PRODUCED BY

Martin Smith

CO-PRODUCED BY

Linda Hirsch

Ben Gold

WRITTEN BY

Martin Smith

NEWSCASTER: Although this downturn started in the housing sector and in the financial sector, you’re seeing a lot of things being hit.

NEWSCASTER: Today’s numbers suggest job losses are accelerating—

NEWSCASTER: Almost six hundred thousand jobs—

NEWSCASTER: That’s the biggest loss since 1974.

NARRATOR: In 2009, Wall Street bankers were on the defensive. The great American mortgage bubble had burst—

NEWSCASTER: This is a huge amount of money.

NARRATOR: —the economy was in ruins, and Wall Street bankers were being blamed. Bankers admitted they had miscalculated.

NEWSCASTER: —crippled the U.S. economy—

NARRATOR: But they were also worried they could be held criminally liable for fraud. With a new administration arriving in Washington, bankers and their attorneys expected investigations and at least some prosecutions.

NEWSCASTER: —$150 billion in mortgage-backed securities—

MARTIN SMITH, Correspondent: [on camera] Was there a sense that there were going to be prosecutions of alleged fraud related to the mortgage crisis?

DAVID BOIES, Boies, Schiller & Flexner: I think there was that expectation. I think people had seen the financial crisis. There was obviously a lot of conduct that had gone on that was improper, and I think people were expecting to see some substantial prosecutions.

Sen. TED KAUFMAN (D-DE), 2009-10: The men and women who duped would-be home owners, who defrauded the American investor, need to identified, prosecuted, convicted and thrown in jail.

NARRATOR: In Washington, there was broad support for prosecuting Wall Street.

TED KAUFMAN: I was really upset about what went on on Wall Street that brought about the financial crisis, not only destroyed the financial— almost destroyed the financial system of the United States, almost destroyed the financial system of the world. That doesn’t happen if there isn’t something bad going on.

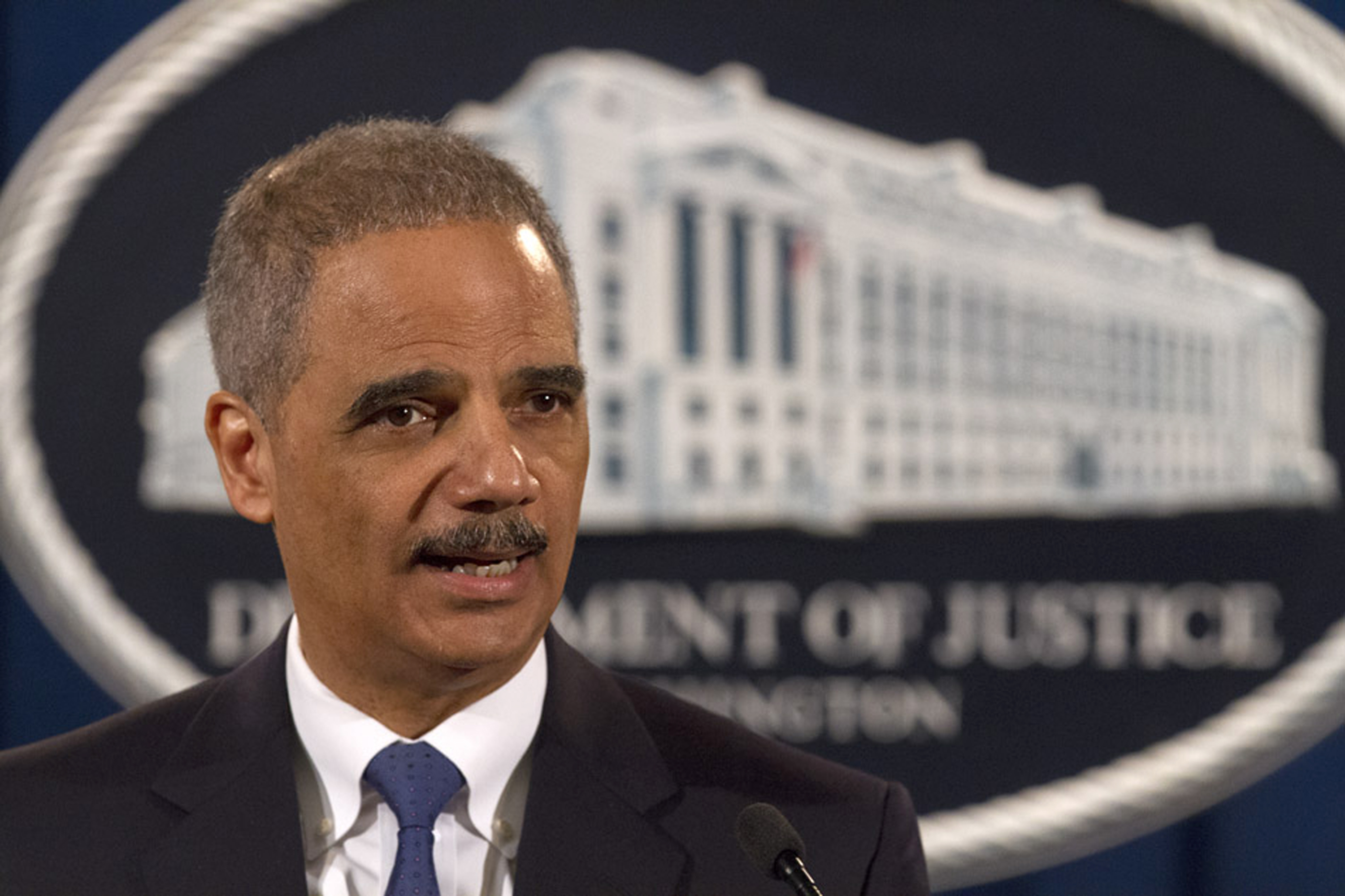

NARRATOR: But today, more than four years since the financial crisis of 2008, there have been no arrests of any senior Wall Street executives. Chief of the Criminal Division at Justice Lanny Breuer says the problem is that greed is not necessarily criminal.

LANNY BREUER, Head of Criminal Division, Justice Dept.: I am personally offended by much of what I’ve seen. I think there was a level of greed, a level of excessive risk taking in this situation that I find abominable and I find very upsetting. But that is not what makes a criminal case. What makes a criminal case is that I can prove beyond a reasonable doubt every element of a crime.

Twitter #frontline

NARRATOR: Some former prosecutors believe the problem is a lack of effort.

ELIOT SPITZER, Attorney General, NY, 1999-06: The Justice Department failed. They have not done what needed to be done. They didn’t ever try to bring together one coherent narrative, laying out the entirety of the story against one of the major players and demand sanctions that are meaningful. That to me is what has been fundamentally lacking.

