From Bear to Lehman: Documents Reveal an Alternate History

May 1, 2012

Share

On the heels of investment bank Bear Stearns’ sudden collapse in March of 2008, the New York Federal Reserve Bank, then led by President Timothy Geithner, and the Securities and Exchange Commission (SEC) dispatched teams of investigators to the four largest remaining investment banks: Lehman Brothers, Merrill Lynch, Goldman Sachs and Morgan Stanley.

Though it was not these firms’ main regulator, the New York Fed’s task was to monitor the health of each and assess whether any firm faced a similar risk of ruin that could reverberate throughout the financial markets.

But less than six months later, Lehman Brothers suffered a similar fate as Bear Stearns — this time without a government bailout. Its demise sent credit markets spiraling into disarray and caused shock waves throughout the global financial system.

So did the government fail to anticipate the systemic risks posed by Lehman Brothers? And why wasn’t more done to save Lehman Brothers?

Regulators, including Geithner, who would later become Treasury secretary, claim they did the best they could with the information that they had at the time. But FRONTLINE interviews with key officials and documents, including internal Federal Reserve Bank of New York emails, reveal another side to the story: a trail of missed warnings and evidence that regulators declined to pursue information that might have helped them to understand the systemic risk posed by Lehman.

“One of the most striking parts of the story is that, first of all, how little people in charge of our system knew and/or did in the wake of the oncoming crisis,” Phil Angelides, Chairman of the Financial Crisis Inquiry Commission (FCIC) set up by Congress to investigate the causes of the crash told FRONTLINE. “Secondly, once the evidence was clear, that the system itself was shaky and unsound, how there wasn’t definitive and strong action to try to curb what was becoming a disaster for the country.”

Early Signs: “$15 BILLION SHORT”

After Bear’s collapse, the New York Fed wanted to know how the remaining banks would react if they experienced a run similar to Bear. A major source of trouble had been the firm’s reliance on the repo market—the market used by banks to take out short-term loans that are used to finance their operations. A loss of confidence in Bear had caused a run on the bank by both its repo lenders and derivatives counterparties, quickly resulting in the bank running out of cash. The idea was to use stress tests to screen each bank against possible Bear-like scenarios in order to assess their vulnerability to a similar loss of confidence by creditors and investors.

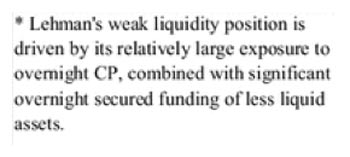

The results of the liquidity stress tests showed trouble. Tests done in May of 2008 showed Lehman would be $84 billion short of cash in the “Bear Stearns” scenario, and $15 billion short when tested against the less stringent “Bear Stearns Light.” A month later, yet another liquidity stress test by the Fed showed Lehman $15 billion short on necessary cash to survive a loss of funding similar to Bear’s.

According to the FCIC, these “less liquid assets” included devalued mortgage-related securities – instruments that had worried the New York Fed since prior to Bear’s collapse. Despite the results of the Fed’s tests, it appears that nothing was done. An exhaustive review by Anton R. Valukas, the court-appointed Lehman Bankruptcy Examiner, noted (PDF) that it was not apparent “that any agency required any action of Lehman in response to the results of the stress testing.”

Lehman ran its own stress tests in June using the same Bear-like scenario and released results to the New York Fed and SEC claiming that they had passed with over $13 billion in “excess cash.”

Then-Assistant Treasury Secretary Michele Davis told FRONTLINE that regulators knew Lehman was in danger, but said that they lacked the authority to directly intervene to save them. She argued that it was a difficult time to ask Congress for additional authority, so they had to resort to using what power they had to instill confidence in the system:

The American people expect the federal government to have the authority to prevent a disaster when they can see it coming. And we don’t have that authority. And they didn’t want to stand up and blast that message from the rooftops every day, because it would just scare people… All we could do was work … cooperatively and try to figure out ways to use existing authority to provide more confidence.

Then-Treasury Secretary Henry Paulson did indirectly intervene, though. According to Bethany McLean and Joe Nocera’s book on the crisis, Paulson began in March 2008 to push Lehman’s CEO Dick Fuld to raise additional liquidity or find a buyer for the firm, but Fuld had seemed reluctant.

Flawed Calculations

According to the Financial Times, following Lehman’s March 2008 publication of its first quarter financial health, Merrill Lynch alerted both the New York Fed and the SEC that Lehman’s assertions about the health of its liquidity pool were likely exaggerated by improper calculations.

