip, the main reason, low mortgage rates—

NARRATOR: The big banks continued to package and sell more mortgage portfolios. And more and more of these CDOs contained high-risk subprime debt. To keep the rating agencies on board, more credit default swaps were sold.

CHRIS WHALEN, Tangent Capital Partners: Let’s say I have a pool of mortgages. I have a thousand mortgages from California, and I want to package these up. But I decide, “Well, some of these mortgages may be subprime, and I want to buy a little bit of credit default insurance.”

MARTIN SMITH, Correspondent: And by doing that, you improve the profile-

CHRIS WHALEN: In theory, yes.

MARTIN SMITH: —of your CDO-

CHRIS WHALEN: That’s right.

MARTIN SMITH: —so that you can sell it better.

CHRIS WHALEN: And I can go get a rating for it, too. I could go to Moody’s and say, “Look, I have laid off 2 percent of the risk on this portfolio. Shouldn’t I get a better rating than if I just sold the pool as it was?”

MARTIN SMITH: So you take a lot of crap-

CHRIS WHALEN: That’s right.

MARTIN SMITH: —a lot of mortgages that are-

CHRIS WHALEN: Hideous crap. [laughs]

MARTIN SMITH: —people are not going to pay— right. OK. But you insure it, and the credit agency says, “Hey, that’s a good idea.”

CHRIS WHALEN: Yes. Yes.

GILLIAN TETT, Financial Times: And it seems that in the housing market, many investors actually began to take more risks precisely because they thought that they had bought protection with credit default swaps.

[www.pbs.org: Watch on line]

NEWSCASTER: New home sales jumped 13 percent over a year ago, while existing home sales rose 4.5 percent, setting a new record—

NARRATOR: The team at JP Morgan was also dabbling in mortgage debt, but they weren’t sure it made good sense.

TERRI DUHON, JP Morgan, 1994-02: We traded mortgages. We had some mortgages on our books. We certainly understood the mortgage-backed security market. But we had a lot of trouble getting comfortable with that risk.

The big hang-up for us was data. We had years and years of historical data about how corporates performed during business cycles. But we didn’t have that much data about how retail mortgages performed during different business cycles.

BILL WINTERS, Co-CEO, JP Morgan Investment Bank, 2004-09: We knew how much money people said they were making. We saw that UBS and Merrill Lynch had securitized products earnings that were growing faster than ours. And we asked ourselves the question, “What are we doing wrong? What are we missing? Have we not figured out how to lay off some of this risk?”

And honestly, we couldn’t figure it out. What we never imagined was that those other firms weren’t doing anything at all. They were just taking the risk and sitting with it.

NEWSCASTER: Sales of new single family homes shot up—

GILLIAN TETT: The first wave of JP Morgan bankers who had developed these original ideas in the 1990s, when they saw what was starting to happen — essentially, other banks were taking these ideas and applying them in ways that they had never expected — some of them began to get very worried.

TERRI DUHON: We were just about to say done on a transaction. We had a global phone call, and we were discussing the risk that we were about to do, and we had discussed it over and over and over. And finally, someone on that phone call said, “I’m nervous.”

NEWSCASTER: Twice as many home buyers are getting adjustable mortgages—

NEWSCASTER: —a huge increase in new home sales—

TERRI DUHON: We almost had stopped thinking and stopped reassessing the risk as we went along. And suddenly, we found ourselves with a product that was vastly different from where we started. And every little tweak along the way, we had all said, “Oh, that’s OK. That’s OK. That’s OK,” until suddenly, we all looked up and said, “Hang on, it’s not OK.”

NEWSCASTER: The world is still living with a lot of big unresolved problems—

NARRATOR: Other banks were not so cautious.

NEWSCASTER: —storm clouds on the horizon—

NARRATOR: They aggressively sold subprime CDOs to customers all over the world. London became a second beachhead for their trading and sales operations.

NEWSCASTER: The stock market’s on the rise and economic statistics—

CHRIS WHALEN: The City of London actually did yeomen’s service in creating some of the nastier structures. They did this offshore. These were not SEC-registered deals. These were all private placements. So they were going through the legal loopholes.

NARRATOR: A group of state-run banks in Germany known as Landesbanks were among the biggest customers. Desiree Fixler, who worked at JP Morgan, says she was amazed by these banks’ appetite for subprime mortgages.

DESIREE FIXLER, JP Morgan, 2001-04: You knew that a core group of banks in Germany would buy anything. We strongly believed they were very naive. We were amazed that they would buy this. It was— I mean, every single person, every sales person, was envious of that particular sales person that was able to cover the Landesbanks and IKB because you were in one of the hottest seats globally. You were going to generate tremendous profit margin. They were big buyers.