NARRATOR: The story of how the big banks amassed enormous fortunes packaging home loans into securities and selling them to investors all over the world began, of course, on the ground with mortgage originators.

MICHAEL WINSTON, Managing Director, Countrywide, 2005-08: [presentation] What my Econ 1 prof taught us was business goes in cycles—

My name is Michael Winston. I worked for Countrywide Financial Corporation from 2005 until 2008. They said their goal was world-class, Goldman Sachs on the Pacific. And they wanted me to realize their vision.

[presentation] See now if you can reach up-with both fists—

NARRATOR: Michael Winston once lived inside the bubble at mortgage originator Countrywide. At first, Winston was impressed by CEO Angelo Mozilo and how he had turned Countrywide into America’s number one mortgage company. But just a few months into the job, Winston had an encounter in the company parking lot.

MICHAEL WINSTON: I’d been there five months when I happened to park next to a car with personalized vanity plates. And the personalized plates said, “Fund ‘em.” And I had a conversation with the person nearest the car. I didn’t know if it was the owner or just some guy walking by. And I just said, ” ‘Fund ‘em’, that’s an interesting plate. What do you suppose that means?” And he said, “That’s Angelo Mozilo’s growth strategy for 2006.”

ANNOUNCER: [Countrywide TV commercial] Low cost refi—

MICHAEL WINSTON: And he said, “We have a loan for every customer.”

ANNOUNCER: [Countrywide TV commercial] A growing family with a lot of debt—

MICHAEL WINSTON: And I said, “A loan for every customer? How can that be?”

ANNOUNCER: [Countrywide TV commercial] —a business owner whose income was hard to document—

MICHAEL WINSTON: “What if the person doesn’t have a job? “Fund ‘em,” the— the guy said. And I said, “What if he has no income?” “Fund ‘em.” “What if he has no assets?” And he said, “Fund ‘em.”

ANNOUNCER: [Countrywide TV commercial] One of them was turned down for a home loan by three different lenders. I’m with Countrywide, and I got them all approved.

MICHAEL WINSTON: I said, “I’m confused. What are the standards you use, the criteria against which you make lending decisions?” And the guy looked at me, smiled smugly and said, “If they can fog a mirror, we’ll give ‘em a loan.”

CHRISTOPHER CRUISE, Loan officer trainer, 1990-2008: My name is Christopher Cruise. I was a trainer of mortgage loan originators throughout the country.

There was a Plano, Texas office in Countrywide, and people would sidle up to me saying, “You wouldn’t believe what’s happening around here. You wouldn’t believe the loans I’ve been getting approved here.” They were just flabbergasted at— at what would— what was going through the pipeline.

[presentation] These are still on the books. Did you know that?

NARRATOR: Christopher Cruise describes an industry driven to loosen its standards by demand from New York.

CHRISTOPHER CRUISE: You got the sense that Wall Street was in control of underwriting standards, and not the mortgage industry.

MARTIN SMITH: What do you mean?

CHRISTOPHER CRUISE: Well, if the underwriting was acceptable to Wall Street, if the underwriting was acceptable to the ratings agencies, that’s all that counted. And so my sense is it was probably a game among the people in the mortgage business to say, “Let’s come up with one of the worst loans we could possibly imagine and see if Wall Street will buy it.”

NEWSCASTER: New homes are selling at the second highest rate on record, and—

CHRISTOPHER CRUISE: And then that type of mentality translates into, “Don’t worry about whether the documents are valid. Don’t worry about whether we can verify income. Don’t worry if the appraisal is any good. Just worry about getting the damn loan closed because if you can get that closed, we can get that securitized and then turn around and do another loan. Don’t worry about it. There’s too much money out there. Just get the loan closed.”

NEWSCASTER: —doled out $36 billion in bonuses this year—

TED KAUFMAN: This is totally about what went on on Wall Street. Was, in fact, Wall Street going out into California and saying, “Hey, just put the mortgages together. Don’t worry whether they’re good or not. You get a fee. I’ll take them. I’ll bundle them up. I’ll sell them off to somebody else. I’ll make my money on that. And whatever happens to the mortgages doesn’t really matter.”

NARRATOR: Even during the bubble years, the Department of Justice had arrested and prosecuted many small mortgage brokers, loan appraisers and even home buyers. But to go after Wall Street bankers would prove to be much harder.

MARTIN SMITH: The Justice Department has indicted something like 2,000 to 3,000 people that were making the loans, the loan originators.

CHRISTOPHER CRUISE: Right. Shooting fish in a barrel, that’s what that is.

MARTIN SMITH: No bankers have gone to jail. Does that surprise you?

CHRISTOPHER CRUISE: No, it doesn’t surprise me.

NARRATOR: To prosecute Wall Street, investigators needed to find proof of what the bankers knew and what they intended. This meant identifying people on the inside who were willing to talk.

ELIOT SPITZER: I’ve always believed that you start at the bottom up at a bank. You start at the credit department. Go to the credit department. Find out what the credit department knew. Those are the guys who wear green eyeshades, who don’t get the big bonuses, who want to make sure that the loans, the underwritings, are legitimate. They actually crunch the numbers. They’re the ones who send the memos up to the folks who get the big bucks. How the folks at the top react to those memos is what determines whether the bank acts properly.

NARRATOR: At the big investment banks, the credit departments hired contractors known as due diligence underwriters.

TOM LEONARD, Due diligence underwriter, 2002-07: My name is Tom Leonard. I was a due diligence underwriter

EILEEN LOIACONO, Due diligence underwriter, 2005-07: My name is Eileen Loiacono and I was a contract underwriter.

CHICO MORTON, Due diligence underwriter, 2006-08: My name is Chico Morton and I was a due diligence underwriter.

MARTIN SMITH: What does a due diligence underwriter do?

CHICO MORTON: A due diligence underwriter assesses the risk of buying loan portfolios. So a company from Wall Street, they’re going to buy a loan pool or a portfolio of loans, and we would be hired to go in and take a sample of the loans and review them.

MARTIN SMITH: So you were contract workers?

TOM LEONARD: Yes.

MARTIN SMITH: And then what would you do? How would you go about doing the due diligence?

TOM LEONARD: Well, we would travel to the location where the loans were stored. And we’d have a room, either a hotel room, a conference room, or some workroom where we could set up tables and our laptop computers.

MARTIN SMITH: So these loans would come in in banker’s boxes?

TOM LEONARD: Yes. A lot of times, we were doing the manual labor of moving the boxes of loans back and forth— load all these boxes on vans and drive them to the hotel, unload them at the hotel, into the room where the due diligence underwriters were working. And they could be stacks all the way up to the ceiling and there could be anywhere from 10 to 20 separate mortgages within each banker’s box.