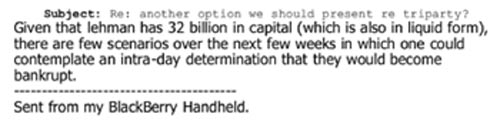

But in July 2008, four months after Merrill Lynch officials say they warned regulators of Lehman’s inflated liquidity figures, one New York Fed regulator still cited Lehman’s reported available liquidity pool whle debating colleagues on the likelihood of a bankruptcy:

The Lehman Bankruptcy Examiner later corroborated Merrill’s warnings when the report concluded that assets on Lehman’s books were misrepresented in order to inflate the firm’s balance sheet and maintain market confidence: “Lehman publicly asserted throughout 2008 that it had a liquidity pool sufficient to weather any foreseeable economic downturn. But Lehman did not publicly disclose that by June 2008 significant components of its reported liquidity pool had become difficult to monetize.”

By Sept. 12, two days after Lehman reported it had a $40 billion liquidity pool, the firm’s available pool was actually less than $2 billion in assets that could be quickly converted to cash needed to pay the firm’s debts.

Reluctant to Investigate

In August 2008, New York Fed emails show regulators were concerned over Lehman’s involvement in the over-the-counter derivatives market – an unregulated and opaque market filled with complicated financial instruments — but were reluctant to push for the information needed to shed light on the risks inherent in Lehman’s role in that market.

On Aug. 8, 2008, Pat Parkinson, then an economist at the New York Fed, sent an email to Treasury and New York Fed regulators with a “game plan” to assess Lehman’s over-the-counter derivatives positions, which could “entail systemic risk”:

Despite the known dangers of over-the-counter derivatives, subsequent emails showed a reluctance within the New York Fed to ask Lehman for more information about the instruments. Officials feared that asking for details could unsettle already rattled markets by shaking confidence in Lehman.

One New York Fed regulator noted that “to really get into possibilities, you would need to request master agreements [of OTC derivatives]” which would “be a huge negative signal”:

While debating whether regulators should formulate a “default management group” made up of senior business representatives to help foresee dangers posed by Lehman and the other investment banks, another regulator questioned: “If we ask, will we see anything in time to deal with some of the immediate issues that concern us? And by asking, are we signaling concerns that only exacerbate the issues?”

“You would think that the people who were in charge of our financial system would have a grip on the key risks that were in it,” Phil Angelides, chairman of the Financial Crisis Inquiry Commission, told FRONTLINE. “And if they did, they would have moved in a sense to get a handle on those. In a sense they had to deliberately turn a blind eye to those problems.”

Days Before the Collapse: “Spiraling Out of Control”

In early September, during the days leading up to Lehman’s bankruptcy, internal New York Federal Reserve Bank emails show that there may have been a lack of understanding of the pending consequences of Lehman’s collapse.

Documents indicate that Timothy Geithner was struggling to grasp the risks posed by Lehman just a week before its demise.

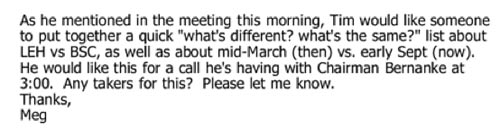

On Sept. 9, 2008, almost 6 months after the collapse of Bear, Geithner asked New York Fed staff to put together a “what’s different? what’s the same?” document comparing Lehman and Bear Stearns as Lehman’s stock prices plunged following news that negotiations with a likely investor, Korea Investment Bank, had ended unsuccessfully.

Michele Davis, who worked closely with Henry Paulson throughout the crisis, told FRONTLINE that around this time Paulson was also beginning to gather more information. He called CEOs on Wall Street, who told him that the markets were prepared for Lehman’s possible demise. “The feedback generally speaking was everyone’s known about this problem for a long time. It’s not like Bear Stearns. It’s not suddenly upon us and it’s too late to do anything,” she said. “So, you know, people should be well prepared for this, or at least, if not well prepared, semi-prepared for it.”

Meanwhile, documents show that regulators at the New York Fed were hearing a different message from Wall Street.

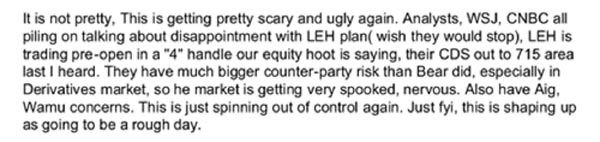

Goldman Sachs executive Susan McCabe wrote an email to William Dudley, Vice President of the Markets Group at New York Fed, on Sept. 11, 2008 that the market had become nervous about a Lehman bankruptcy. “It is not pretty, this is getting pretty scary and ugly again,” she wrote.

