CORRESPONDENT

Martin Smith

PRODUCED BYMarcela Gaviria

WRITTEN BY

Marcela Gaviria and Martin Smith

NEWSCASTER: Increasingly, Americans in money trouble in this bad economy are borrowing from their 401(k)s.

NEWSCASTER: The number of workers borrowing from their accounts has reached a 10-year high.

NEWSCASTER: A record number of workers now raiding their 401(k)s—

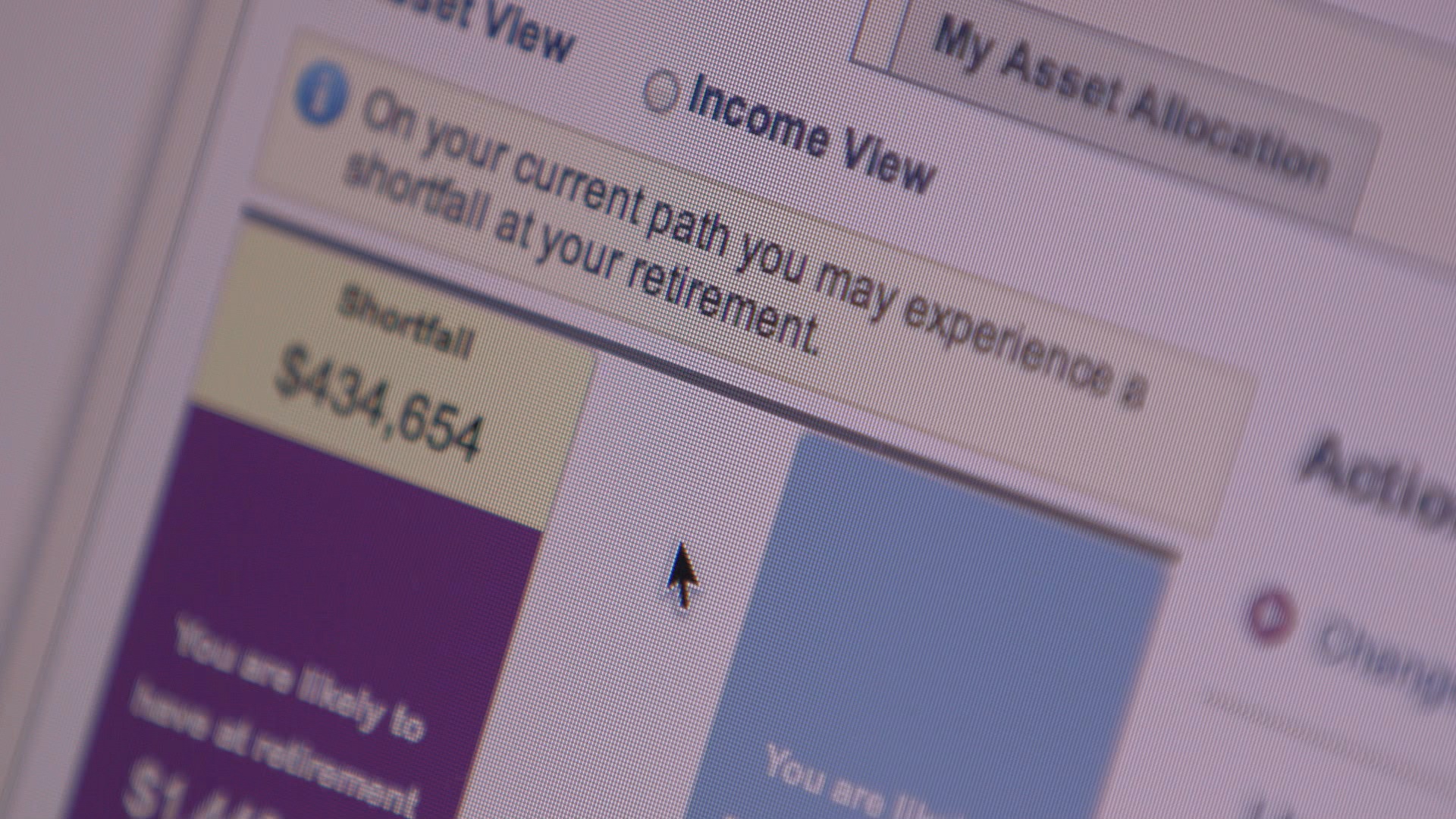

MARTIN SMITH, Correspondent: [voice-over] Let’s begin with one simple fact. America is facing a retirement crisis. And the statistics are grim.

NEWSCASTER: —tax code overhaul that could hit 401(k)s—

MARTIN SMITH: Half of all Americans say they can’t afford to save for retirement.

NEWSCASTER: The average retirement fund has lost $12,000.

MARTIN SMITH: One third have next to no retirement savings at all.

NEWSCASTER: —creating the need for many Americans to work longer and save more for retirement.

Salary: $61,000

Retirement Savings: $8,000

ROBERT HILTONSMITH, Economist, Age 31: I just don’t know if I’ll be able to save that much. God willing, Social Security will still be there. For someone like me, it’ll probably be enough to keep me out of poverty.

NEWSCASTER: The retirement fund gets sliced and diced and divvied up for Wall Street to play with.

ROBERT HILTONSMITH: I’m just going to have to somehow find a way to save 10 percent of my salary or 15 percent of my salary, which is probably what I— what I need to actually be saving to have any shot of retiring, you know, not on food stamps. Yeah. I don’t know. Hope. Hope to be able to retire.

Salary: $70,000

Retirement Savings: $115,000

CRYSTAL MENDEZ, Teacher, Age 32: Recently, I’ve started to look into how to make more money, how to increase my income while still teaching. It’s tough to really worry about retirement right now because I know it’s so far off and I know that worrying and stressing over it is an easy thing to do.

But I’m also of the mindset that as long as I don’t have too many bills or anything, too many debts, then I could essentially live off of whatever I get. I guess Plan B would be to keep working. But I’m really banking on Plan A. Otherwise, yeah, no, I don’t have a Plan B.

Unemployed

Retirement savings: $80,000

MARK FEATHERSTON, Unemployed, Age 54: It’s hard to imagine, even at this point in my life, being retired. I just don’t see it, you know, living the American dream of having your house and being able to retire. Nobody has a pension anymore. It wasn’t like it was in the ‘60s or ‘70s, where people worked for, you know, good companies and had a pension plan.

Annual salary: $70,000

Retirement savings: $20,000

LAURA FEATHERSTON, Office Manager, Age 48: I think that’s a harsh reality for a lot of people. I think— and I do think that we’ll be working until— we’ll definitely be working until our probably mid-70s, I would— if I had to make a— unless we can make up some big ground soon.