CHICO MORTON: Thirty underwriters crammed at a table, you know, bumping shoulders. And you know, sometimes, we’re in there 6:30. Sometimes we’re out at 10:00, 11:00, 12:00 at night. I’ve been on jobs where we worked late.

MARTIN SMITH: And so what was it like? What was the atmosphere like?

EILEEN LOIACONO: It was like a party. You know, we were all in hotels together, so you know, it was definitely a party atmosphere. We were getting through these loans as quick as we can. They were not being looked at like they should’ve been looked at.

TOM LEONARD: It wasn’t uncommon to have an underwriter on one side of the room start to laugh and say, you know, “Hey, get a load of this,” you know? “Here’s a guy that’s moving from $500 a month in rent to a $650,000 house, and he’s an electrician and his wife is a waitress,” ha, ha, ha, everybody in the room laughing. Somebody else would have another story.

CHICO MORTON: A school teacher making, you know, $10,000 a month, or a waitress making, you know, $12,000 a month. You’re supposed to exercise some common sense, and you know, like, say, “OK, well, is it reasonable that they could make XYZ a month?” But a lot of times, we didn’t do that.

MARTIN SMITH: You didn’t do that, on the instruction of your supervisor, your lead?

CHICO MORTON: Right.

MARTIN SMITH: So the lead would say what?

CHICO MORTON: “Looks reasonable to me.” [laughs]

MARTIN SMITH: The lead would say, “That waitress making $12,000 a month looks reasonable to me?”

CHICO MORTON: Yeah.

MARTIN SMITH: You’re kidding.

CHICO MORTON: Well, depending on the area. You know, if it’s—

MARTIN SMITH: What area does a waitress make $12,000 a month?

CHICO MORTON: Las Vegas. You know, if it’s Vegas, then, you know, possibly with tips and all that stuff, or—

MARTIN SMITH: I can’t do the math, but that sounds pretty high.

CHICO MORTON: [laughs] Right. It is high.

EILEEN LOIACONO: You couldn’t say the word “fraud” because we couldn’t prove that it was fraud.

MARTIN SMITH: Well, if you saw something that was a misrepresentation, you were expressly told, “Don’t write ‘fraud’ or mention— use the word ‘fraud’?”

EILEEN LOIACONO: All the time. Even if we suspected, we had to say, “This appears to be incorrect.” You would never say, “This looks fraudulent.”

MARTIN SMITH: Were you told to ignore loans that you clearly knew contained fraud?

TOM LEONARD: Well, fraud— in the due diligence world, fraud was the F-word or the F-bomb. You didn’t use that word.

MARTIN SMITH: Even if a loan was clearly— a stated income loan that made no sense, there was no support for—

TOM LEONARD: Yeah, but you didn’t use the word “fraud” when you—

MARTIN SMITH: But it was fraud. You saw loans that—

TOM LEONARD: By your terms and my terms, yes, it was fraud. By the due diligence terms, it was something else.

NARRATOR: And it wasn’t just outside contract underwriters who were finding fraud. Insiders at the big banks were finding problems.

RICHARD BOWEN, Sr. VP & Chief Underwriter, CitiGroup, 2002-09: My name is Richard Bowen. I was with CitiGroup and I was a senior vice president and business chief underwriter in the commercial lending group. And the overall operations I had purview over involved about $90 billion a year of mortgages we were purchasing from other mortgage companies.

MARTIN SMITH: And what were you to do with those $90 billion worth of mortgages?

RICHARD BOWEN: I had responsibility to make sure that those mortgages met our credit policy guidelines.

MARTIN SMITH: So the bank had agreed to buy these loans—

RICHARD BOWEN: Subject to their meeting our credit policy.

MARTIN SMITH: But you found out that the loans that your team was looking at didn’t meet the credit policy.

RICHARD BOWEN: We found that approximately 60 percent of the loans did not meet our policy.

MARTIN SMITH: Sixty percent?

RICHARD BOWEN: Sixty percent, yes.

MARTIN SMITH: Sixty percent of the loans didn’t meet the—

RICHARD BOWEN: Our policy.

MARTIN SMITH: —your policy.

RICHARD BOWEN: Yes. And the volumes increased through 2007, and the rate of defective mortgages increased from 60 percent to in excess of 80 percent.

NARRATOR: On November 3rd, 2007, Bowen wrote an email to four senior CitiBank executives, including board chairman and former Secretary of the Treasury, Robert Rubin. “Since mid 2006, I have continually identified breakdowns in internal controls. I must now communicate these concerns. I am deeply distressed.”

RICHARD BOWEN: I actually included in that e-mail my cell phone, told them I was available this weekend, to please call me. And in that e-mail, I also requested an outside investigation. And in December, I sent another e-mail and I said, “Please contact me. You need to know the details behind this. There are risks to the company.”

NEWSCASTER: Just a few months ago, they were giants, but now they need rescue.

NARRATOR: There were risks to the entire country.

NEWSCASTER: —simply too big to fail.

NARRATOR: By 2008, highly-leveraged banks stuffed with bad loans began to fail.

NEWSCASTER: —bailing out Bear Stearns…that business is gone

MARTIN SMITH: What did you think when Bear Stearns went down?

CHICO MORTON: I couldn’t believe it. Like, I thought the whole banking system was about to go down.

NEWSCASTER: 158-year-old Lehman Brothers filed for bankruptcy—

NARRATOR: It almost did. Billions drained from the economy overnight. The party was over.

NEWSCASTER: —in July and said everything was great. And off that, a lot of people bought stock—

TOM LEONARD: Bill O’Reilly was having a temper tantrum on his show, where he was going off about, you know, “Why didn’t I hear about this? Why didn’t somebody tell me about all this that was going on?”

BILL O’REILLY, Fox News “The O’Reilly Factor”: This industry— 90 percent! Ninety percent!

TOM LEONARD: And I almost threw my shoe through the television set.

BILL O’REILLY: We just heard the words! Look, stop the BS here!

TOM LEONARD: And I was screaming and yelling, “I did try to let you know,” because he had been one of the ones that I had sent e-mails and never received any response.

NEWSCASTER: Millions of American taxpayers are still wondering, how did we get ourselves into this economic mess, and is there someone truly to blame?

Pres. BARACK OBAMA: Hello, everybody.

NARRATOR: To help prosecute those who were to blame, President Obama signed a new bill.

Pres. BARACK OBAMA: Four months ago today, we took office amidst unprecedented economic turmoil—

NARRATOR: It was designed to amend America’s fraud statutes—

Pres. BARACK OBAMA: —sign the Fraud Enforcement and Recovery Act—

NARRATOR: —to make prosecution easier and also to increase funding for the SEC, the FBI and the Department of Justice.

