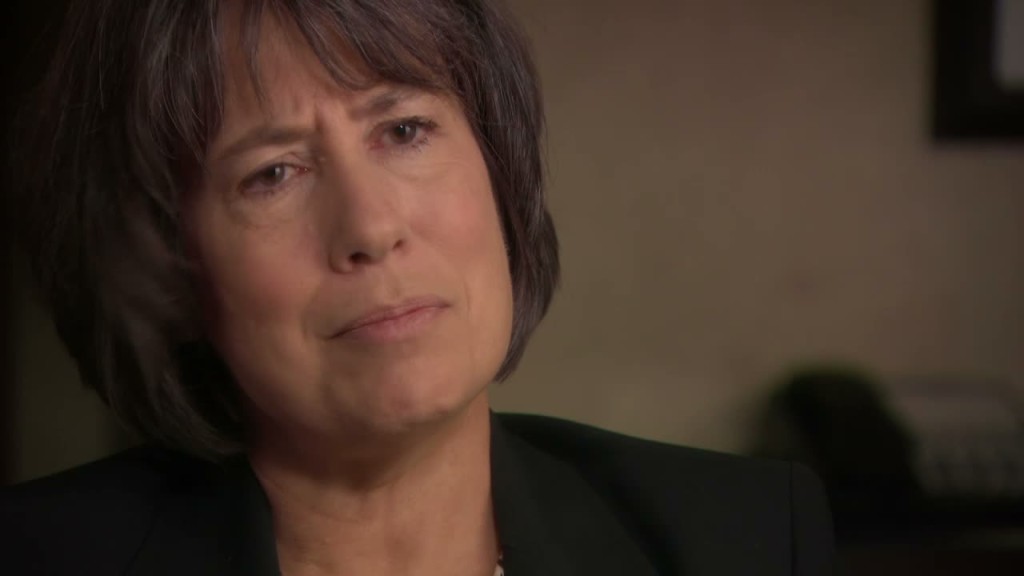

Sheila Bair: From Regulator To Watchdog

June 12, 2012

Share

If Spain’s weekend request for up to $125 billion in bailout funds was a reminder of anything, it was of the lingering threat of systemic risk to the global financial system.

Here in the U.S., the Dodd-Frank law was designed, in part, to eliminate systemic risk — that is, the idea that the failure of one institution could be big enough to bring down an entire economy. Implementing financial reform has taken longer than expected, though, and that has many watchdogs increasingly on edge.

Count Sheila Bair among the concerned. Last week, Bair, the former chairwoman of the Federal Deposit Insurance Corporation, announced she will be leading a new private sector group called the Systemic Risk Council whose mission will be to encourage reform.

The council’s members are a who’s who of regulators, lawmakers, and academics, including Paul Volcker, former chairman of the Federal Reserve; Brooksley Born, a former chairwoman of the Commodity Futures Trading Commission; and Paul O’Neill, who served as Treasury secretary under George W. Bush.

As the council prepares to issue its first call to action on June 18, Bair spoke to FRONTLINE about the challenges she sees facing reform.

What does it say about the state of financial reform that you felt a need to launch the Systemic Risk Council?

I think it’s getting bogged down. I think it has become confusing to the general public. They’re losing confidence in the reform effort, which I think is unfortunate because if we don’t have public support for reform to counter some of the more special interest influences that are always brought to bear, we’re not going to get good reforms in place.

So I do think there is a need for an independent voice, a monitor if you will, a group of wise men and women who have established track records of public confidence and knowledge of financial regulatory matters to provide some clarity and commentary on what the priorities should be.

When Dodd-Frank passed, it was one of the few pieces of recent legislation to win bipartisan support. What happened? Why have people grown so weary of reform?

Dodd-Frank is a very complicated law. … I also think, frankly, there are some who oppose various elements of reform who have played for time. I think they think, quite rightly, that the longer you drag this out, the more controversy and confusion you can generate, the more the public and the political support will lose its steam. You can just wear people down. You can wear the regulators down. You can wear the public down and eventually get the rule that you want. …

“Obviously you need to listen to industry, but your job is not to protect the industry. Your job is to protect the public.”That’s not to say that everything that industry says is wrong. Obviously you need to listen to industry, but your job is not to protect the industry. Your job is to protect the public. When industry lobbyists come in, it is their job to advocate for their own interest, so they will be advocating for whatever it is that’s going to make them the most money. And regulators just need to understand that, and members of Congress need to understand that when these positions are advocated.