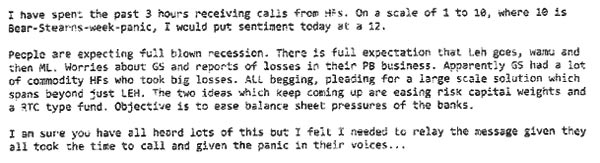

After receiving calls from hedge fund mangers (referred to as ‘HFs’ in the document below), Haley Boesky of the New York Fed wrote an email that “on a scale of 1 to 10, where 10 is Bear-Stearns-week-panic, I would put sentiment today at a 12. People are expecting a full blown recession.” (The term PB used below refers to Goldman’s Prime Brokerage Business, which provides services to hedge funds.)

The Decision Not to Save Lehman: “Can’t Stomach A Bailout”

Despite warnings of the dangers of a Lehman collapse, there would be no government bailout.

In the early morning hours of Sept. 14, 2008, Lehman filed for bankruptcy. Treasury and Fed officials say they worked furiously to find a buyer for Lehman in the week leading up to the firm’s collapse, but after last minute hopes of deals with Barclay’s and Bank of America were quashed, Tim Geithner was quoted as having warned officials at the Federal Reserve Bank of New York that it was time to spray “foam on the runway” and prepare to cushion the blow from Lehman’s fall.

Regulators have since argued that there was no authority to save Lehman, and that a calculation was made that Lehman’s investors had adequate time to prepare for the firm’s failure.

“The failure of Lehman posed risks. But the troubles at Lehman had been well known for some time, and investors clearly recognized—as evidenced, for example, by the high cost of insuring Lehman’s debt in the market for credit default swaps—that the failure of the firm was a significant possibility,” Ben Bernanke told the House Financial Services Committee. “This, we judged that investors and counterparties had had time to take precautionary measures.”

Documents show that there was also a discussion about the policy effects and political implications of a Lehman bailout at both the Treasury and Federal Reserve Bank of New York.

Jim Wilkinson, then-Treasury Chief of Staff under Henry Paulson, indicated his reluctance to bail out Lehman because of how the bailout would play in the press. In a Sept. 8, 2008 email to then-Assistant Secretary of Treasury Michele Davis, Wilkinson wrote:

On Sept. 10, 2008, Senior Vice President of the New York Fed Patricia Mosser shared her thoughts on how to resolve the Lehman situation, again noting that the consequences of moral hazard — the idea that a bailout could lead other firms to expect a similar treatment — would outweigh those of a bankruptcy (PDF):

Michele Davis says that Henry Paulson and officials at Treasury were consumed with trying to find a solution, but had little time to react without the necessary authority. “You had this outpouring of stuff from the Hill of: ‘No bailouts. No government money. No nothing,'” she said. “The politics were, as we get closer and closer to an election, I don’t think you could have found a worse time in the political cycle to have a financial crisis.”

But critics say that the government could and should have saved Lehman Brothers in order to prevent the systemic consequences of its collapse. After all, only days later the government bailed out investment giant AIG.

“We looked at all the facts and what we really found was, there was a decision to let Lehman go,” Angelides said of the FCIC’s investigation. “They undersized the effect of letting Lehman go down. … We determined that they made it on the basis that they couldn’t find a buyer and had doubts about whether they really could, absent a buyer, save Lehman… It was a decision to let Lehman go for a variety of reasons, political, financial — their sense of the market.”

Related Documentaries

Latest Documentaries

Related Stories

Money, Power and Wall Street

Related Stories

Money, Power and Wall Street

Explore

Policies

Teacher Center

![]()

Jon and Jo Ann Hagler on behalf of the Jon L. Hagler Foundation

Corey David Sauer

Koo and Patricia Yuen

FRONTLINE is a registered trademark of WGBH Educational Foundation. Web Site Copyright ©1995-2025 WGBH Educational Foundation. PBS is a 501(c)(3) not-for-profit organization.

Funding for FRONTLINE is provided through the support of PBS viewers and by the Corporation for Public Broadcasting, with major support from Ford Foundation, and Fialkow Family Foundation. Additional funding is provided the Abrams Foundation, Park Foundation, John D. and Catherine T. MacArthur Foundation, Heising-Simons Foundation, and the FRONTLINE Trust, with major support from Jon and Jo Ann Hagler on behalf of the Jon L. Hagler Foundation, and Corey David Sauer, and additional support from Koo and Patricia Yuen. FRONTLINE is a registered trademark of WGBH Educational Foundation. Web Site Copyright ©1995-2026 WGBH Educational Foundation. PBS is a 501(c)(3) not-for-profit organization.