JOSEF ACKERMANN, CEO, Deutsche Bank: IKB was very convinced that they were one of the strongest banks in that area. They were running around, telling people how good they are in investing.

NARRATOR: Multinational Deutsche Bank did several deals with IKB.

MARTIN SMITH: Did you think, at the time, that your products were helping IKB, that these were good things for them to buy?

JOSEF ACKERMANN: Yeah, absolutely. Otherwise, we wouldn’t have manufactured these products and sold it to them.

MARTIN SMITH: So you were bullish on subprime mortgages in the U.S.

JOSEF ACKERMAN: We were bullish on the mortgage market in general, and subprime, which was an element of it, we were not overly aggressive, but we were a part of that market. Absolutely.

NEWSCASTER: Americans are buying real estate in record numbers. That demand has given—

NARRATOR: By the end 2005, the total outstanding value of credit default swaps around the world was measured in trillions of dollars and was doubling every year.

NEWSCASTER: Existing home sales rose 4.5 percent, setting a new record.

MARTIN SMITH: Did top management at JP Morgan understand credit derivatives?

TERRI DUHON: Yes, they did. Absolutely, they did.

MARTIN SMITH: Did they at other banks?

TERRI DUHON: No, not all other banks. Certainly not.

MARTIN SMITH: Did the regulators understand them?

DANIEL K. TARULLO, Federal Reserve Board Governor: I don’t think the regulators understood. I don’t think the credit ratings agencies, the bankers or the regulators fully understood all of the kinds of credit instruments that we’re talking about.

MARTIN SMITH: In other words, some big banks simply didn’t know what they had in terms of risk.

DANIEL K. TARULLO: Certainly, they didn’t— they didn’t know some of the forms of risk that they had. That’s exactly right.

NEWSCASTER: Sales were higher than most regions, up more than 40 percent in the West and Northeast—

NARRATOR: Housing prices continued to soar.

NEWSCASTER: The average price of a new home grew slightly—

NARRATOR: Banks packaged more and more CDOs. Theoretically, there was no limit. An investor didn’t need to own any actual mortgages. So-called synthetic CDOs allowed investors to bet many times over on someone else’s portfolio of debt.

BILL WINTERS: It allowed participants— either buying or selling, so on either side of the market — to take their positions without being constrained by the size of the underlying market.

[www.pbs.org: More on synthetic CDOs]

Prof. FRANK PARTNOY, Univ. of San Diego School of Law: In synthetic CDOs, all you had to do was make a side bet based on what would happen to this group of mortgages and have that be the basis of the CDO. The fact that someone had done it one time wouldn’t stop you from doing it again and again and again.

MARTIN SMITH: So how is that different than betting on the outcome of the Super Bowl?

DENNIS KELLEHER, Better Markets, Inc.: Or a horse race or a craps table. There’s no different at all. It’s just a pure bet by somebody who has no economic interest in what they’re betting on. You’re going to bet on the outcome of the Super Bowl, you’re going to bet on the outcome of a horse race, or you’re at the craps table or you’re betting on which way the dice are going to go.

MAN: We’re pretty confident that the housing market’s not going to down at all. It’s just going to go up.

CHRISTOPHER WHALEN: Within a decade, you have the most phenomenal machine anybody’s ever seen.

NEWSCASTER: New homes are selling at the second highest rate on record—

MAN: We are in a housing boom. It’s strong right now.

NEWSCASTER: Profits soared 93 percent.

NEWSCASTER: —expected to dole out $36 million in bonuses this year.

GILLIAN TETT, _Financial Times: Everyone was high-fiving. It seemed to be brilliant. The combination of free markets, innovation and globalization appeared to have delivered this incredibly heady cocktail of tremendous growth.

NEWSCASTER: Top executives will earn as much as $20 million to $50 million—

NARRATOR: Between 2003 and 2006, Dick Kovacevich, CEO of Wells Fargo, remembers attending meetings with bankers and regulators.

DICK KOVACEVICH, CEO, Wells Fargo, 1998-07: Oftentimes, what would happen at these meetings is— regulators would be there, like Chairman Bernanke, and there might be, I don’t know, 30, 40 bankers. And they would often go around the room and say, “Well, what are you guys seeing out there?” You know, “What’s working? Are you concerned about housing,” you know, trying to get input.

And when they came to me, I would say, “This is toxic waste. We’re building a bubble. We’re not going to like the outcome.

MARTIN SMITH: What did your fellow bankers say to you when you told them that you thought this stuff was toxic?

DICK KOVACEVICH: Well, the ones that were in it said I was wrong and everything’s fine. “We don’t see any losses occurring in this.”

MARTIN SMITH: But you saw risk all over the place.

DICK KOVACEVICH: We didn’t even participate in the exotic subprime side of the mortgage because we knew that this was absolutely wrong for our customers, if we would have done it, and would have been wrong for us because we think this thing was going to blow up.