Part-time income: $25,000

Retirement savings: $500,000

BOB WOOD, Semi-Retired, Age 67: You know, I consider myself middle class. I don’t have the luxury of a couple million dollars in savings. The cost of living’s going up. Your water bill goes up, your utility bill goes up, your gas bill goes up, your food goes up. Retirees are getting stressed because their nest eggs, their savings, are not producing any income for them, so they’re all wondering where they’re going to make ends meet. I’m fortunate I can live at a higher standard because I have a little bit of a nest egg in my retirement savings. But others, they’re at poverty level.

MARTIN SMITH: As for me, I’m almost 65. I started saving for my retirement in my late 20s. But along the way, I dipped into my nest egg— not once, but several times.

[on camera] So this is my IRA and 401(k) and—

FINANCIAL ADVISOR: Which will be cleaned out over a certain amount of time.

MARTIN SMITH: Right.

[voice-over] And now, like millions of other Baby Boomers, I, too, don’t have enough.

FINANCIAL ADVISOR: The key to your retirement working out is having enough return on your assets.

MARTIN SMITH: Most of my savings went to pay for my kids’ educations.

[on camera] Well, this is where fees would really hurt you badly, as well.

FINANCIAL ADVISOR: This is where fees would hurt you badly because—

MARTIN SMITH: [voice-over] A divorce and the crash of 2008 didn’t help, either.

[on camera] It looks like my own personal fiscal cliff.

[voice-over] I’m now planning to work for as long as I possibly can.

[on camera] So this whole plan is predicated on working full-time until 70.

FINANCIAL ADVISOR: Yes.

MARTIN SMITH: And at 70?

FINANCIAL ADVISOR: From age 70 to 75, I have you working part-time.

MARTIN SMITH: [voice-over] These days, many Baby Boomers are planning to delay their retirement. Some may never stop working. It’s hard. Without knowing exactly how long you’re going to live, it’s difficult to guess how much you need to put away.

BROOKS HAMILTON, Retirement Plan Consultant: Most people seem to feel that at retirement, to be OK, you need 10 or 12 times pay, and maybe 15. So if you make $100,000 a year, you need $1.5 million to be OK. You need to save more. You need to start sooner. You can’t start work when you’re 20 or 22 and decide to get serious about this in your 40s. The boat has sailed.

MARTIN SMITH: So what can we do? Today, Americans entrust over $10 trillion to thousands of big and small financial service providers.

TELEVISION COMMERCIAL: I just bought stock. You just saw me buy stock. No big deal.

MARTIN SMITH: With expensive marketing, these companies compete for our money.

TELEVISION COMMERCIAL: You got to buy. Yes. I’m for picking. I’m for buying. Super, super strong buy.

MARTIN SMITH: But there are so many choices, it’s hard to understand.

TELEVISION COMMERCIAL: When it comes to mutual funds, it’s often hard to tell what you’re looking at.

MARTIN SMITH: Rather than a system, it’s more like a free-for-all.

HELAINE OLEN, Author, “Pound Foolish”: I don’t really see it as a real system. I see it as maybe a retirement mess, is a better word for it.

TELEVISION COMMERCIAL: Looking for real life answers to your retirement questions?

HELAINE OLEN: If you’re lucky, you have a 401(k). Roughly half of companies offer a 401(k). If you work for a small business, chances are you might— you don’t have access to such a thing. Some companies then offer other supplements. And then of course, there are things you can do on you own, like the Individual Retirement Account.

MARTIN SMITH: [on camera] So it’s entirely confusing.

HELAINE OLEN: Right.

MARTIN SMITH: [voice-over] So where does one begin?

TELEVISION COMMERCIAL: Let’s talk about that 401(k) you picked up back in the ‘80s—

MARTIN SMITH: About 60 million Americans have signed up for their company 401(k) plan.

AMERIPRISE ADVISORS VIDEO: These are your 401(k) election forms. As you can see there are numerous options to choose from. And remember, this is your retirement, so make your selections carefully.

MARTIN SMITH: But most people remember their first 401(k) meeting as dumbfounding.

AMERIPRISE ADVISORS VIDEO: Any questions?

DEBBIE SKOCZYNSKI, Computer Leasing Agent: I had no idea. I was so confused. I came out of that meeting, and I was, like, “Oh, my God.” It was just— it was overwhelming for me, the knowledge that you had to have in order to invest.

CRYSTAL MENDEZ, Teacher: I really was kind of clueless. I didn’t know what I wanted to invest in. I really didn’t know anything about it. I had learned somewhere— some— I had heard something about, if you’re young, you should be more willing to take risk. You have time. So other than that, I really knew nothing.

MARK FEATHERSTON, Former Sales Manager: They showed you the plan. You either had your choices between an aggressive investment, moderate, or conservative. You know, there was nobody there managing my money. It was all up to me.

ADVISOR: So traditional pensions don’t necessarily let you take it all in a lump sum—

Prof. TERESA GHILARDUCCI, Economist, The New School: The 401(k) is one of the only products that Americans buy that they don’t know the price of it. It’s also one of the products that Americans buy that they don’t even know its quality. It’s one of the products that Americans buy that they don’t know its danger. And it’s because the industry, the mutual fund industry, have been able to protect themselves against regulation that would expose the danger and price of their products.

MARTIN SMITH: It used to be much easier. In 1970, 42 percent of employees had a pension, a guarantee by your employer that you would get a good percentage of your salary and benefits upon retirement.

TELEVISION COMMERCIAL: This is the life. What with my retirement plan and a few dollars I’d saved, I didn’t have a thing to worry about.

MARTIN SMITH: Workers didn’t have to figure out how to manage their own savings plan. It was done for them.

ROBIN DIAMONTE, CIO, United Technologies: It was very simple. The employee really didn’t know any of the mechanics behind it. They just knew when they came close to retirement that they were promised a benefit, so a secure income over their entire life. So they had this income until they died.

MARTIN SMITH: [on camera] And so what was wrong with that system?

ROBIN DIAMONTE: Absolutely nothing, to be honest. It was a great system. The problem was that over the last decade, the rules of the game changed.

MARTIN SMITH: [voice-over] What changed was that people started living longer. New accounting rules, global competition and market volatility, too, affected the cost of maintaining a pension plan.

CHRISTINE MARCKS, President, Prudential Retirement: The old system became an expensive system, I think, from an employer standpoint. They have to know how to manage investment risk and they know how to— they have to know how to manage longevity risk.

MARTIN SMITH: [on camera] And they have to spend a good deal of money.

CHRISTINE MARCKS: And they have to spend a good deal of money. And if the market doesn’t do what they hope it will do, you know, they can lose some of the cash that they’ve actually put in from a funded status standpoint. So it’s pretty complex.

MARTIN SMITH: [voice-over] It was then that corporations found a new loophole in the internal revenue code.