NEWSCASTER: Senator Ted Kaufman is a Democrat from Delaware, the man who now holds the seat vacated by Vice President Joe Biden—

NARRATOR: Senator Ted Kaufman was a co-sponsor of the bill. He was an unusual senator.

NEWSCASTER: When this particular term is up, what are you going to do?

Sen. TED KAUFMAN (D-DE): Oh, I’m going to leave. I would never run for office.

NARRATOR: Appointed to replace Senator Joe Biden, he had taken no campaign money and was beholden to no lobbyists.

Sen. PATRICK LEAHY (D-VT), Judiciary Committee Chairman: I want to see people who have committed such fraud and the havoc, it’s caused this country— frankly, I want to see them go to jail.

NARRATOR: In early 2009, Kaufman joined his colleagues on the Senate Judiciary Committee to discuss bolstering the FBI and Justice Department’s financial crimes units.

Sen. CHARLES GRASSLEY (R), Iowa: I’m going to ask some questions to each of you—

My feeling and Senator Leahy’s feeling is that, you know, if you’re going to stop crime, the best way is to punish crime, and the best way to do that is to put people in jail.

Sen. PATRICK LEAHY: Senator Kaufman?

NARRATOR: Senators were surprised by how unprepared the government was to investigate Wall Street.

TED KAUFMAN: The deputy director of the FBI gave incredible testimony.

JOHN PISTOLE, Dpty. Director, FBI, 2004-10: After 9/11, we moved almost 2,000 criminal investigative resources over to national security matters.

TED KAUFMAN: He said what happened was that the government had transferred a great deal of the FBI agents over to anti-terrorism, but they didn’t replace them. So we’re basically down to 200 FBI agents.

JOHN PISTOLE: We have about 240 agents—

TED KAUFMAN: And what he said was, essentially, during the savings and loan crisis, there were 1,000 FBI agents working on fraud.

NEWSCASTER: Charles Keating, the millionaire banker who was—

NARRATOR: After the S&L crisis of the ‘80s, the government responded forcefully. Back then, Justice convicted over 1,000 bankers, a third of them top executives.

NEWSCASTER: —loan scandal, was led off in handcuffs today.

NARRATOR: In the wake of the financial crisis of 2008, Kaufman wanted the government to respond as it had in the past.

Sen. TED KAUFMAN: We should find them, and if they’re guilty of a crime, they should go to jail.

NEWSCASTER: Why should people hearing you have any confidence that there will be serious investigations and serious penalties to some of the biggest and most powerful people in corporate America?

Sen. TED KAUFMAN: Trust me, it’s going to happen.

NARRATOR: Kaufman became front man for the new fraud enforcement bill.

JEFF CONNAUGHTON, Chief of Staff, Sen. Ted Kaufman, 2009-10: Ted began giving speeches and writing op-eds about how important it was. You know, we came up with this sort of slogan that, you know, when people rob a bank, they know they’re going to go to jail.

Sen. TED KAUFMAN: If somebody robs a store, they get caught, they go to jail. If somebody robs hundreds of millions of dollars, they should go to jail.

JEFF CONNAUGHTON: When bankers rob people, they should know they’re going to go to jail.

Sen. TED KAUFMAN: Commit a big crime, go to jail for big time. These people should go to jail.

Sen. TED KAUFMAN: Lots of people on Wall Street said, “What are you doing? You’re trying to destroy the banks. There’s no crime up here. We didn’t commit any crimes. There’s no reason to come up here and start talking about crimes. Plus, we’re very, very fragile. And you know, something could happen if, in fact, you start talking about crime,” which was just totally, completely…ridiculous.

[www.pbs.org: More from Ted Kaufman]

NARRATOR: There was one case already in the pipeline. It had been started under the Bush administration and involved two Bear Stearns hedge fund managers charged with deceiving investors. It was seen as a test case.

ELIOT SPITZER, Attorney General, NY, 1999-06: Aha! Finally, we’re beginning to see the criminal cases that will evidence a determination by the Justice Department to bring to justice those individuals who misled the public, who misled investors, who, knowing that an investment was bad, still said it’s good.

NARRATOR: At first, prosecutors were optimistic.

Judge FREDERIC BLOCK, Fed. District Court, Eastern District of NY: The kneejerk reaction when this case was brought was that since people were incensed about what was happening with the economy, it would be a simple type of prosecution. I think there was that general perception.

EDWARD LITTLE, Attorney for the Defense: And so they figured that they’d have an easy conviction. And you know, I mean, I think they believed in what they were doing. I’m not going to say they were malevolent. But they were naive.

NEWSCASTER: Documents unsealed by prosecutors—

NARRATOR: It wasn’t the strongest case.

NEWSCASTER: The government says that the emails are direct evidence—

NARRATOR: With no whistleblowers talking, prosecutors had to rely on the interpretation of a few emails.

NEWSCASTER: —no way for us to make money ever—

NARRATOR: Eighteen Wall Street defense attorneys went to work, and after a three-week trial, the government failed to convince a jury that the hedge fund managers were guilty.

NEWSCASTER: —not guilty of charges that they defrauded investors.

MARTIN SMITH: Were you surprised by the outcome of the Bear Stearns hedge fund managers’ case?

DAVID BOIES, Boies, Schiller & Flexner: I was a little surprised, but I wasn’t shocked. These are hard cases to win.

MARTIN SMITH: Was the Justice Department wrong to go after those two guys?

DAVID BOIES: No, I thought that that was a reasonable case for the government to bring. Now, the fact it’s a reasonable case to bring doesn’t mean you’re always going to win.

ELIOT SPITZER: The acquittal in that case left many of us feeling a little empty.

NEWSCASTER: That’s got to put a big wrench in the government’s prosecution scheme—

ELIOT SPITZER: There was a definite sense that Justice backed off and that they became timorous when it came to making the cases that would really have gone to the heart of what did happen in the crisis of ‘08.

NARRATOR: Senator Kaufman was worried. He wanted to make sure that Justice wouldn’t shy from the next opportunity and that the money Congress had appropriated would not go to waste.

JEFF CONNAUGHTON: Ted said to Chairman Leahy, “I would like to chair an oversight hearing to ensure that these funds are being spent effectively.”

GEOFF MOULTON, Chief Counsel, Sen. Ted Kaufman, 2009-10: We met with Lanny Breuer, who was the head of the Criminal Division. We met with Rob Khuzami, who was head of enforcement for the SEC. We met with a senior deputy in the FBI, Kevin Perkins.

JEFF CONNAUGHTON: We sat down and we sort of got down to business. And Ted said “Chairman Leahy has asked me to hold an oversight hearing that will provide me with a public forum to explore,” you know, “just what you’re doing on this front of investigating Wall Street.” Well, that certainly got their attention.

