Did the Fed’s Emergency Lending Prop Up “Too Big to Fail”?

May 1, 2012

Share

The Obama administration arrived in Washington in early 2009 facing the worst financial crisis since the Great Depression — and an American public outraged by bailouts for the financial institutions that had gotten them there.

To build confidence in the banking system, Treasury Secretary Timothy Geithner, the man tasked with the economic turnaround, hinged his plan on what were called “stress tests” to determine the biggest banks’ fiscal health and, if necessary, provide “capital support” to those that were the most in trouble.

On May 7, the results were in: The nation’s 19 largest banks were fundamentally healthy, the administration announced, and would soon repay the loans they had taken.

For more than a year, many of these same banks had turned repeatedly to the Federal Reserve to tap a vast reservoir of cash in order to keep their daily operations from freezing up.

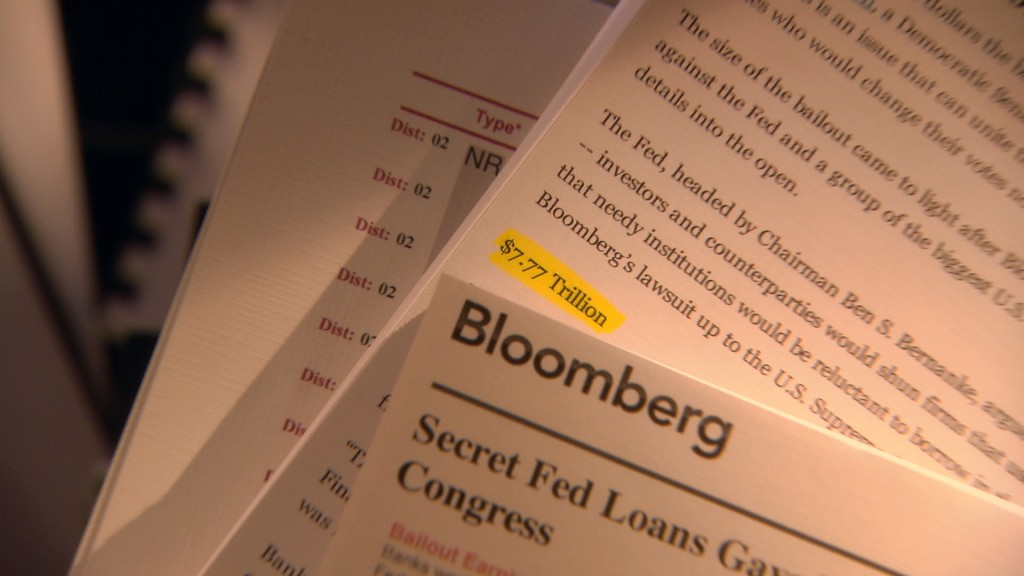

“Wall Street was in much deeper trouble than we ever imagined.” — Bob Ivry, Bloomberg NewsLate last year, Bloomberg News broke the story of the Fed’s unprecedented intervention in the financial markets — under which it made trillions of dollars in loans, commitments and guarantees to financial institutions around the world. After two years of legal wrangling, the news organization obtained thousands of pages of documents, which revealed critical details about the emergency lending, including how much money went to which banks, when and at what interest rates.

What Did the Documents Reveal?

“What we found out, really, was that Wall Street was in much deeper trouble than we ever imagined,” Bob Ivry, one of the Bloomberg reporters investigating the loans, told FRONTLINE. In a series of reports, Bloomberg laid out three main calculations:

- $1.2 trillion: The amount the Fed loaned to banks on Dec. 5, 2008, the “peak lending day” or single neediest day for banks that year;

- $7.77 trillion: The total amount the Fed either lent, spent or committed “to rescuing the financial system” as of March 2009;

- $13 billion: The estimated net interest margin banks made “by taking advantage of the Fed’s below-market rates.”

Bloomberg says these amounts “dwarfed” the amounts lent to the same banks through TARP — the $700 billion the Bush administration had secured from Congress to help alleviate the crisis. Citigroup, for example, received $45 billion in TARP funds, as compared with $99.5 billion it had borrowed from the Fed on its peak lending day, according to Bloomberg.

“Congress had no idea that these banks were having such trouble,” Ivry told FRONTLINE, noting that the loans came while bank CEOs were assuring Congress — which was in the midst of a debate over whether to regulate and even break up the banks — that they were in good shape. The secrecy, Bloomberg asserts, “helped preserve a broken status quo and enabled the biggest banks to grow even bigger.”