HELAINE OLEN: What essentially happens is that the 401(k) comes in in the late ‘70s, early ‘80s. It starts as a corporate tax dodge, basically. It’s, if you’re a high earner, you’re going to put some of your money aside. Nobody ever thought that this was going to apply to the rest of us. I mean, there was never any thought of that.

MARTIN SMITH: So not quite by design, a new retirement system was born. Big brokerages and banks saw an opportunity to expand their business and helped employers set up and run their new plans. They promoted the arrangement as a win for everyone.

KAREN WIMBISH, Retirement Executive, Wells Fargo: From the individual perspective, the 401(k) actually opened up the opportunity to save for retirement for many individuals who worked for businesses that didn’t have a pension. And it also allowed them to have a portable, vested amount of money that they could take with them, as Americans started changing jobs more frequently.

MARTIN SMITH: [on camera] It’s as simple though, isn’t it, as the— businesses decided to get out of the business of providing pensions and shift the burden to employees?

KAREN WIMBISH: I would express that more as a sharing of the responsibility for retirement between employers and employees.

MARTIN SMITH: [voice-over] But while some employers contribute to employees’ 401(k) plans, all of the risks fall on the individual.

ZVI BODIE, Author, Risk Less and Prosper: 401(k) plans really place the burden on the individual participant to have an adequate retirement. And the vast majority of ordinary people don’t know how to do that. It’s a very complex task.

ROBIN DIAMONTE, CIO United Technologies: We wanted them to be able to figure out how much they needed to save for retirement, how to invest that money. And then once they had a lump sum, once they retired, how to withdraw the money so they didn’t outlive their assets. So that’s three different risks.

TELEVISION COMMERCIAL: Picking and choosing the right investments requires very careful handling—

MARTIN SMITH: Enter the mutual fund industry.

RON LIEBER, The New York Times, “Your Money” Column: People in the mutual fund industry realized that there was a huge opportunity here, right? I mean, not only could they sell their mutual funds, you know, directly to investors, but they could make the mutual funds the very foundation of the 401(k) plans.

MICHAEL FALCON, Retirement Exec., J.P. Morgan Asset Mgt.: In 1981, nobody knew what a 401(k) was. By 1989 it’s in the lexicon. It’s being written about. It’s being talked about. By— throughout the ‘90s, now all large employers effectively have plans in place. People are participating. It continues to grow from there.

TELEVISION COMMERCIAL: Start saving $300 a month when you’re 23, and you can retire a millionaire.

MARTIN SMITH: The boom happened in lockstep with the roaring bull market of the ‘80s and ‘90s. Mutual funds were charging high management fees, but nobody seemed to care.

ROBIN DIAMONTE: The returns were great. So no one thinks about, “How much is this costing me” when they’re earning 15 or 20 percent.

MARTIN SMITH: Star mutual fund managers like Fidelity Magellan’s Peter Lynch encouraged all of us to jump in.

PETER LYNCH, Fidelity Magellan: You shouldn’t be intimidated. Everyone can do well in the stock market. You have the skills. You have the intelligence. It doesn’t require any education. All you have to have is patience, do a little research, and you’ve got it.

MARTIN SMITH: Saving for retirement seemed as simple as betting on the market.

ZVI BODIE, Author, Risk Less and Prosper: It was a great time. Employees who participated in these plans and invested in the stock market, you know, couldn’t wait to open their monthly statements to see how much the value had gone up, you know? So things seemed to be working nicely.

BOB WOOD, Semi-Retired: Well, I was invested in everything— stocks, mutual funds, you name it. We would get monthly reports. Things were growing, everything was growing. In the ‘90s, you could not lose money in the market even if you were a dumb investor. I mean, it just kept growing and growing and growing.

NEWSCASTER: Internet stocks drove a powerful surge on Wall Street today—

NEWSCASTER: Internet stocks suddenly—

MARK FEATHERSTON, Former Sales Manager: The economy was doing great. I mean, you had all kinds of gains in the stock market. That was kind of the dot-com era.

NEWSCASTER: Internet stocks continue their meteoric rise.

MARK FEATHERSTON: You really didn’t have to pay attention to— you know, you got your statements at the end of every quarter, and you were making money.

DAN ROBERTSON, Retired Teacher: It was exciting because just gradually over time, we would have a day where we would make $7,000 or— and as much as $30,000 in a day, as it built, and even more.

STEVE SCHULLO, Retired Teacher: In 1996, we had, like, doubled our money. We had, like, $400,000, almost $500,000.

MARTIN SMITH: Steve Schullo and Dan Robertson believed they were headed for early retirement the day their portfolio topped $1 million. It was November 11th, 1999.

STEVE SCHULLO: Oh, that was a very nice day, that day, wasn’t it?

DAN ROBERTSON: What happened November 11th?

STEVE SCHULLO: See? He doesn’t— [laughs] It’s when our portfolio went over a million, silly!

DAN ROBERTSON: Oh!

STEVE SCHULLO: That was just amazing. It was like, well, yeah, this is— this is how investments work. You invest it and it grows. I mean, that’s how I thought about it.

NEWSCASTER: It was a manic Monday in the financial market—

NEWSCASTER: Stocks plunged—

NEWSCASTER: Traders are standing there, watching in amazement, and I don’t blame them!

MARTIN SMITH: But in the spring of 2000, the market collapsed.

NEWSCASTER: They’re working the phones today. A lot of their customers are freaked out!

STEVE SCHULLO: We did not know— this is our mistake. We didn’t know it was a bubble. We just didn’t know. Our portfolio had gone all the way down to where it was in 1996, from $1.5 million to $500,000.

DAN ROBERTSON: $460,000, I think.

STEVE SCHULLO: All that was gone.

MARTIN SMITH: At the height of the Internet bubble, Americans had also stuffed 19 percent of their retirement money into company stock.

ENRON SHAREHOLDERS MEETING: Should we invest all of our 401(k) in Enron stock? Absolutely. Don’t you guys agree? [laughter]

MARTIN SMITH: For savers like Debbie Skoczynski, who worked for Comdisco, a computer leasing company, the fall would be precipitous.

DEBBIE SKOCZYNSKI, Computer Leasing Agent: I was close to a half million dollars I had in my 401(k) with company stock. You know, it was, like, “Wow, look at all the money we have. Look at what is happening. You know, I can retire probably when I’m 45.”

NEWSCASTER: The dot-com failures continue to mount, especially—

MARTIN SMITH: Skoczynski not only lost her savings, she lost her job.

NEWSCASTER: Comdisco today filed for Chapter 11 bankruptcy protection, including another 200 job cuts or 10 percent—

NEWSCASTER: —joined a Who’s Who list of corporate bankruptcies—

DEBBIE SKOCZYNSKI: The day I got laid off, I lost it. I thought, “Oh, my God, I’m a single parent. I have no job. I have a house. I have a house payment. What do I do,” you know? And I was scared, really scared. [weeps] I didn’t have much of a retirement left. I couldn’t even borrow against it. And it was just something that I never foresaw, ever, you know, losing my job, ever. Never.