TED KAUFMAN: They started telling me about— about this great thing they had out in California, this web to catch the mortgage brokers who had given out the loans. And we made it clear to them, I made it clear to them, that absolutely, positively I don’t— I’m not— this is not about LA. This is totally about what went on on Wall Street. That’s what the bill say and that’s what the emphasis is.

JEFF CONNAUGHTON: We said, you know, “Don’t just come back here a couple of years from now and say, you know, ‘Look at all the small fry we— we nailed to the wall.’ You know, we’re talking about also investigating senior-level people at Wall Street firms, even at the board level.”

GEOFF MOULTON: I think we might have been a little bit concerned at this meeting that— that the FBI wasn’t necessarily at that point — this is now fall of 2009 — aiming high enough.

NARRATOR: Shortly before the hearing, the Justice Department made an announcement.

ERIC HOLDER, Attorney General of the United States: President Obama has established the Financial Fraud Enforcement Task Force to investigate and to prosecute fraud and financial crime.

TED KAUFMAN: This is the value of oversight hearings. A week before our hearing, they announce the fraud task force.

ERIC HOLDER: And we will not hesitate to bring charges, where appropriate, for criminal misconduct.

TED KAUFMAN: Somebody had to come to that hearing and talk about what they were doing, and so that was the impetus. I am convinced to the day I die that the only reason that fraud task force was announced at that point was because somebody had to go to the hearing.

Sen. TED KAUFMAN: Mr. Breuer, last month we saw a jury acquit the two Bear Stearns hedge fund managers. Are there lessons we can learn from that, is was that just a one-off?

LANNY BREUER: I’m a big believer in the jury system, and juries are going to do what juries feel are right. These are tough cases, but we’re going to continue to bring them. It’s not a deterrence at all. We’re marching forward.

GEOFF MOULTON: One of the things that oversight hearings do is it holds folks’ feet to the fire. We wanted to get them to say what they could in public that paralleled what they had said to us in private.

Sen. TED KAUFMAN: Why haven’t we seen more, you know, boardroom prosecutions?

LANNY BREUER: Senator, these are complicated cases. Don’t for a moment think that they’re not being pursued and investigated.

KEVIN PERKINS, Associate Deputy Director, FBI: —from Main Street to Wall Street and beyond.

ROB KHUZAMI, Dir. Div. of Enforcement, SEC: We are focused on that, and we will bring the cases where we— where it’s appropriate.

MARTIN SMITH: Isn’t this a bit of theater? I mean, they had the questions in advance.

JEFF CONNAUGHTON: Well, I thought it was fair theater because, you know, we were asking tough questions.

Sen. TED KAUFMAN: If we come back a year from now and we’re having this hearing, how much progress do you think we’ll have made on—

JEFF CONNAUGHTON: I do think it served a purpose. I mean, do I wish we had been even more aggressive? Yes. But we were willing to give them the benefit of the doubt. And we felt like, “OK, let’s sit back and let them do their jobs.”

NARRATOR: But over the next year, it would be others, not the Justice Department, who put bankers on the witness stand.

LLOYD BLANKFEIN, Chairman and CEO, Goldman Sachs: We are audited and reviewed and subject, and we have due diligence practices—

PHIL ANGELIDES, Chmn., Financial Crisis Inquiry Comm.: Was your due diligence adequate?

NARRATOR: Beginning in January 2010, a fact-finding commission established and funded by Kaufman’s Fraud Enforcement and Recovery Act held a series of public hearings.

JAMIE DIMON, Chairman and CEO, JPMorgan Chase: In mortgage underwriting, somehow we just missed, you know, that home prices don’t go up forever.

PHIL ANGELIDES: We held 19 public hearings. We reviewed millions of pages of documents — corporate documents, regulatory documents — most of which had never seen the light of day.

Mr Bowen?

RICHARD BOWEN, Sr. VP & Chief Underwriter, CitiGroup, 2002-09: Thank you, Mr. Chairman. I witnessed business risk practices which made a mockery of Citi credit policy.

PHIL ANGELIDES: You take a organization like CitiGroup, for example, people involved in due diligence like Richard Bowen signaled up the line all the way up to Robert Rubin that something was wrong, that they were finding that some 60 percent of mortgages they were buying weren’t meeting their standards.

Mr. Bowen sent you an email—

NARRATOR: In one exchange, the commission asked CitiBank’s Robert Rubin to respond to Bowen’s email.

PHIL ANGELIDES: Did you ever act on that?

ROBERT RUBIN, Fmr. Senior Adviser, Director, CitiGroup: Mr. Chairman, I do recollect this, and that— either I or somebody else— and I truly do not remember who, but either I or somebody else sent it to the appropriate people—

MARTIN SMITH: Rubin told Angelides that actions were taken to improve the bank’s due diligence operations. But his recollections were vague.

ROBERT RUBIN: I certainly don’t remember today whether I knew at the time or not— I honestly— I truly do not remember—

PHIL ANGELIDES: If the excuse at the top was, “We didn’t know,” that’s a pretty poor excuse from people who are hauling down $10 million, $20 million, $30 million, or in Robert Rubin’s case, $115 million.

NARRATOR: Bowen was demoted and eventually left the bank. But later, CitiGroup admitted wrongdoing in a civil fraud suit for failing to perform basic due diligence between 2004 and 2010.

Another focus of the commission was the work of a due diligence company named Clayton Holdings.

PHIL ANGELIDES: You know, one piece of information that we released were documents from Clayton Holdings, who performed due diligence for two dozen banks who were buying mortgages from the Countrywides, the Ameriquests, the New Centurys, packaging those loans up and selling them to investors.

And if you look at those documents, what they show is in each of these banks, Clayton Holdings was finding that a substantial portion of the loans did not meet the standards of the bank buying those loans. And bank after bank after bank, they took those loans, they knew they were defective, and notwithstanding that, they never told the investors. In fact, they told investors quite the opposite.

So if you look at that pattern of behavior, I think it raises very serious questions about whether this is criminal conduct.

NARRATOR: This was among several referrals the commission made to the Justice Department for further investigation. We asked chief of the Criminal Division, Lanny Breuer, why such referrals hadn’t led to charges.

LANNY BREUER: I can’t really talk about any specific case, but Phil Angelides and I have had very direct and very good conversations. But in reality, in a criminal case, we have to prove beyond a reasonable doubt — not a preponderance, not 51 percent, beyond any reasonable doubt — that a crime was committed. If we cannot establish that, then we can’t bring a criminal case.

But we don’t let these institutions go. We’ve brought civil cases. We’ve brought regulatory cases. And the entire approach here is to have a multi-pronged, comprehensive approach to what gave rise to the financial crisis.