FRANK PARTNOY: There’s a great set of adages on Wall Street about where risk will flow. And if you ask people, they’re basically split between two camps. One says that risk will flow to the smartest person, the person who best understands it. And the other says that risk will flow to the dumbest person, the person who least understands it.

And at least based on my experience and my understanding of what has been happening in the derivatives market, it’s the latter.

TERRI DUHON, B&B Structured Finance, 2004-Present: I was amazed at the interest on the part of investors to invest in a product that was highly complex and very risky on top of it.

MARTIN SMITH: So let me get this straight. You were— you were first to the party. You developed this tranching of stuff—

TERRI DUHON: That’s right.

MARTIN SMITH: —and writing credit default swaps on it. But now everybody else has jumped into the game.

TERRI DUHON: Everybody wants to do it.

MARTIN SMITH: But your team decided to stop. Why did so many others keep going, marching towards the cliff?

TERRI DUHON: The— I mean, there— I— look, very simply, there are certainly some— some investors, some banks, some borrowers who are a bit greedier than they should be.

NEWSCASTER: Goldman Sachs Lloyd Blankfein will take home $53 million.

NARRATOR: No one wanted the party to end.

NEWSCASTER: —pocket an estimated $40 million—

NARRATOR: Most banks believed housing prices would never go down, let alone crash.

BLYTHE MASTERS, Head of Global Commodities, JP Morgan: To imagine losses of that severity required very significant assumptions about the path of the economy which were just not in people’s mind. So it required things like assuming that house prices in the United States fell by 25 percent.

People weren’t thinking that way. And as long as house prices never fell, then these risks would never come home to roost. And that ultimately was obviously very flawed logic.

NEWSCASTER: As interest rates rose early this year, home sales slowed. And after years of record appreciation—

NEWSCASTER: —businesses and individuals do, as well, and the cost of borrowing is going up.

NARRATOR: The unraveling began in late 2006.

NEWSCASTER: Big trouble for millions of American home owners—

NARRATOR: When housing prices started to drop, only a very few bankers could see the bubble they were trapped in.

NEWSCASTER: The housing market has turned some mortgages into time bombs.

SATYAJIT DAS, Author, Traders, Guns and Money: By 2007, 2008, all the smart money knew the game had ended, and all the banks tried to effectively repackage what they were stuck with as quickly as possible and get it off their books. But there was second parallel movement which was going on, which was all about, “How can we take advantage of it?”

NEWSCASTER: The Dow-Jones average seemed in freefall, ending the day down—

NARRATOR: One of the Wall Street banks that took advantage of a declining market was Goldman Sachs. According to a congressional investigation, the bank created a series of CDOs containing toxic subprime and then sold them to customers—

LLOYD BLANKFEIN: [television commercial] We at Goldman Sachs distinguish ourselves by our ability to get things done on behalf of our clients—

NARRATOR: —while Goldman Sachs, using credit default swaps, bet against them.

Sen. CARL LEVIN (D-MI), Permanent Subcommittee on Investigations: They bet against their own clients, so when the clients lost money, Goldman was making money. Goldman has a little slogan that the clients come first. No, they didn’t. Not in these transactions. Goldman came first, second and third. They were really, I think, the only major bank which made money when the housing bubble burst.

NARRATOR: In a settlement with the SEC, Goldman admitted that some of their marketing materials did not disclose important information, but Goldman claimed that their investors were highly sophisticated institutions.

NEWSCASTER: Thirty-four subprime mortgage companies have gone bus—

NARRATOR: One customer was that German Landesbank, IKB.

NEWSCASTER: Analysts say anyone associated with the subprime market is going to pay the price.

DESIREE FIXLER, Ariya Capital, 2008-Present: Even when there was a downturn in the markets, they were still buying. I mean, the market is telling them. It’s on the screen. There are headlines everywhere, “Danger.” But they still wanted to go ahead.

MARTIN SMITH: Did you feel there was an obligation on your part to tell them that, “Look, wake up, the markets are going down. Maybe you should stop buying this crap?”

DESIREE FIXLER: Those discussions— the word “crap” wasn’t used, but I mean, those discussions definitely happened. But they felt that this was just a temporary glitch in an overall bull market. “It will recover. It has to recover.”

NARRATOR: In July 2007, the German bank, IKB, stuffed with subprime, was the first bank to fail.

NEWSCASTER: —hundreds of thousands of home owners are defaulting on their loans—

NARRATOR: It was only a matter of time before the crisis came back to Wall Street.

NEWSCASTER: —and that could hurt the value of homes nationwide by—

DAVID WESSEL, The Wall Street Journal: We knew that the housing bubble had burst. But we’d been reassured that the problem had been contained. But by the beginning of 2008, it was becoming clear that this was a much, much bigger problem than anybody anticipated.