MARTIN SMITH: The worst was yet to come.

NEWSCASTER: Concerns about shaky home mortgages are triggering fears of a financial meltdown on Wall Street.

NEWSCASTER: Let’s talk about the speed with which we are watching this market deteriorate—

MARTIN SMITH: Eight years later, savers were hit again.

NEWSCASTER: —turmoil in the mortgage market is far from over.

NEWSCASTER: This is volatility we haven’t seen, of course, since way before you and I were born.

NEWSCASTER: More trouble ahead for the nation’s banks—

MARTIN SMITH: When the housing bubble turned into the crash of 2008, it put retirement even further out of reach.

NEWSCASTER: The economic turmoil of recent years is putting a comfortable retirement at risk for many Americans.

MARK FEATHERSTON: It was like, “Holy smokes, how do you— how do you stop the bleeding?”

LAURA FEATHERSTON: The reality of what you’ve lost is huge. I mean—

MARK FEATHERSTON: Right.

LAURA FEATHERSTON: —not only have you now lost half of your 401(k), but your house is not worth anything anymore, either. So anything that you thought you were going to have there is gone. And now half of your 401(k) is gone.

MARK FEATHERSTON: You know, if it took 13 years to accumulate $80,000 and one year to lose half of that, and then try to get that back in another 13 years, and only be at the $80,000 that you were 13 years ago?

LAURA FEATHERSTON: The math doesn’t work.

MARK FEATHERSTON: You know, the math doesn’t work.

MARTIN SMITH: Debbie Skoczynski was already in a hole, with next to nothing to cushion the blow of a second shock. And now her house was worth less than the loan she owed the bank.

DEBBIE SKOCZYNSKI: And you know, there’s some days where it’s, like, you just want to go scream, you know, in the back yard, just scream because you have your choice. Do you pay this or do you pay this?

MARTIN SMITH: Her bills were piling up. She did what a quarter of Americans have done. She dipped into what was left of her 401(k).

DEBBIE SKOCZYNSKI: I freaked out when I took the money out of my 401(k). It was hard. I mean, it’s— you know, you never— every day on the news, I’d listen to it and I’d be, like, “Oh, God, it’s really bad. Will I be able to keep my house? Will—” you know, “I— what if my car breaks down? I can’t afford a car payment.” It just can’t be this hard to make— it can’t. You know, you hear these big companies with these people taking these huge bonuses. You’re thinking, “Well, what happened to the average Joe?” They just don’t care. They made their money already.

NEWSCASTER: Growing outrage over those bonuses—

MARTIN SMITH: The year the markets crashed, Wall Street doled out $18 billion in bonuses.

NEWSCASTER: The latest bonus bombshell is sending shock waves across Washington.

MARTIN SMITH: Robert Hiltonsmith entered the workforce in 2003. He taught for a bit, worked at a coffee shop, and then went to grad school, where he ran up $40,000 in student loans.

But on the bright side, he had no savings to lose during the 2008 crash. When he graduated with a master’s in economics, he was hired at a small think tank in New York. They had a 401(k), and he began to make regular contributions.

But even in a relatively good market, he began to sense that something else was wrong.

ROBERT HILTONSMITH, Economist: I have a 401(k). I save in it. It hasn’t seemed to go up. It’s awful. I kept checking the statement and I’d be, like, “Why does this thing never go up? This is weird.” I mean, the stock market I knew was up and down but I was, like, “I still should be seeing some returns.”

MARTIN SMITH: Hiltonsmith decided to make a research project out of the subject. He began by looking at the investment options inside his 401(k) plan, 22 funds in all.

ROBERT HILTONSMITH: You know you’ve got all these names, and the names tell you nothing. It’s a balance fund. It’s— it’s a growth fund. OK, you know, it— yes, that’s lingo for certain kind of broad investment strategies, but really, what the heck does it invest in? You know, so I went through each of these— the actual fund prospectuses, which took me an exorbitant amount of time because each of these things were, you know, 50 pages long. They still wouldn’t tell you what they were doing.

MARTIN SMITH: As he dug deeper, he discovered one fund was invested in mortgage-backed securities, the kind of security that caused the collapse of the housing market.

But that’s not what worried him.

ROBERT HILTONSMITH: I was digging into all the different aspects of it, and I kept coming back to fees.

[at the computer] So here’s the first mention of fees, this “EXP ratio” right here. Why would you think that “EXP ratio” means fees?

MARTIN SMITH: Hiltonsmith found over a dozen different kinds of fees, including asset management fees, trading fees, marketing fees, record-keeping fees and administrative fees.

ROBERT HILTONSMITH: Fees when you withdraw money, fees when you take loans, fees when you actually get money out when you’re retired, which I actually didn’t even know about.

I spent a month literally going “Oh. Oh, actually, this fee is a subtype of this fee. And oh, that covers that. Or no, that’s another name for that.” It was very opaque.

[www.pbs.org: The hidden costs of fees]

MARTIN SMITH: The average actively managed mutual fund carries an annual expense of 1.3 percent. Some funds charge a fee of 2 percent, and even as high as 5 percent.

RON LIEBER, The New York Times, “Your Money” Column: That may not seem very much, right? You know, you’ve got $50,000 or $100,000. And OK, so you lose $500 or you lose $1,000 a year. That’s what you would pay to a financial advisor, right?

But if you add that up over 20 or 30 or 40 or 50 years in a 401(k) plan, all of a sudden, you’re well into the six figures as your balance grows. And that’s the difference between running out of money before you die— or having a little money left to pass on to your heirs.

JASON ZWEIG, Wall St. Journal, “The Intelligent Investor” Column: A lot of 401(k) programs are lousy. The fund choices stink. The fees are outlandishly high. And in many cases, you can take two next-door neighbors, you know, living on Maple Street in Anytown, USA, and one person is paying 10 times as much to invest in a 401(k) as the other person.

MARTIN SMITH, Correspondent: To understand this fee business, I went to talk to someone who has thought long and hard about it, Jack Bogle, the founder of Vanguard, a company that offers some of the lowest-fee products on the market. He says that if you want to improve your retirement outcome, make sure to minimize Wall Street’s take.

JOHN BOGLE, CEO, The Vanguard Group, 1974-96: Costs are a crucial part of the equation. It doesn’t take a genius to know that the bigger the profit of the management company, the smaller the profit that investors get. The money managers always want more, and that’s natural enough in most businesses, but it’s not right for this business.