What do you hope to accomplish through the council?

We will make commentary at a high level … We’re not going to be trying to write the rules for the regulators. We’re not going to be second-guessing them. We are going to be saying these are [areas] where you need to be focused.

I think really the effort is to try to provide better focus and clarity about what the remaining risks are, the things that need to be finished sooner than later to protect the broader public. Because not much has changed frankly, I’m sorry to say, from 2008, and it needs to change, because the system we had prior to 2008 was not a stable one. It was one that brought us a lot of economic hardship for a lot of people and it needs to be fixed.

How much influence can you truly have in the face of the millions of dollars that Wall Street is paying to lobby against reform?

I hope we can have a lot. You certainly have a lot of very influential names on this council. So I don’t think we’re going to be able to work miracles, but I think we can have an impact on regulation that’s focused on the public interest.

When we’re talking about systemic risk, we’re largely talking about this issue of “too big to fail.” If anything, though, the banks that nearly crashed the system are even bigger today. What’s to be made of that?

I think for me the issue is more complexity than it is sheer size. And I’m just speaking for myself now, I think this is an area that obviously the council will want to deal with in detail, how you deal with so-called systemic institutions.

A bread-and-butter bank, even if it’s a very large one, if it takes deposits and makes loans — certainly you can get yourself into trouble making loans, but those are risks that are understood. I think they’re understood by managers and bank boards and investors and examiners much better than some of these enormously complex activities that the very largest banks now engage in.

I would like to see more simplification of these entities. Better separation of business lines. Better focus, specialized focus on each business line. And frankly risks that are not well understood should not simply be undertaken.

Of course, risk is an inherent aspect of capitalism, so how do you square that with the larger goal of safeguarding the broader financial system?

You obviously need to take risk, but you need to take risk that you understand. How many boards of financial institutions understand the derivatives book of the institution they oversee? My guess is not very many.

Paul O’Neill, who is also on our council, I remember him telling me when I worked with him at Treasury, when he was the CEO of Alcoa, every week he would have his CFO come in and brief him on their derivatives position. And if he didn’t understand a derivatives position, they didn’t take it. Wouldn’t that be refreshing if we had more managers and boards taking that approach?

I think sometimes people are intimidated. They don’t want to admit that they don’t understand. That’s nuts. Your job as a manager or as a board member is to understand the risk, and if you don’t understand the risks you shouldn’t be undertaking them. So yeah, we want banks to take risk, we even want them to make money, but we want them to do that in a way where they don’t hurt other people in the process.

What do you say to critics who argue that excessive regulation is overburdening business and thus slowing the recovery?

You need rules of the roads. There’s a difference between free markets and free-for-all markets. Any good financial system needs some good, basic, prudential regulation. It doesn’t need to be complex. It doesn’t need to be prescriptive.

“There’s a difference between free markets and free-for-all markets.”I’m a big believer in regulation that aligns economic incentives. Make people put their own skin in the game. Increase capital requirements. Make bank owners put more of their own money at risk instead of just using leveraged, borrowed money to make their bets. … Again these are just my personal views.

When regulation tries to get very, very prescriptive and says, “You can do this, you can’t do that,” then you do run into inefficiencies and stifling of healthy innovation. … The other problem with overly prescriptive rules is that they can never keep pace with whatever the new area of risk-taking may be. But with capital, capital is always there. No matter what kind of risk, what falls through the cracks, what new risk emerges that people don’t get ahead of, there’s going to be capital there to absorb the losses. So capital has the constancy about it that can help keep pace with innovation but still make sure, again, that if the financial institution messes up and has losses, the rest of us aren’t hurt.

What do you see as the biggest threat facing the financial system today?

Complexity and leverage. Historically, every single financial crisis has been driven by excess leverage. This is my personal view. … With this protracted period of very low interest rates, you are seeing more and more decisions being made where people are looking for return, and as they look for return, they want to go farther and farther out on the risk curve to generate those returns. So I do worry about that.