DANIEL K. TARULLO, Federal Reserve Board Governor, 2009-Present: There was a broad misperception of the risk in housing prices. The widespread view that we could have a regional decline in housing prices, but never a national decline in housing prices, proved to be horribly wrong.

NEWSCASTER: Last week was a difficult time in the mortgage business. There was talk about problems in funds—

NEWSCASTER: This was the most actively traded stock by far—

NARRATOR: In New York, banks were trying to unload what they could. But there was confusion. At CitiGroup, they were running in circles.

FRANK PARTNOY, Author, Infectious Greed: One of the incredible things about CitiGroup, we now know, was although it was tossing these risks off its balance sheet, those risks came right back, almost like a boomerang. Without knowing it, they had set up one business to offload risk, and then completely reversed that business, taking those risks back onto its balance sheet.

DANIEL K. TARULLO: It was quite clear to me that a number of really quite large financial institutions had not had the kind of management information systems which allowed them even to know what all their risks were.

MARTIN SMITH: that was astounding to you.

DANIEL K. TARULLO: It was astounding to me.

NEWSCASTER: The sort of origination of these subprime loans, the creation of the CDOs— that business is gone.

NEWSCASTER: And the reason why is all those credit default swaps—

NARRATOR: It would all come down to those credit default swaps. Would they pay off as they were designed to do?

DAVID WESSEL: We have known for generations that banks are susceptible to runs. Banks can’t function if everybody comes and wants their money at the same moment.

NEWSCASTER: —Merrill Lynch, devastated by losses—

NEWSCASTER: The failure of Lehman Brothers and the fire sale of Merrill lynch—

NEWSCASTER: —starting to take a closer look at AIG. The world’s largest insurance company—

NARRATOR: This time, it would be a run on an insurance company. AIG was on the hook for $440 billion worth of credit default swaps.

NEWSCASTER: —credit default swaps—

SATYAJIT DAS: Remember, an insurance contract is only as good as the credit quality of the insurer. They have to pay you. And if they can’t pay you for whatever reason, then this whole process of risk transfer breaks down.

NEWSCASTER: We need to stabilize this industry. It can spread throughout the economy. It could be a very, very dangerous—

STEVE BARTLETT, Pres., Financial Services Roundtable: September 18th of 2008, when I have a conference of my CEOs, and CEOs traditionally don’t read their Blackberries during meetings. But I kept looking around and noticing that a number of them were. And so I turned to one. We recessed. And I said, “You looked like the world was ended.” And he said, “I think it has.”

NEWSCASTER: —the enormity of the situation, like a financial nuclear holocaust. Some $400-odd billion of credit default swaps—

NEWSCASTER: —another government bailout, AIG securing an $85 billion—

DANIEL K. TARULLO: AIG could not conceivably have paid off all of those credit derivatives because it had misunderstood the risks and did not have what we’d call a balanced book or nearly enough capital to back their losses.

MARTIN SMITH: Didn’t everybody know that AIG was holding a lot of CDSs?

CHRISTOPHER WHELAN: No. There was no disclosure. That’s the whole point They haven’t reported this to anyone else. The other dealers have no idea what’s going on. The other banks don’t know. Nobody knows. The banks turned this market into their own private game.

SATYAJIT DAS: It was, in fact, a financial shell game where we were manipulating banking results by moving the risk out through one door, but bringing it back into the banking system by another door. The risk was not leaving the banking system, and everybody in the world was connected to these chains of risk. And if any part of that chain breaks down because they can’t honor the contract, the entire system implodes.

NARRATOR: The idea dreamed up by a group of young JP Morgan bankers at a weekend retreat many years ago was supposed to reduce risk.

GILLIAN TETT: Their original idea had been taken and it turned into a Frankenstein monster, which they never dreamt would become so big and spin out of control to that degree.

BLYTHE MASTERS: It was a very scary time. We were in totally new territory. And the notion that Lehman Brothers could be filing for bankruptcy and AIG could be at risk of the same fate was absolutely unprecedented. And the implications— thinking through the implications of that for the health not just of the U.S. economy but the world were— I mean, it wasn’t— it wasn’t really conceivable to do that. I couldn’t get my mind around it. I know others couldn’t.

TERRI DUHON: We never saw it coming. We never saw that coming. And I was disappointed, hugely disappointed. I mean, I was part of a market that I believed was doing the right thing. And maybe I was idealistic, maybe I was young, maybe I— I didn’t fully appreciate where we were going, but there was a whole system going on all the way from the borrower of the mortgage, all the way through to the investor. There’s a whole system of people who maybe were turning a blind eye, maybe were, you know, just— I don’t know. It’s— it’s frustrating to see, certainly.