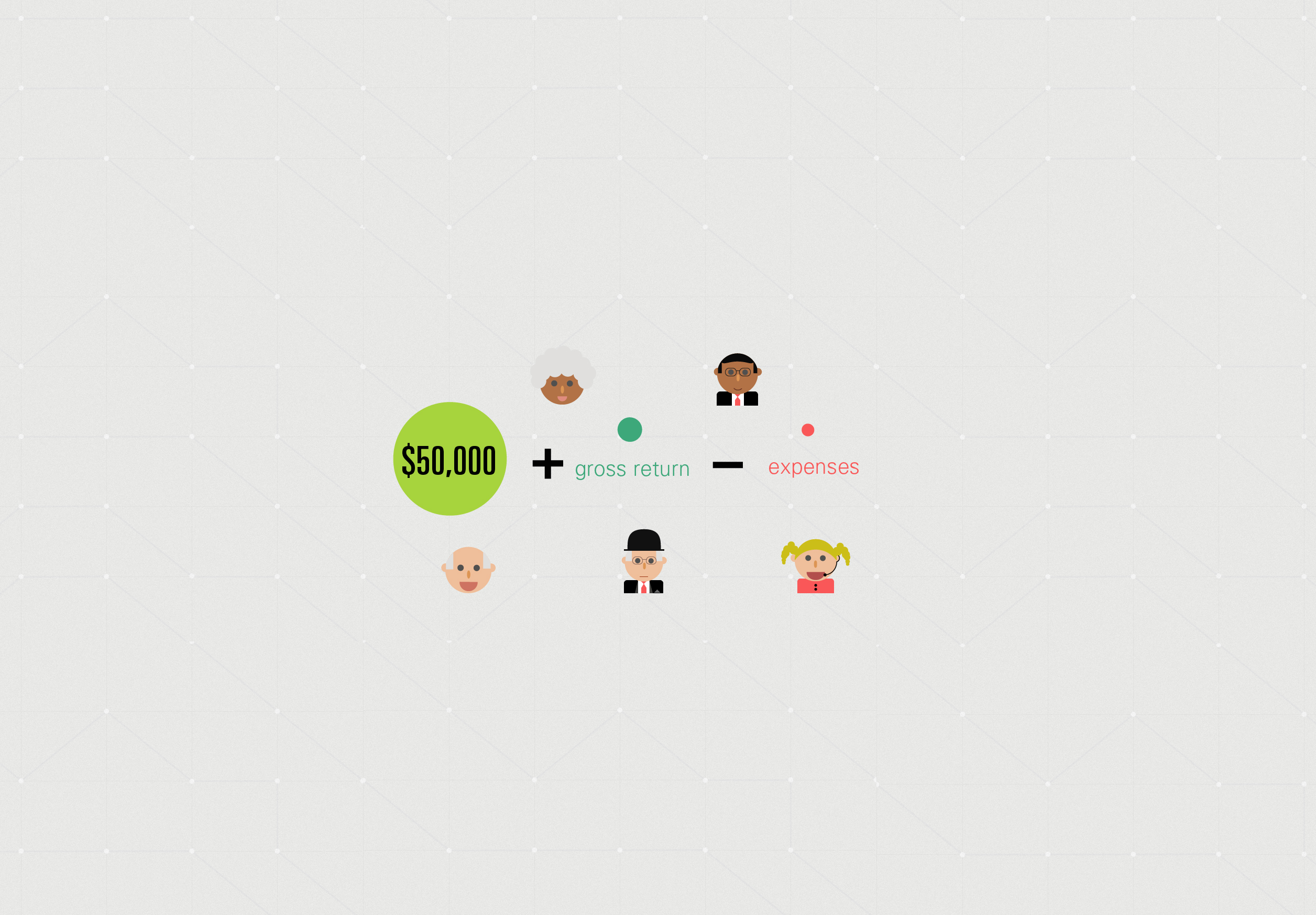

MARTIN SMITH: Bogle gave me an example. Assume you’re invested in a fund that is earning a gross annual return of 7 percent. They charge you a 2 percent annual fee. Over 50 years, the difference between your net of 5 percent — the red line — and what you would have made without fees — the green line — is staggering.

Bogle says you’ve lost almost two thirds of what you would have had.

JOHN BOGLE: What happens in the fund business is the magic of compound returns is overwhelmed by the tyranny of compounding costs. It’s a mathematical fact. There’s no getting around it. The fact that we don’t look at it— too bad for us.

MARTIN SMITH: [on camera] What I have a hard time understanding is that 2 percent fee that I might pay to an actively managed mutual fund is going to really have a great impact on my future retirement savings.

JOHN BOGLE: Well, you have to rely on somebody to get out a compound interest table and look at the impact over an investment lifetime. Do you really want to invest in a system where you put up 100 percent of the capital, you the mutual fund shareholder, you take 100 percent of the risk and you get 30 percent of the return?

[voice-over] I wanted to know how others would react to Bogle’s claims. JPMorgan Chase offers more than 100 mutual funds that charge anywhere from less than half of 1 percent to more than 2.5 percent annually.

[on camera] I want to get your reaction to an example that Jack Bogle gave us. And that is that if you invest over a 50-year investing lifetime in a mutual fund making 7 percent a year on average, but you’re paying 2 percent in fee for that, that that 2 percent will erode something like two thirds of your gains.

MICHAEL FALCON, Retirement Exec., J.P. Morgan Asset Mgt.: So the lower fees relative to an— to any given investment will always result in a higher accumulation.

MARTIN SMITH: But is his example correct? I mean, it’s— it’s shocking that you would be giving up two thirds of your—

MICHAEL FALCON: So I— so I don’t know the math behind the example that you’re—

MARTIN SMITH: But does it sound correct to you?

MICHAEL FALCON: —citing. It sounds— it sounds high.

MARTIN SMITH: [voice-over] It had sounded high to me, as well. So I took Bogle’s advice, found a compounding calculator on line and used a simple example in order to isolate the effect of fees.

Take an account with a $100,000 balance and reduce it by 2 percent a year. At the end of 50 years, that 2 percent annual charge would subtract $63,000 from your account, a loss of 63 percent, leaving you with just a little over $36,000.

Most investors are unaware of all the types of fees they’re paying. Crystal Mendez started saving for retirement in her early 20s. But she rarely looked at her account and just assumed it was doing well.

CRYSTAL MENDEZ: One day, my fiance was looking at his retirement, and he was essentially bragging about how great he was doing. So I pulled out my annual report, and we kind of compared notes. And I realized that he was doing far better than I was. He basically said, “Honey, I think you’re getting ripped off. We should look into this.”

MARTIN SMITH: After looking at the fine print, Mendez found out that not only she paying high fees, she was invested in an annuity with a high surrender fee, a penalty for any early withdrawals.