[www.pbs.org: The legal response to the crisis]

NARRATOR: In April 2010, Goldman Sachs CEO Lloyd Blankfein was summoned to the Hill by Senator Carl Levin.

PROTESTERS: [at hearing] If Martha Stewart can go to jail, so can Blankfein!

NARRATOR: This would be the biggest showdown between Congress and a major Wall Street banker.

PROTESTERS: Not too big to go to jail!

MARTIN SMITH: Blankfein was unapologetic.

LLOYD BLANKFEIN: Clients know our activities and they understand what market making is.

Sen. CARL LEVIN (D), Michigan: Do you think they know that you think something is a piece of crap when you sell it to them and then bet against it? You think they know that?

LLOYD BLANKFEIN: The nature of the principal business and market making—

TED KAUFMAN (D-DE), United States Senator 2009-10: Lloyd Blankfein argued it was perfectly OK, that “At the same time we were selling securities to you, we were betting on the fact these securities were going to go down. But that’s OK because we’re a market maker and we’re allowed to do that.” That sounds like fraud to me.

[at hearing] In the first half of 2007, Goldman Sachs sold long-position CDOs to its clients, right?

LLOYD BLANKFEIN: We sold— we reduced our risk.

Sen. TED KAUFMAN: So you were selling CDOs at the same time you were taking short positions on the same CDOs?

LLOYD BLANKFEIN: The best way of reducing your risk is to sell what you have.

Sen. CARL LEVIN: I believe in a free market. But if it’s going to be truly free, it cannot be designed for just a few people. It must be free of deception. It’s got to be free of conflicts of interest. It needs a cop on the beat, and it’s got to get back on Wall Street. We stand adjourned.

NARRATOR: Senator Levin referred his committee’s findings to Justice, but again, the department declined to bring any criminal charges.

JEFF CONNAUGHTON, Author, The Payoff: No one going to jail, no individuals being held accountable for anything other than relatively paltry fines.

MARTIN SMITH: The Justice Department says these are very difficult cases to bring. Showing intent and proving every step of the crime beyond a reasonable doubt is a difficult thing to do.

JEFF CONNAUGHTON: I think that is without a doubt a factor in the difficulty of proving intent. But I’m sorry, I just don’t believe there was enough effort. It just doesn’t make common sense. And so you’re telling me that not one banker, not one executive on Wall Street, not one player in this entire financial crisis committed provable fraud? I mean, I just don’t believe that.

NARRATOR: Kaufman and Connaughton were running out of patience.

MARTIN SMITH: I’ve talked to Senator Kaufman. I’ve talked to Senator Grassley. I’ve talked to staffers. I’ve talked to a number of people. They told us that they felt that you didn’t make this a top priority.

LANNY BREUER: Well, I’m sorry if they think that because I made it an incredibly top priority. But when we can’t bring a case, we have a— we have an ethical obligation not to bring those cases. But it’s not for lack of trying. Our lawyers are working incredibly hard, and it’s a disservice for anyone to suggest otherwise.

[www.pbs.org: More from Lanny Breuer]

MARTIN SMITH: In all of this, was there a case that you thought could have gone forward as a criminal prosecution that didn’t?

KEVIN PERKINS, Associate Deputy Director, FBI: You know, there were a lot of discussions along those lines. You know, I talked to Lanny when I was in the Criminal Division, you know, daily.

MARTIN SMITH: Did you argue with him?

KEVIN PERKINS: Yes. And we would argue this back and forth. And then we— but when we finally came to a decision, sometimes I would be frustrated. Sometimes I would be disappointed.

MARTIN SMITH: You always accepted the decision?

KEVIN PERKINS: But I accepted it.

MARTIN SMITH: As a professional, you accepted it.

KEVIN PERKINS: As a professional, I accepted—

MARTIN SMITH: But did you—

KEVIN PERKINS: —it.

MARTIN SMITH: —accept it as a citizen?

KEVIN PERKINS: Well, that’s— I mean, that’s— that’s a bit different because as a citizen, I would hope that something would happen to them, somehow, some way.

NARRATOR: FRONTLINE spoke to two former high-level Justice Department prosecutors who served in the Criminal Division under Lanny Breuer. In their opinion, Breuer was overly fearful of losing.

MARTIN SMITH: We spoke to a couple of sources from within the Criminal Division, and they reported that when it came to Wall Street, there were no investigations going on. There were no subpoenas, no document reviews, no wiretaps.

LANNY BREUER: Well, I don’t know who you spoke with because we have looked hard at the very types of matters that you’re talking about.

MARTIN SMITH: These sources said that at the weekly indictment approval meetings that there was no case ever mentioned that was even close to indicting Wall Street for financial crimes.

LANNY BREUER: Well, Martin, if you look at what we and the U.S. attorney community did, I think you have to take a step back. Over the last couple of years, we have convicted Raj Rajaratnam. Now, you’ll say that’s an insider trading case, but it’s clearly going after Wall Street. We—

MARTIN SMITH: But it has nothing to do with the financial crisis, the meltdown, the packaging of bad mortgages that led to the collapse, that led to the recession.

LANNY BREUER: Well, first of all, I think that the financial crisis, Martin, is multi-faceted. And what we’ve had is a multi-pronged, multi-faceted response. And it’s simply a fiction to say that where crimes were committed, we didn’t pursue the cases. And that’s why, where crimes were committed, you have more people in jail today for securities fraud, bank fraud and the like than ever before.

MARTIN SMITH: But no Wall Street executives.

LANNY BREUER: No Wall Street executives.

NARRATOR: By September 2010, Senator Kaufman’s term was nearing its end. Before leaving, he held a second oversight hearing.

Sen. TED KAUFMAN: Criminals on Wall Street must be held to account.

JEFF CONNAUGHTON: Ted decided he wanted to have a second hearing before he left office so that he could question Breuer, Perkins and Khuzami.

Sen. TED KAUFMAN: We’re now nearing the final quarter of 2010 without the sort of prosecutions that I fully expected we would hope to see by this time.

MARTIN SMITH: What was the thinking, I mean, if you can recount any conversations that you had with Senator Kaufman about, you know, “Let’s pull these guys back into the room”?

JEFF CONNAUGHTON: From our perspective, it was a big mystery. You know, we really believed that there was sufficient evidence of fraud, that there should have been some cases.

[www.pbs.org: Watch on line]

Sen. CHARLES GRASSLEY (R), Iowa: If heads don’t roll, nobody makes any changes.

I’m disappointed that in all of the wrongdoing that went on and all the fraud that went on, that there wasn’t an effort to go after bigger fish than the evidence shows they went after.

LANNY BREUER: I think many times, you have very sophisticated parties on both sides of these—-

JEFF CONNAUGHTON: Mr. Breuer basically kept his testimony at the level of generalities.