DICK KOVACEVICH, Chairman, Wells Fargo, 2005-09: It shouldn’t have happened. Most of our financial crisis in the past is due to some macroeconomic event— an oil disruption, war. This was caused by a few institutions, about 20, who, in my opinion, lost all credibility relative to managing their risk.

And the sad thing is it should never have happened. The management should have stopped it before it got big. And people are suffering for something that should never have happened.

NARRATOR: Today, the fallout is felt mostly in places that had seen the highest growth, like Georgia. Ground zero of the subprime crisis— local neighborhoods, city streets.

Prof. FRANK ALEXANDER, Emory Univ. Law School: Cities throughout the United States are seeing a rise in vacant and abandoned properties. And that’s where the neighbors feel it. As neighbors, we’re concerned not so much with the complexities of the subprime mortgage market and derivatives. These things we will hardly ever understand.

What we feel on the street is the fact that the house next to us is vacant, abandoned, partially burned. And we wonder how long it’s going to be there, how long we pay the price for that abandonment. A neighborhood cannot survive long when it has a growing inventory of vacant, abandoned properties.

NARRATOR: Sometimes, no one even knows who owns the properties.

MTAMANIKA YOUNGBLOOD, Atlanta Housing Activist: It’s hard to know who owns it because it’s been sliced and diced so many ways by investors that it could be somebody in Ireland who owns it.

You have these securitized pools, where investors own pieces of it. The investors are around the world, literally, and so it’s just in no-person’s land. It’s a vacant property, mostly vandalized, and it just sits here and we can’t do anything with it. And the reality is that that plays out across this neighborhood hundreds of times.

ROY BARNES, (D) Governor of Georgia, 1999-03: That house has a loan that is somewhere lost in a huge financial vehicle put together by some young Turks on Wall Street. It’s lost in that billion-dollar package because there’s nobody assigned to look after it.

And there are whole subdivisions like this, by the way, that are just lost in this great morass. And so it affects Main Street because Wall Street was too greedy. The greed of Wall Street broke Main Street.

Money, Power & Wall Street Part Two

PRODUCED BY Michael Kirk Jim Gilmore Mike Wiser

REPORTED BY Jim Gilmore

WRITTEN BY Michael Kirk & Mike Wiser

DIRECTED BY Michael Kirk

ANNOUNCER: Coming up next, FRONTLINE’s four-part investigation of the financial crisis continues.

NEWSCASTER: Concerns about shaky home mortgages are triggering fears of a financial meltdown on Wall Street—

ANNOUNCER: Inside Washington’s struggle to respond to the meltdown.

NEWSCASTER: The Dow tumbled 240 points, while the NASDAQ sank 46—

ROBERT REICH, Secretary of Labor, 1993-97: They were all very afraid of the possibility of a bank failure. They didn’t know what it would lead to.

NEWSCASTER: —fears of a global liquidity crisis have intensified today—

ANNOUNCER: Inside the critical decisions—

NEWSCASTER: The stock market dropped by hundreds of points—

PHIL ANGELIDES, Chmn., Financial Crisis Inquiry Comm.: The policy makers have sent inconsistent signals. So the marketplace doesn’t know what to expect.

CHARLES DUHIGG, The New York Times: Everything freezes, and that’s what causes the crisis.

NEWSCASTER: —turmoil in markets around the globe—

PAUL KRUGMAN, Economist, Princeton University: My God, we may be presiding over the second Great Depression.

ANNOUNCER: —the politics of a bailout—

MICHAEL GREENBERGER, Federal Regulator, 1997-99: They had to throw their principles out the door and save the economy.

Rep. SCOTT GARRETT (R), New Jersey: America, you should be outraged about what Washington is about to do!

ANNOUNCER: —and the education of a future president—

RON SUSKIND, Author, Confidence Men: The economy is melting. The Bush administration is leaving.

NEWSCASTER: And all eyes are now on Barack Obama to turn it around.

RON SUSKIND: Obama gets a real glimpse of the future. Disaster is coming.

ANNOUNCER: Money, Power and Wall Street continues right now.

NARRATOR: It was on a cold March day in 2008 that the fear of a meltdown would become a reality.

NEWSCASTER: —fears of a financial meltdown on Wall Street—

NEWSCASTER: Home foreclosures rose to record highs—

NARRATOR: After the real estate bubble burst, it would only be a matter of time before investors would start to lose confidence in Wall Street’s biggest banks.

NEWSCASTER: It started with news that some Bear Stearns hedge funds would—

NEWSCASTER: The Case-Shiller home price index—

NARRATOR: Bear Stearns was the first to crack.