I think there are incentives to take risk now — strong incentives to take risk — that perhaps are not wise. And if you’re doing that with borrowed money you’re setting yourself up for potential failure again. So I think that is a real problem.

What would happen if the economy fell back into crisis? In what ways are we better off today than in 2008? How are we worse off?

The banks have more capital now. Their liquidity is not as stable as is should be, but they do have more capital which is an improvement pre-crisis. So I think that puts us in better shape.

But the risks that we face — I mean the European situation is very problematic and I don’t think we have a good handle of what the impact could be on the United States if there’s a bank run in Europe or a major bank failure there …

Longer term, our fiscal situation here is a source of risk to the economy and the financial sector. Right now, our government is able to fund itself through very cheap debt, frankly, because Europe is having so many problems. People are not looking too closely at us. But that’s not going to last forever, and if and when investors start to realize how bad our fiscal situation is, and start to demand higher interest rates on our government debt, that could have severe negative impact on the economy as well as the financial sector.

I guess that’s all to say I get so frustrated by some of these big financial institutions, and their hordes of lobbyists descend on Washington, spending all this energy on fighting reform, when I wish they were really focusing their efforts on managing the risk and trying to prepare and anticipate the risk that could come from a deteriorating situation in Europe or here with us not getting our own fiscal house in order. I wish they would focus more on that and less on fighting regulators all the time over common-sense regulation.

What would be the single most important step lawmakers could take to better protect the economy?

Speaking for myself … I think Congress, and this administration, for elected political leadership, I think the best place that they can focus their attention is on our fiscal problems. This doesn’t mean we need austerity right now. But it does mean that businesses and households need to know what the long-term game plan is. Businesses need to know what the tax code is going to look like. Households do too. People are retiring now; they need to know what’s going on with Medicare and Social Security. Are benefits going to be reduced? Are premiums going to be raised? Workers need to know what’s going to happen with the payroll tax.

All these things are on the table and need to be resolved, but the uncertainty surrounding them creates risk aversion on the part of the general population. So we hoard our money in nice, safe, FDIC-insured deposits, or buy government debt, or very safe corporate debt. We sit on a lot of cash, we don’t spend it, we don’t invest it, because we just don’t know what the future is going to hold.

“If we wait for another crisis, it’s going to be too late because there’s really not many bullets left.”So putting a long-term plan in order, a bipartisan plan — Simpson-Bowles [PDF] was one approach I think would have worked very well. We need some combination of revenue increases and entitlement and defense spending constraint, and I think people need to understand that our government can function and put a plan together and let us know, and our kids know, what the future is going to hold. …

The problems we have now are structural, and only Congress and this administration can fix the structural problems. … We always seem to pull through. … We always seem, even if it’s the 11th hour, to make the right decision. But my 11th hour was last year, and so I am getting a little worried about that. …

We can’t wait for another crisis for Congress to make these decisions. If we wait for another crisis, it’s going to be too late, because there’s really not many bullets left. There’s not going to be anything to fall back on if there’s another crisis. So we need to get a fiscal plan in place to avert that and to prevent that from ever happening.

Former Digital Editor

Related Documentaries

Latest Documentaries

Related Stories

Money, Power and Wall Street

Related Stories

Money, Power and Wall Street

Explore

Policies

Teacher Center

![]()

Jon and Jo Ann Hagler on behalf of the Jon L. Hagler Foundation

Corey David Sauer

Koo and Patricia Yuen

FRONTLINE is a registered trademark of WGBH Educational Foundation. Web Site Copyright ©1995-2025 WGBH Educational Foundation. PBS is a 501(c)(3) not-for-profit organization.

Funding for FRONTLINE is provided through the support of PBS viewers and by the Corporation for Public Broadcasting, with major support from Ford Foundation, and The Fialkow Family Foundation. Additional funding is provided the Abrams Foundation, Park Foundation, John D. and Catherine T. MacArthur Foundation, Heising-Simons Foundation, and the FRONTLINE Trust, with major support from Jon and Jo Ann Hagler on behalf of the Jon L. Hagler Foundation, and Corey David Sauer, and additional support from Koo and Patricia Yuen. FRONTLINE is a registered trademark of WGBH Educational Foundation. Web Site Copyright ©1995-2026 WGBH Educational Foundation. PBS is a 501(c)(3) not-for-profit organization.