LANNY BREUER: You know, where the right balance is—

JEFF CONNAUGHTON: And I was sitting there behind the senator, thinking, “You’re dancing around the central question. Did the Department undertake a purposeful, concerted, timely investigation of higher-level Wall Street executives?”

LANNY BREUER: For very complicated cases, there are lots of different issues—

JEFF CONNAUGHTON: And at that point, I just began to feel like, “OK, I feel like I’m being gamed here.”

LANNY BREUER: They take time. They take the review of—

JEFF CONNAUGHTON: Not only was no one going to be held to account for the financial crisis, but — and I don’t say this lightly — no one was being held to account for the failure to hold Wall Street to account.

I really think this was a stain on the American justice system, and I did not want to be an accomplice to that. So I packed my bags, sold my house, and left town the day Ted Kaufman’s term was over. I mean, I literally was driving down I-95 the day he left office.

NEWSCASTER: JPMorgan reported a 47 percent increase in income….

NARRATOR: Meanwhile, a freelance journalist and blogger named Teri Buhl was sipping cocktails in Connecticut.

TERI BUHL, Investigative reporter: I was actually at a fund-raiser in Greenwich, and I met a man running for Congress. And he told me about a documentary filmmaker, Nick Verbitsky, who had been collecting a lot of interviews from Bear Stearns employees.

EMPLOYEE: [“Confidence Game”] So I go out and I find a borrower, and I lend this borrower $100,000—

NICK VERBITSKY, Director, Confidence Game: I actually had a friend who put me in touch with a couple a people who ended up in the film, people that worked at EMC Mortgage, which was Bears’s mortgage conduit, was really the factory floor of their entire mortgage operation.

EMPLOYEE: [“Confidence Game”] The problem with due diligence is it’s very costly.

TERI BUHL: We went through about three to four hours of multiple whistleblower tape detailing a massive fraud at the highest level inside of Bear Stearns against its own clients.

NARRATOR: Buhl wrote a story for The Atlantic Monthly’s Web site featuring two Bear Stearns insiders Verbitsky had interviewed.

TERI BUHL: And the first call I got after that story came out was from a few lawyers that wanted to meet our whistleblowers. And they were representing a group of mortgage insurers called monolines.

MARTIN SMITH: What did they tell you?

TERI BUHL: They told us that they were working on a massive fraud suit against Bear Stearns and that it’s critical that our whistleblowers help build their case.

NARRATOR: The lawyers worked at the New York firm Patterson Belknap Webb & Tyler. They were suing Bear Stearns and its successor, JPMorgan Chase, on behalf of companies that had insured the quality of the loans Bear was selling. In January of 2011, they filed a 161-page complaint.

MARK PALMER, Financial analyst: And within 160 pages, that document essentially summed up what looks to be the core of the credit crisis.

NARRATOR: Mark Palmer has pored through the Bear Stearns lawsuit and a dozen other private suits now pending against other Wall Street banks for fraudulently misrepresenting the mortgages they packaged and sold.

MARTIN SMITH: You say this is the core of the credit crisis.

MARK PALMER: I believe so. Based on what we’ve seen thus far, frankly, I think there’s some pretty decent evidence that the mortgage securitization industry was rotten to the core.

MARTIN SMITH: Do you think the government should have brought criminal cases against these players?

MARK PALMER: I would find it difficult to believe that there wasn’t sufficient evidence to at least indict many of the players involved here.

NARRATOR: In building their cases, attorneys at Patterson Belknap spoke to over 35 whistleblowers, many of them due diligence supervisors and underwriters. Among them, Tom Leonard.

MARTIN SMITH: It was Patterson Belknap that first got in touch with you about this.

TOM LEONARD: Yes. Yes.

NARRATOR: Leonard told the lawyers how due diligence was compromised.

MARTIN SMITH: And you told the truth to them about what you had seen.

TOM LEONARD: Yes, sir.

MARTIN SMITH: And you were a supervisor.

TOM LEONARD: Yes.

MARTIN SMITH: And you saw what your— your underwriters were doing.

TOM LEONARD: Yes.

MARTIN SMITH: And you saw the instructions—

TOM LEONARD: Yes.

MARTIN SMITH: —coming down from the banks.

TOM LEONARD: Yes.

MARTIN SMITH: What was the highest defect rate you ever saw on a job?

TOM LEONARD: Oh, gosh. We had a job that was, like, 50 percent. But then the word came down, everything got renegotiated and redone and—

MARTIN SMITH: In other words, you would come into a job, you’d find 50 percent of the loans were defective, but then the standards would be loosened so that you could qualify those loans—

TOM LEONARD: Right.

MARTIN SMITH: —and mark them as not defective.

TOM LEONARD: Right.

MARTIN SMITH: Isn’t that fraudulent?

TOM LEONARD: Yes.

MARTIN SMITH: Is this something you think is important for the government now to be prosecuting, the kind of fraud that you saw?

TOM LEONARD: Yeah. I mean, it’s— if it’s still within the statute of limitations…

MARTIN SMITH: The Department of Justice says that it’s very hard to prosecute these kinds of crimes because you have to prove criminal intent.

TOM LEONARD: Yes, sir.

MARTIN SMITH: How do you respond to that?

TOM LEONARD: I think if I was sitting on the jury and I saw this information that I could pretty well assure myself that there’d been criminal intent.

MARTIN SMITH: Were you ever contacted by anybody in law enforcement or the Justice Department?

TOM LEONARD: Not until just recently.

ERIC SCHNEIDERMAN, Attorney General, NY: We are going to step up on the principle of one set of rules for everyone, equal justice under law—

NARRATOR: Finally, in late 2012, the State of New York sued a Wall Street bank for fraudulently misrepresenting the mortgages they packaged and sold.

ERIC SCHNEIDERMAN: Very simply, we’re investigating the misconduct of folks who caused the bubble—

NARRATOR: The man who brought the suit was New York Attorney General Eric Schneiderman, co-chair of a new state-federal working group that included the Department of Justice, the SEC and others.

ERIC SCHNEIDERMAN: —securities fraud against JPMorgan Chase, as successors to Bear Stearns and Company and EMC Mortgage Corporation.

NARRATOR: Although the case centered on bankers’ fraudulent and deceptive practices, no individuals were named. The suit was a civil, not criminal case.

MARTIN SMITH: You’ve alleged in the case of Bear Stearns that they passed these things on knowingly, intentionally, knowing they were bad?

ERIC SCHNEIDERMAN (D), Attorney General, NY: Yes. We think the facts as alleged in our complaints make it very hard to conclude that by 2006 and 2007, the folks at these banks did not know what was going on, and that they were putting more and more bad loans into these securities.