BRYAN BURROUGH, Vanity Fair: Pretty normal morning. And then suddenly, around 11:00 o’clock, there’s a tremor. The stock starts to go down. The CFO of Bear starts calling down to his desks, to the repo guys, the bond guys, “Anybody hear anything? Anybody know anything? What is this?” “Yeah, the rumor is that we’re running out of cash and that we might be in trouble.”

NEWSCASTER: —leading this very sharp rally on Wall Street, with the exception of Bear Stearns—

NARRATOR: The rumors swirling around Bear were about its massive investments in subprime mortgages, what would become known as “toxic assets.”

DAVID FABER, Author, And Then the Roof Caved In: They were big in mortgages. They were big in packaging them and creating securities out of them, buying them.

NARRATOR: The road to riches for Bear was simple, buy hundreds of thousands of subprime mortgages, then bundle and sell them to investors. But now the party was over, and Bear was spiraling out of control.

DAVID FABER: [CNBC appearance] You’ve either got liquidity or you don’t, so—

BILL BAMBER, Fmr. Sr. Managing Dir., Bear Stearns: It was nothing short of surreal.

DAVID FABER: But those are the kinds of concerns in this market, concerns of confidence—

BILL BAMBER: You’re watching on CNBC, et cetera, I mean, they’re talking about where you work.

CNBC ANCHOR: Well, the only bank in the red right now, basically Bear Stearns, although it is dragging the rest of the financial markets down, as well.

NARRATOR: The stock was in freefall, and the cash reserves were shrinking.

JEFFREY LANE, Fmr. CEO, Bear Stearns Asset Management: The stock started to go down. More and more people called up and said, “I want my money out” or “I won’t trade with Bear Stearns.” And it just completely unwound.

NARRATOR: Nearly bankrupt, the top brass at Bear called Wall Street super-lawyer Rodgin Cohen.

H. RODGIN COHEN, Lawyer, Bear Stearns: It became clear that they were having serious funding difficulties. And it had been very clear to me that an investment bank has a very short lifespan after it loses its liquidity.

NARRATOR: Cohen made an emergency call to Timothy Geithner, the president of the New York Federal Reserve.

H. RODGIN COHEN: Geithner understood that it was a vulnerable situation. He said something like, “Believe me, I’ll be on it.” And that was really the phone call.

NARRATOR: Geithner was Bear’s last chance.

DAVID WESSEL, The Wall Street Journal: Tim Geithner is at the Federal Reserve bank of New York. It’s the epicenter of the financial system. He is supposed to be the Fed’s front-line general, field marshal, in the financial markets.

MARK LANDLER, The New York Times: He’s 47 years old. He looks like he’s about 32.

PAUL KRUGMAN, Economist, Princeton University: Extremely smart, extremely aware of this stuff, very discrete, controlled.

NARRATOR: Geithner realized he needed to know how bad Bear’s books looked. He dispatched a SWAT team of investigators from the Federal Reserve to Bear’s headquarters.

BETHANY McLEAN, Co-Author, All the Devils Are Here: Tim Geithner is frantically involved in trying to figure out what’s going to happen if Bear melts down, and how you need to prevent it from going into freefall and dragging down the rest of the financial sector with it.

BRYAN BURROUGH: By midnight, by 1:00, 2:00 in the morning, everybody and their mother has teams at Bear— Morgan, the Fed, the SEC— and they find out Bear is stuffed to the gills with toxic waste.

NARRATOR: Bear was party to complicated financial deals.

BETHANY McLEAN: Nobody understood how subprime mortgages had proliferated through these things called credit default swaps. And nobody understood how they’d kind of gotten into the blood of the financial system.

NARRATOR: Geithner learned that Bear had made credit default swap deals worth trillions of dollars all over Wall Street and around the world.

Rep. BARNEY FRANK (D-MA), Chmn., Financial Services Cmte., 2007-10: Because Bear Stearns was so indebted to so many other people, their failure to repay their debts, or pay their debts, would cause a cascade of other failures.

NARRATOR: Geithner saw what central bankers fear most, “systemic risk.” Bear was frighteningly interconnected with other banks up and down Wall Street.

H. RODGIN COHEN: No one knew what would be the ramifications, which other institutions were exposed, which other institutions would suffer runs.

NARRATOR: Bear Stearns, Geithner concluded, was “too big to fail.” A bankruptcy could undermine confidence in every major Wall Street firm.

ROBERT REICH, Secretary of Labor, 1993-97: They were all very afraid of the possibility of a bank failure. They didn’t know what it would lead to.

NARRATOR: The precipitous collapse of Bear Stearns had taken federal regulators almost entirely by surprise.

PHIL ANGELIDES, Chmn., Financial Crisis Inquiry Comm.: What became clear, as you look at the record, is the extent to which the people who were charged with overseeing our financial system really didn’t have a sense of the risks that were embedded in that system. They didn’t see the fundamental rotting in the system that had manifested itself for years.