CRYSTAL MENDEZ: I think it was 10 percent was the surrender fee. So I was, like, you know, battling with myself. “Do I really want to give these people my money, or leave it there, and then I won’t have a surrender fee?” But I think, in the end, I just said, “Forget it. They can have the fee and I’ll move on with the remainder of my money.”

MARTIN SMITH: All this talk of fees made me curious about my own 401(k). I run a small company with a handful of employees. We make documentaries for FRONTLINE. But we’re too busy to look at the fine print of our retirement plan. But while putting together this report, I went on line to look at what my plan was offering.

I found what Hiltonsmith found— confusing tables of all sorts of products with different kinds of fees. I even found this offering, the American Century Livestrong Fund, a mutual fund co-branded with Lance Armstrong’s Cancer Foundation.

How did this get here? How do funds like these get into my plan in the first place?

In seeking an answer, I came across another family of fees. It works like this. In order get their offerings placed on employer 401(k) menus, mutual funds rely on brokers and plan administrators. In return, the brokers ask for a payment or revenue share.

It’s a kind of pay-to-play arrangement — or as some say, a kickback — that adds another layer of costs to retirement plans.

JASON ZWEIG, Wall St. Journal, “The Intelligent Investor” Column: A lot of people use a term like kickback because, in some ways, it is. It’s a legal kickback. There’s nothing against the law about it. But it is a sort of “You scratch my back, I’ll scratch yours” kind of arrangement. “If you sell our funds, you will get a portion of the revenue we earn from selling them through you.”

JOHN BOGLE: This is a kind of sub rosa part of this industry, and there’s not a lot of information about it. But the fact of the matter is, as far as I know, that those kind of payments to brokers for distributing your shares has simply become part of the system. You know, the brokers are getting a little religion here. They’re saying, “Why should I distribute your funds unless you pay me to? You get these big management fees, I want some of it. You’re getting plenty. Give me some.”

[www.pbs.org: More from John Bogle]

MARTIN SMITH: The problem is that these fees are not paid by the fund company. The bill is passed to you and me. Here it is, buried deep in my 401(k) plan documents. It took me about an hour to find the reference.

[on camera] Do you think the industry could do a better job of making people aware of the effective fees on their savings?

KAREN WIMBISH, Retirement Executive, Wells Fargo: I think we could make people aware of the effect of every pressure that they have on their accounts.

MARTIN SMITH: What stands in the way of doing that better job?

KAREN WIMBISH: [laughs] I— what I would tell you is, it’s— sometimes, it’s very difficult to get people to focus on something that seems complicated and dull and boring. So could we do a better job with helping consumers understand all the things that are tied to what they just bought, whether it’s financial services or the riding lawn mower? Yes. It’s too complicated.

TELEVISION COMMERCIAL: Ah, retirement. Sit back, relax, pull out the paper and— what? An article that says a typical family pays $155,000 in Wall Street fees on their 401(k)s? Seriously? Seriously! You don’t believe it—

BUSINESS SHOW HOST: It turns out the average American household will pay nearly $155,000 over the course of a lifetime in fees alone. That’s according to a new study. Here to break it all down, Robert Hiltonsmith—

MARTIN SMITH: [voice-over] In the spring of 2012, Robert Hiltonsmith came out with his study on the impact of fees on retirement savings.

ROBERT HILTONSMITH, Economist: When we looked at it, we really found that all of the costs of retirement are really being shifted onto individuals—

I was amazed. I mean, everybody covered it, all the major outlets and all of the financial industry outlets, as well, every one of them.

These really have been sold to us, these 401(k)s and IRAs, as safe products over the years and—

The point is that this system isn’t built for individuals at all. It’s certainly not built for their benefit.

NEWSCASTER: An eye-opening report out this morning, fees are taking a huge chunk out of our retirement.

MARTIN SMITH: The industry took issue with some of Hiltonsmith’s numbers, but he’d made his point.

ROBERT HILTONSMITH: We are being charged a lot by these financial firms to do not a lot, in a lot of cases.

We need something different out there. We need something simpler, something safer, you know, honestly, something that people can put their money in, get good returns, not have to worry about losing their entire nest egg, and then trust that they’ll actually be able to retire one day if they, you know, do the right thing and save enough, et cetera.

MARTIN SMITH: There is someone who has been promoting something simpler.

JOHN BOGLE, CEO, The Vanguard Group, 1974-96: [Global Ethics Summit Conference] I was criticized many years ago. Somebody said the only thing that poor guy has going for him is the uncanny ability to recognize the obvious.

MARTIN SMITH: For the past four decades, Jack Bogle has been preaching the gospel of long-term, low-cost investing through index funds.

JOHN BOGLE: Get Wall Street out of the equation. Get trading out of the equation. Get management fees out of the equation. You own American business and you hold it forever. That’s what indexing is. Own a fund that owns the entire U.S. stock market, does no trading, and has a cost of 1 percent a year to own. And that is the only way to do it. Then you’re with a creature of the market and not of the casino.

MARTIN SMITH: Index funds buy and hold a broadly diversified basket of stocks that match the holdings of a market index— the S&P 500, the Wilshire 5000, or maybe a bond or commodity index. They don’t eliminate market risk, they ride the market up and down, but they are much cheaper because there is no active manager.

JOHN BOGLE: You can guarantee to the shareholder that they will capture their fair share of the stock market’s return, for better or for worse.

If you want to gamble with your retirement money, all I can say is be my guest. But be aware of the mathematical reality. Maybe you have a 1 percent chance of beating the market over time. It has been proven right year after year after year because it can’t be proven wrong. It’s a mathematical certainty, a tautology, if you will.

[www.pbs.org: How index funds work]

MARTIN SMITH: [on camera] Jack Bogle would say, “Stop fooling yourself. You’re better off investing in a broadly diversified index fund than in actively-managed mutual funds.” What do you say to that?

MICHAEL FALCON, Retirement Exec., J.P. Morgan Asset Mgt.: I think he’s a— I’m not going to second guess him. I’m going to say that I think that there’s a role for actively managed product in the marketplace—

MARTIN SMITH: But that is second guessing him. He’s saying—

MICHAEL FALCON: OK, so I’m— so I’m second guessing Jack Bogle. I respectfully disagree. I think there’s a role for— for active management in— in portfolios. That’s— that’s my belief.

MARTIN SMITH: [voice-over] But what is that role? How well do they perform? They come with names intended to reassure every investor— growth funds, value funds, balanced funds. And they are run by seasoned professionals who are paid handsomely to manage them.

Prof. ZVI BODIE, Economist, Boston University: The question is, what are you getting for that? Are you getting superior performance? And the answer unequivocally, for the industry as a whole, is no. There’s no scientific evidence that mutual funds outperform a simple strategy of holding the market index.