MARTIN SMITH: I guess I still don’t understand. If this was so clear and so intentional and so many commissions and hearings brought this forward, why is this taking so long?

ERIC SCHNEIDERMAN: You know, it’s— it’s hard for me to address the specifics of what happened before I got here. Believe me, we’ve moved as fast as we could. You have to ask others about what happened before then.

MARTIN SMITH: What gave you the confidence that you would have results, given that the government had gone for three years with really very little to show?

ERIC SCHNEIDERMAN: We were able to do some work more quickly by subpoenaing the records of private parties that had brought actions.

MARTIN SMITH: You were drawn to the work of a private law firm, Patterson Belknap.

ERIC SCHNEIDERMAN: Oh.

MARTIN SMITH: Eric Haas and his team of attorneys at Patterson Belknap.

ERIC SCHNEIDERMAN: Well, we had— when we started our investigation, we took a look at what other complaints had been filed. And there were a whole series of private complaints that had been brought, and Patterson Belknap had brought a couple of those cases.

MARTIN SMITH: The complaint that was filed by New York Attorney General Schneiderman was based largely on work done by private law firms, work that goes back several years. What does that tell us about the work that the Justice Department was doing all this time?

GEOFF MOULTON, Chief Counsel, Sen. Ted Kaufman, 2009-10: I do think— I think it’s unusual for— but not unprecedented for the Justice Department to sort of follow onto the work of private litigants. But it does raise the question, you know, why didn’t the government develop it first?

MARTIN SMITH: That’s a real question—

GEOFF MOULTON: It is.

MARTIN SMITH: —given all the pushing that you were doing and Senator Kauffman was doing.

GEOFF MOULTON: I think— yeah, I think it’s an absolutely fair question to ask.

NARRATOR: Attorney David Boies, whose firm has represented both banks and plaintiffs suing financial institutions, has also reviewed Schneiderman’s complaint.

MARTIN SMITH: Schneiderman is bringing a civil case alleging fraud.

DAVID BOIES, Boies, Schiller & Flexner: Yes.

MARTIN SMITH: Couldn’t it be filed as a criminal case?

DAVID BOIES: I think that if you took every allegation that’s made in Schneiderman’s complaint and you accepted that as true and believe that you could prove that beyond a reasonable doubt, that could have been filed as a criminal case.

NARRATOR: Filmmaker Nick Verbitsky was finally contacted by the Justice Department this past August about the whistleblowers he found for his film about Bear Stearns. It had been more than a year since those lawyers at Patterson Belknap first called him.

NICK VERBITSKY: I think, you know, the ease with which I found these people and the things that they were telling me, you know, it wouldn’t have taken a lot of effort on the part of a regulatory entity in Washington to have done this.

I’m an independent filmmaker. You know, I’m not a financial regulator. I’m not somebody who’s running the SEC. It’s, like, you know, “What have you guys been doing? What have you been looking at?” I mean, I went out and found these people myself and— you know, in my spare time, basically, you know, and— and it— it was work, but it wasn’t that hard.

MARTIN SMITH: We have been able to contact a number of people who were inside the banks, doing due diligence work as contractors, who all told us that they were never contacted by the Justice Department.

LANNY BREUER: Well, look, I— I can’t talk in general about— nondescript, anonymous whistleblowers. But here’s what I can tell you. Whenever I personally have been in any public setting, I’ve invited whistleblowers to come forward.

MARTIN SMITH: But it shouldn’t be so easy for journalists to go out and find whistleblowers that, at this point, four years after the meltdown, that haven’t been contacted by Justice.

LANNY BREUER: Martin, I don’t accept—

MARTIN SMITH: No?

LANNY BREUER: I don’t accept for one moment that you all are finding whistleblowers that we’re not. What I do— let me continue— what I do believe is that when we speak to the whistleblowers, we have to make a determination whether what they say is really a criminal case.

MARTIN SMITH: We’ve talked to whistleblowers, we’ve talked to people inside the banks who’ve told me, “Yes, there was fraud that went on.”

KEVIN PERKINS, Associate Deputy Director, FBI: And we’ve talked to hundreds and hundreds and hundreds of people in these investigations.

MARTIN SMITH: And you’re saying in not one of those cases— having interviewed hundreds of people and looked at these things, you can’t find one person in this whole mess that you can establish beyond a reasonable doubt that was selling these things knowingly, intentionally, and defrauded the investors.

KEVIN PERKINS: We were not able to reach a level of— that would sustain beyond a reasonable doubt. We were not able to show criminal intent sufficiently enough to obtain what we believe— to obtain a conviction of a criminal—

MARTIN SMITH: Do you think the banks did all this unintentionally?

KEVIN PERKINS: No, I personally don’t. But in the end, sure, I was frustrated. Lanny was frustrated. Lanny was disappointed. I’m sure he was. And so was I. But we knew professionally this was the decision that needed to be made.

LANNY BREUER: The jobs of tens of thousands of employees can literally be at stake.

NARRATOR: In a September 2012 speech, Lanny Breuer gave a speech explaining his reluctance to indict a major bank.

LANNY BREUER: — the kinds of considerations in white collar cases that literally keep me up at night.

MARTIN SMITH: You gave a speech before the New York Bar Association. And in that speech, you made a reference to losing sleep at night, worrying about what a lawsuit might result in at a large financial institution.

LANNY BREUER: Right.

MARTIN SMITH: Is that really the job of a prosecutor, to worry about anything other than simply pursuing justice?

LANNY BREUER: Well, I think I am pursuing justice. And I think the entire responsibility of the department is to pursue justice. But in any given case, I think I and prosecutors around the country, being responsible, should speak to regulators, should speak to experts, because if I bring a case against institution A, and as a result of bringing that case, there’s some huge economic effect — if it creates a ripple effect so that suddenly, counterparties and other financial institutions or other companies that had nothing to do with this are affected badly — it’s a factor we need to know and understand.

TED KAUFMAN: That was very disturbing to me, very disturbing. That was never raised at any time during any of our discussions. That is not the job of a prosecutor, to worry about the health of the banks, in my opinion. Job of the prosecutors is to prosecute criminal behavior. It’s not to lie awake at night and kind of decide the future of the banks.

MARTIN SMITH: So is Wall Street breathing a sigh of relief?

DAVID BOIES: I don’t think people are breathing a sigh of relief, given the— the level of other litigation that’s out there. However, I think there are probably a lot of individuals who have breathed sighs of relief over the last two or three years.

NARRATOR: So far, in civil proceedings, the government has levied several billion dollars in penalties for misconduct in a crisis that’s cost investors and homeowners many hundreds of billions of dollars.

But to date, not one senior Wall Street executive has been held criminally liable by the Department of Justice for activities related to the financial crisis.