The Dispute

The Fed disputes Bloomberg’s accounting. In a letter (PDF) from chairman Ben Bernanke to Congress, the Fed said that all of its outstanding loans never totaled more than $1.5 trillion and that nearly all of them had been fully repaid or were “on track to be fully repaid.” The letter questioned the calculations and argued that most of its lending was priced at a penalty over normal market interests rates.

The Fed also defended not immediately disclosing some details about the loans. “Releasing the names of these institutions in real-time, in the midst of the financial crisis,” the letter states, “would have seriously undermined the effectiveness of the emergency lending and the confidence of investors and borrowers.”

Bloomberg has stood by its reporting, issuing a point-by-point response to the Fed’s letter and releasing its spreadsheets of the data on its website.

Regardless of the precise amount the Fed lent to banks during the crisis, many analysts agree it was significant. The number “was huge, whatever it was,” Wall Street super-lawyer Rodgin Cohen told FRONTLINE.

So Did the Lending Work?

Cohen and a number of other Wall Street and Washington insiders told FRONTLINE that the Fed’s emergency lending program helped restore confidence in the financial system and prevent a greater crisis.

“[The Fed] did what they were supposed to do.” — Wall St. super-lawyer Rodgin Cohen“This is an area where I think it’s easy to criticize, but I think when you understand what is the role of the central bank,” Cohen said, “they did what they were supposed to do.”

But Phil Angelides, who headed the Financial Crisis Inquiry Commission (FCIC), warns that Americans paid a “dear price” for the Fed’s and the government’s other loans to banks. “It also precluded us from moving forward and asking the people of this country to make the kind of investments to stabilize the housing market, to help homeowners, to create jobs that [were] necessary in the wake of this crisis,” he told FRONTLINE.

Richard Fisher, the president of the Dallas Federal Reserve, says the problem was not that the Fed made was making “very large loans during the crisis,” but that financial institutions were able to grow so large they developed a “stranglehold” on our economy. “This is why we should not be put in a position where a few institutions are so dominant that we run that risk in the first place,” he told FRONTLINE.

“If we don’t do something about ‘too big to fail,’ first we lessen the efficiency of our economy. Monetary policy cannot operate with the efficiency with which we would like to operate,” Fisher added. “We place those that are of lesser size at a competitive disadvantage. We undermine the sense of confidence that people need to have to make capitalism work. And we exacerbate extreme views that are suspicious of whether or not the system is rigged.”

Dig Deeper

Bloomberg’s Reporting: Read the original story, the outlet’s response to the Fed and an explanation of how it crunched the numbers. Also explore this interactive graphic of the lending and download data Bloomberg aggregated of daily borrowing totals for 407 banks and companies that used the Fed’s emergency lending programs during the financial crisis.

The Fed’s Response: Read Ben Benanke’s letter to Congress (PDF).

The FRONTLINE Interviews: Read more analysis from our interviews with key players about how much the Fed lent, whether the loans were effective and what the role of transparency should be going forward.

Related Documentaries

Latest Documentaries

Related Stories

Money, Power and Wall Street

Related Stories

Money, Power and Wall Street

Explore

Policies

Teacher Center

![]()

Jon and Jo Ann Hagler on behalf of the Jon L. Hagler Foundation

Corey David Sauer

Koo and Patricia Yuen

FRONTLINE is a registered trademark of WGBH Educational Foundation. Web Site Copyright ©1995-2025 WGBH Educational Foundation. PBS is a 501(c)(3) not-for-profit organization.

Funding for FRONTLINE is provided through the support of PBS viewers and by the Corporation for Public Broadcasting, with major support from Ford Foundation, and Fialkow Family Foundation. Additional funding is provided the Abrams Foundation, Park Foundation, John D. and Catherine T. MacArthur Foundation, Heising-Simons Foundation, and the FRONTLINE Trust, with major support from Jon and Jo Ann Hagler on behalf of the Jon L. Hagler Foundation, and Corey David Sauer, and additional support from Koo and Patricia Yuen. FRONTLINE is a registered trademark of WGBH Educational Foundation. Web Site Copyright ©1995-2026 WGBH Educational Foundation. PBS is a 501(c)(3) not-for-profit organization.