JASON ZWEIG, Wall St. Journal, “The Intelligent Investor” Column: The verdict is in. It’s been in for at least a quarter century. All else being equal, you should buy the cheaper fund. And one of the ultimate dirty secrets of the fund industry is that a lot of people who run other fund companies own index funds in their— in their own accounts and don’t talk about it, I mean, unless you put a couple beers in them.

MARTIN SMITH: The evidence is overwhelming. Year after year, actively managed mutual funds fail to beat index funds. Studies have borne this out repeatedly over various time periods, in bull and bear markets.

I asked the head of retirement at Prudential, which markets dozens of actively managed funds, what she thought about this.

CHRISTINE MARCKS: Yeah, I haven’t seen any research that substantiates that. I mean, it— I don’t know whether it’s true or not. I honestly have not seen any research that substantiates that.

MARTIN SMITH: [on camera] So all the research that’s done at Vanguard that makes that argument, you’ve looked at that?

CHRISTINE MARCKS: No, I haven’t. I haven’t— I haven’t read everything. But so much of it depends on, you know, what I need is different than what you need and there’s not an asset allocation or a fund strategy that’s right for everybody.

MARTIN SMITH: I talked to one woman at the Prudential, who’s head of retirement, and asked her if she was aware of the studies that showed that index funds did better over time than the actively managed funds. And she says she wasn’t.

HELAINE OLEN, Author, Pound Foolish: That’s unbelievable. I find that actually unbelievable.

MARTIN SMITH: These people that are in the business know that the index funds do better, right?

HELAINE OLEN: They convince themselves that’s not true. When I’ve talked to these people—

MARTIN SMITH: But wait a minute. All the studies— how can they convince themselves that’s not true?

HELAINE OLEN: Because they’re convinced they’re recommending the fund that’s going to do better.

NEWSCASTER: This is not a time when you want to be buying index funds—

MARTIN SMITH: And of course, there are hot funds.

NEWSCASTER: This is not gambling, it’s investing.

MARTIN SMITH: The financial media loves them.

NEWSCASTER: —the best-performing fund U.S. stock mutual fund this year.

MARTIN SMITH: And we’re often susceptible to the lure. The problem is, as the small print says, past performance doesn’t guarantee future results.

JOHN BOGLE: Well, if only the past were prologue, it would be a great thing. Returns do not persist.

NEWSCASTER: There are some funds that are outperforming the broader market.

JOHN BOGLE: Good markets turn to bad markets, bad markets turn to good markets. So the system is almost rigged against human psychology that says if something has done well in the past, it will do well in the future. That is not true. And it’s categorically false. And the high likelihood is when you get to somebody at his peak, he’s about to go down to the valley. The last shall be first and the first shall be last.

NEWSCASTER: Last year’s dogs could actually be this year’s winners.

MARTIN SMITH: So why aren’t more of us invested in a diversified portfolio of low-cost index funds? Critics say it’s because the fund industry spends millions, hoping workers will follow their financial advice.

[www.pbs.org: Watch on line]

Prof. TERESA GHILARDUCCI, Economist, The New School: They’re hoping that the worried worker will actually trust an advisor.

TELEVISION COMMERCIAL: You have the audacity to believe your financial advisor should focus on your long-term goals, not their short-term agenda.

MARTIN SMITH: In its marketing, the industry implies that retirement advisors are on our side.

TELEVISION COMMERCIAL: So as his financial advisor, I took a look—

MARTIN SMITH: But when it comes to employee retirement plans, there are no clear standards on who can give advice.

TELEVISION COMMERCIAL: Our financial advisors are lead from a new position of strength.

MARTIN SMITH: The Department of Labor is responsible for regulating employee retirement plans.

PHYLLIS BORZI, Asst. Secretary of Labor: We have a system today where anybody can hold themselves out as an expert. They call themselves retirement planners, financial planners, advisors, et cetera. We don’t have a standard way that the consumer can figure out who has the expertise to provide advice.

MARTIN SMITH: [on camera] What’s a financial advisor?

HELAINE OLEN: That is a term that means almost nothing. It is somebody who might be a financial planner, or it could be a broker who is really a salesperson.

TELEVISION COMMERCIAL: There when you need it.

MARTIN SMITH: There are registered investment advisors, or fiduciaries, who are obligated by law to act in their clients’ best interests.

TELEVISION COMMERCIAL: Let’s talk about the cookie-cutter retirement advice you get at some places.

MARTIN SMITH: But the vast majority of so-called advisors — around 85 percent — are not fiduciaries.

TELEVISION COMMERCIAL: Selling their funds makes them more money. Which makes you wonder, isn’t that a conflict?

MARTIN SMITH: They are merely brokers or salesmen.

ZVI BODIE: A fiduciary is a professional who by law is supposed to put your interests ahead of their own. Broker-dealers are not under that obligation. They have to conform to a suitability standard, which means they can’t put you into something which is totally unsuitable for you.

RON LIEBER, The New York Times: It doesn’t have to be the best thing that you could pick out for them. It’s just something that’s suitable. It’s OK. I can’t believe that somebody would want to get into a business and then stay in the business of merely being suitable.

TERESA GHILARDUCCI: Basically, your guy is out for himself to maximize his sales, and the way he does it is to be loyal to the mutual fund. And they try to sell you the most profitable products.

MARTIN SMITH: Steve Schullo learned this lesson the hard way when he encountered someone selling financial advice in his school lunchroom.

STEVE SCHULLO: I met my salesperson in the teachers’ cafeteria. She showed us the different products. You know I didn’t know very much about investing, but in the back of my mind, way back then, “How is this person compensated” was always a question because I had worked in the private sector before I came into teaching, and I knew there were no free lunches, that nothing is free.

MARTIN SMITH: The salesperson, working on a commission basis, offered Schullo an annuity, a retirement insurance product with what he thought was a guaranteed return of 12 percent a year.

STEVE SCHULLO: So I signed up for $200 a month. And for about five years, the interest rate was going way down to 3 percent. And I was wondering, “What the heck is going’ on here? Why is it down to 3 percent?” I didn’t understand that the insurance company has the right, every year, to reset that rate as they see fit.

MARTIN SMITH: So how can you know when a financial advisor is really a salesman?

RON LIEBER, The New York Times: If you’re working with somebody who is trying to sell you financial advice, you say to them, “Are you acting in my best interest here? Would you be willing to sign a pledge that says that you’re going to act as my fiduciary at all times with all products? Because if you’re not, then I’m going to leave.” And it’s really just as simple as that.

MARTIN SMITH: Another broker sold an annuity to the Featherstons after the crash of 2008. At the time, it seemed suitable.

LAURA FEATHERSTON: This was a product that we had discussed with him, and we thought that this would insulate some of our money from what we had just gone through, what most— a lot of people had just gone through.

MARK FEATHERSTON: Right. You know, we trusted him.

LAURA FEATHERSTON: Yeah, we trusted him.