NARRATOR: A year later, Phil Angelides would chair the Financial Crisis Inquiry Commission. In their report, the commission concluded regulators at the Federal Reserve, the SEC and other agencies ignored evidence that Wall Street was flirting with disaster.

[www.pbs.org: Read the report]

PHIL ANGELIDES: You would think that the people who were in charge of our financial system would have a grip on the key risks that were in it. And if they did, they would have moved, in a sense, to get a handle on those. They had deliberately turned a blind eye to those problems.

NARRATOR: For three decades, Washington had steadily moved to a hands-off attitude towards Wall Street. And with little oversight, inside these black boxes, Wall Street had created a host of complicated but lucrative financial products.

[Twitter #frontline]

BROOKSLEY BORN, Financial Crisis Inquiry Commission: We had no regulation. No federal or state public official had any idea what was going on in those markets. It was a dark market. There was no transparency.

JOSEPH STIGLITZ, Economist, Columbia University: They were making money, and they want to continue making money. It was generating fees. Transparency drives profits down, drives down transaction costs. The banks don’t want that because they make their money from transaction costs, and they like lots of non-transparency.

NEWSCASTER: The story has continued to mushroom, and there are concerns among—

NARRATOR: Now, with Bear failing, those dark markets threatened to bring down the American economy.

At 4:00 AM, Tim Geithner picked up a phone and called the chairman of the Federal Reserve in Washington, Ben Bernanke.

MARK LANDLER, The New York Times: Ben Bernanke is a highly, highly respected scholar, and not only a scholar of economics but of the Great Depression.

PAUL KRUGMAN: If he weren’t chairman of the Fed, he’d be top of the list of people you’d be going to for advice and understanding in all this stuff.

NARRATOR: One of the Depression expert’s biggest fears was being realized.

MARK GERTLER, Economist, NYU: It was clear that this had to be contained. There was no doubt in his mind. He, more than anyone else, appreciated what would happen if it got out of control.

NARRATOR: Bernanke believed that just as in the Depression, a lack of confidence in the banks could bring down the entire economy.

RICHARD FISHER, President, Dallas Federal Reserve: You could see the credit default swap spreads widening. The market was telling you something was wrong.

NEWSCASTER: Well, here we are, 90 minutes in, and it looked— it looked like it was going to be a big up day, but—

NARRATOR: The next morning, Bernanke warned President George W. Bush’s treasury secretary, Hank Paulson, of systemic risk to the financial system if Bear collapsed.

KATE KELLY, Author, Street Fighters: Paulson was picturing a 1,000 to 2,000-point drop in the Dow that Monday, possibly the failure in very short order of a number of other investment banks— Lehman Brothers, Morgan Stanley, and so on.

NARRATOR: Paulson thought he knew the markets well. Only two years before, he had run Bear’s largest competitor.

STEVE LIESMAN, CNBC: Paulson comes from the great breeds of masters of the universe that have come from Wall Street.

GRETCHEN MORGENSON, The New York Times: Henry Paulson came from Goldman Sachs. He was a very powerful Wall Street figure.

NARRATOR: At Goldman, he had overseen the growth of those complicated financial products, and was always a champion of the free market.

JOE NOCERA, The New York Times: Paulson does not have the mentality of a regulator, he has the mentality of an investment banker, that the market rewards and the market punishes, so you don’t need a lot of regulation.

NARRATOR: A bailout of Bear Stearns was not Paulson’s style, but Bernanke and Geithner believed it was too big to fail. And by that weekend, options were dwindling.

MICHELE DAVIS, Asst. Secretary, Treasury, 2006-09: It was a gut check moment. Do we feel like we can take the risk of letting it go? They all looked at each other and just said, “I’m not ready to take that risk.”

NARRATOR: They would use $3 billion of government money to avoid a bankruptcy. Tim Geithner would broker a fire sale of Bear Stearns to JP Morgan.

DAVID WESSEL: The Federal Reserve used powers that it had had but had lain dormant since the Great Depression. They basically took $30 billion, went to JP Morgan and say, “We’ll give you $30 billion if you buy this Bear Stearns, so it doesn’t have to go out of business.” And they did.

BOB IVRY, Bloomberg News: What the New York fed did was take all the bad stuff off the books of Bear Stearns and allow JP Morgan to purchase the good part of it. It’s kind of like if Uncle Sam had come in and taken all the vinegar and allowed JP Morgan to have the wine.

NARRATOR: Bailing out a major financial institution in crisis was something Tim Geithner had seen before. It was taken from a playbook created back in the 1990s, how to respond to a financial crisis.

CHRISTINA ROMER, White House Econ. Advisor, 2009-10: Tim Geithner, going back even to his days in the Clinton administration, is sort of known as a cool head in a crisis, and in, you know, “How do you manage a really troubled financial system?”