MARK FEATHERSTON: Yeah, we trusted him.

MARTIN SMITH: But the problems came after Mark got laid off and the couple had to break into their account.

LAURA FEATHERSTON: I mean, we’re talking on $7,000, the fees have been upwards of $600 just to get the money out.

MARK FEATHERSTON: I can agree paying the 10 percent penalty, you know, to Uncle Sam, but you know, these companies need to realize that they’re making money off the backs of people that have worked hard for their money. It makes you mad, but you know, what are you going to do? You’re powerless.

PHYLLIS BORZI, Asst. Secretary of Labor: [Capitol Hill testimony] He paid for advice that was not appropriate.

MARTIN SMITH: To try and hold the industry accountable, the Department of Labor proposed a new fiduciary rule in the fall of 2010.

PHYLLIS BORZI: When retirement savings are at stake, advisors should put their clients’ interests first. The critical question is what constitutes paid investment advice. The proposal we’re discussing today will amend a 35 year-old regulatory interpretation—

MARTIN SMITH: The rule would require all financial advisors to put their customers’ interests before their own whenever dealing with retirement accounts.

PHYLLIS BORZI: Today, there are trillions of dollars in each of these markets. The variety and complexity of financial products have increased and made fee arrangements far less transparent.

MARTIN SMITH: The financial services industry lobbied hard against the new rule.

Rep. JUDY BIGGERT (R), Illinois: It just seems that the financial services industry is really concerned about—

MARTIN SMITH: They got the attention of Congress.

Rep. RUSH D. HOLT (D), New Jersey: Our job here in Congress is not to preserve the business model that has existed for 35 years. But if you’re going to upset that business model, we’d better know why and we’d better know where we’re going.

Rep. TODD ROKITA (R), Indiana: We don’t need an alternative. We just don’t need to do this.

MARTIN SMITH: The Labor Department pulled back their proposal.

RON LIEBER: People in the suitability business have very good lobbyists, and they’ve done a very effective job of creating doubt in Washington and concern about how something like this would be administered, about how the fiduciary standard would be enforced, about the costs of making whatever transition you would need to make.

Rep. GEORGE MILLER (D-CA), Fmr. Chair, Education and Labor Cmte.: The full political power of the financial institutions and the mutual fund industry was completely engaged in making sure that that rule never saw the light of day.

MARTIN SMITH: [on camera] They were saying, “The rule is too tough.”

Rep. GEORGE MILLER: They were saying they don’t want any rule.

MARTIN SMITH: They don’t want to have fiduciary applied to them. They don’t want to be—

Rep. GEORGE MILLER: Because they’re not really dispensing financial advice. They’re just dispensing information and educational services, yada, yada, yada. Give me a break! They’re steering you to the funds controlled by their company. Otherwise, you might leave and go somewhere else.

MARTIN SMITH: [voice-over] I asked the head of retirement at J.P. Morgan Asset Management why anyone would want to take advice from someone not bound by a fiduciary pledge.

[on camera] Shouldn’t I want to only work with somebody who has a fiduciary obligation?

MICHAEL FALCON, Retirement Exec., J.P. Morgan Asset Mgt.: Not necessarily.

MARTIN SMITH: No?

MICHAEL FALCON: No.

MARTIN SMITH: Isn’t it better?

MICHAEL FALCON: That can— it’s different.

MARTIN SMITH: It’s not better?

MICHAEL FALCON: It can cost more. You may not get any different advice or outcome, and it can cost you more.

MARTIN SMITH: But make this simple for the investor. I sit down with somebody and they give me some advice. You say I should ask a lot of questions. I want to know whether or not one of those questions shouldn’t be whether they have a fiduciary responsibility to me.

MICHAEL FALCON: Yes, that’s a— I think that’s a very good question to ask.

MARTIN SMITH: And if they don’t?

MICHAEL FALCON: Ask them— so ask them what that means and— and see what you think about their answer.

MARTIN SMITH: Well, make it simple. Should I prefer somebody with a fiduciary responsibility?

MICHAEL FALCON: So that’s a question that can only be answered on a personal basis, based on what your level of need is, what your risk appetite is and how much of the investment decision you want to delegate. If you don’t want—

MARTIN SMITH: But this isn’t making it simple.

MICHAEL FALCON: —if— well, I wish it was simpler.

MARTIN SMITH: [voice-over] Over the past couple of decades, we’ve handed over more than $10 trillion of our retirement money to the financial services industry. They’ve built a pretty good business out of it. But how well is it working for you and me?

So far, most efforts to reform the industry have fallen flat. Recently, the government has forced some new rules on fee disclosure, and the Department of Labor says it will try to reintroduce a new fiduciary rule soon.

ROBERT HILTONSMITH, Economist: Unless there’s a game changer, unless there’s a law passed, or laws passed, or— scrap the system and start over, as I advocate oftentimes, no, nothing’ll change because there’s no incentive for the market to change. People will just keep on saving because it’s the only option they’ve got. And companies will keep on raking in the profits.

MARTIN SMITH: So saving for retirement remains a bewildering and frightening challenge for millions of Americans. For the people we met in making this program, the outcomes are mixed. Some are confident.

CRYSTAL MENDEZ: I definitely couldn’t retire right now. But the fact that I’m planning ahead, and you know, investing wisely is— is, hopefully, you know, going to help. And I— I don’t think I’ll run out of money.

BOB WOOD: I am concerned about running out of money. But I’m a survivor, and if I have to downsize into a tent, I will.

STEVE SCHULLO: The retirement dream, I mean, we— we’re living it right now.

DAN ROBERTSON: This is it.

STEVE SCHULLO: This is it. You know, it’s— life gives you these opportunities. We never planned to learn about investments until we got slammed in the gut. Then, “Oh, we better start paying attention here.”

MARTIN SMITH: Others are worried.

DEBBIE SKOCZYNSKI: I’m leery. I’m really, really leery. I don’t know what I’m going to do. I feel like I’ll be working for the rest of my life, absolutely for the rest of my life.

MARK FEATHERSTON: It’s hard to imagine, even at this point in my life, being retired. I just don’t see it.

LAURA FEATHERSTON: Yeah, I just don’t see it, either.

MARK FEATHERSTON: I don’t see it.

ROBERT HILTONSMITH: My retirement plan is fingers crossed and pray, basically. Yeah, win the lottery, hope my dad has more money than he does. And the truth is, just going to have to find a way to save way more than you should have to.

MARTIN SMITH: Meanwhile, what about Hiltonsmith’s research? He is now finishing his Ph.D. dissertation on America’s retirement crisis, but the grant money he needs to support his continuing work has dried up.

As for me, over the last several months, I’ve spent a lot of time playing with different on-line retirement calculators. Some were optimistic, others very discouraging.

I will keep working.