NARRATOR: In the Clinton administration, Robert Rubin was the treasury secretary. Larry Summers was his top deputy. And undersecretary Tim Geithner was always in the room.

JOSHUA GREEN, Bloomberg Businessweek: They had this bonding, unifying experience during the Clinton administration putting out these various crises, from Thailand to Japan to Indonesia. Geithner was one of the guys who was sort of part of that SWAT team that understood how to react to a financial crisis.

NARRATOR: They engineered massive bailouts when American banks were threatened by financial turmoil overseas. Working with the International Monetary Fund, they loaned hundreds of billions in countries like Mexico, Thailand and South Korea. Rubin and Summers, along with Federal Reserve chairman Alan Greenspan, became superstars of the financial world.

BETHANY McLEAN, Co-author, All the Devils Are Here: You had this infamous now Time magazine cover with Bob Rubin, Larry Summers and Alan Greenspan, called “The committee to save the world.” And that just sums up the attitude of the times perfectly.

JOSHUA GREEN: By the end of the Clinton administration, the folks in the Treasury — Geithner, Summers, Rubin — felt like there was an established playbook for dealing with a financial crisis. The first thing you had to do was come in and flood the banks with money so that they would keep lending, as difficult as that was to do politically.

NARRATOR: It was an approach Geithner took with Bear Stearns, spending lots of money to respond to a financial crisis. But Treasury Secretary Henry Paulson thought Geithner’s strategy might send a dangerous message. He started publicly reminding Wall Street of one of the most basic tenets of the free market, moral hazard.

HENRY PAULSON, Treasury Secretary: I’m as aware as anyone is of moral hazard. I am also aware of—

JOE NOCERA: Moral hazard poses the question, if you bail somebody out of a problem they themselves cause, what incentive will they have the next time to avoid making the same mistake?

RON SUSKIND, Author, Confidence Men: Paulson is out in public saying, “It’s all on you now. This was a one time only event,” right? “You’re on your own now. We did it with Bear, but now you’re on your own.”

NEWSCASTER: There’s news today of a federal bailout for a Wall Street investment—

NEWSCASTER: It’s a fire sale for troubled Bear Stearns.

NARRATOR: The bailout of Bear Stearns landed in the middle of an election year.

Sen. BARACK OBAMA (D-IL), Presidential Candidate: Are you fired up? Are you ready to go? Fired up! Ready to go!

NARRATOR: Barack Obama had already made the economy a key issue.

Sen. BARACK OBAMA: —because we’ve got eight years of disastrous economic policies. That’s what we’re going to change when I’m president of the United States of America!

CHARLES DUHIGG, The New York Times: Obama very early realized that things were only going to get worse. And so, Obama made this decision, “The thing I’m going to run on is that there’s a problem in our economy, my opponent doesn’t see it, and I can fix it.”

NARRATOR: And right after the Bear Stearns crisis, he turned his attention to Wall Street. He had an inside source, the man in the pink striped tie.

ROBERT WOLF, Chairman, UBS Americas: We met for a little dinner, just him and I, and you know, I was hook, line and sinker. I felt like here was a guy that could really bring this country together.

NARRATOR: Robert Wolf was a Wall Street power broker, the chairman of UBS Americas, part of the giant Swiss bank.

ROBERT WOLF: From that day on, we started talking very, very often. I don’t know if it was once a week, three times a week, five times a week, emailing back and forth. But from that time on, we started talking about the markets and the economy nonstop.

NARRATOR: And with Wolf’s support, Obama decided to confront the bankers on their own turf.

ROBERT WOLF: I actually went down to the Cooper Union speech with him in his car.

Mayor MICHAEL BLOOMBERG (R), New York City: —Senator Barack Obama.

ROBERT WOLF: He was talking about the idea of making sure that the ethics of Wall Street was pure and that we were doing the business that we should be doing.

Sen. BARACK OBAMA: [March 27, 2008] We let the special interests put their thumbs on the economic scales. We’ve excused and even embraced an ethic of greed.

JONATHAN ALTER, Author, The Promise: The Cooper Union speech was essentially Obama’s effort to say to the Democratic Party and to the country that he believed that we had to rein in Wall Street, we had to resume more aggressive regulation of Wall Street.

Sen. BARACK OBAMA: Instead of establishing a 21st century regulatory framework, we simply dismantled the old one. In doing so, we encouraged a winner-take-all, anything-goes—

NARRATOR: In the audience, Wall Street’s power brokers were paying close attention.

ROBERT WOLF: He was sitting in the heart of the world financial center, talking about regulation before we started talking about regulation.

Sen. BARACK OBAMA: A free market was never meant to be a free license to take whatever you can get, however you can get it.