Neil Barofsky on the “Broken Promises” of the Bank Bailouts

August 1, 2012

Share

“By any objective standards, the Trouble Asset Relief Program [TARP] has worked,” the Treasury Department wrote in a July progress report (PDF) on the $700 billion program that Congress authorized in 2008. “It helped stop widespread financial panic, it helped prevent what could have been a devastating collapse of our financial system, and it did so at a cost that is far less than what most people expected at the time the law was passed.”

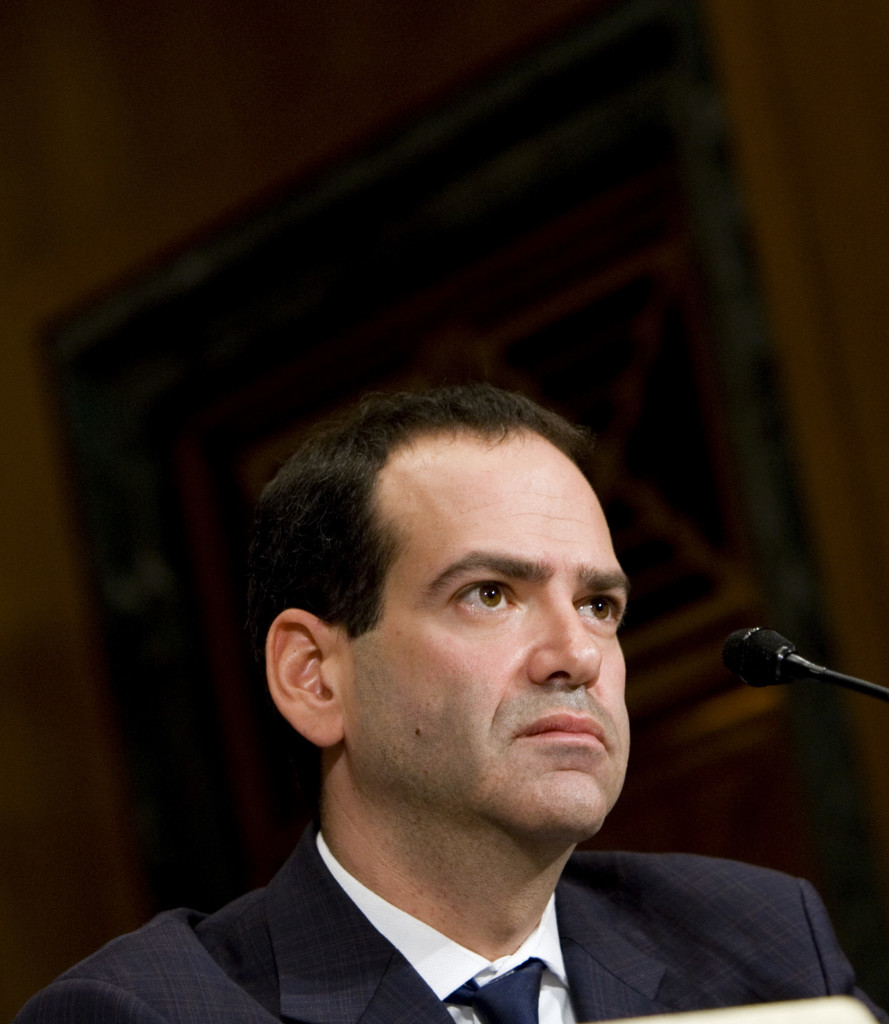

Neil Barofsky sees it much differently. From December 2008 to March 2011, Barofsky, a formal federal prosecutor and lifelong Democrat, served as special inspector general of TARP, charged with protecting against abuse and fraud in the program. In his new book about that experience, Bailout, he writes that the American people “should be enraged by the broken promises to Main Street and the unending protection of Wall Street.”

FRONTLINE spoke with Barofsky, now a senior fellow at New York University School of Law, about his time policing TARP. This is an edited transcript of that conversation:

You are highly critical of the management of TARP. What went wrong?

It’s important to remember that there were a number of different objectives for TARP. It did meet one of its primary objectives, which was to help prevent the entire collapse of our financial system. … The other goals, which have more of a focus on helping Main Street institutions and individuals and businesses definitely small enough to fail — those goals all came short.

So, for example, TARP was supposed to be used by the banks to restore lending, help pump that oxygen into the lifeblood of the economy, and it just didn’t happen. One of the reasons why it didn’t happen is the money went to the banks with no strings attached, no conditions, no incentives, just essentially piles of money given to them without any instructions whatsoever and sort of this hope that somehow or other they use the money to achieve the policy goals of the administration. Of course, that never happened and you just look at the malaise the economy has been in in the years ever since.

Similarly, TARP was supposed to help homeowners, and that was part of the very bargain that was struck in order to get TARP passed. … We had a housing program that was an utter failure by any definition if you look at what its original goal was — up to 4 million homeowners helped, and today it’s around 800,000, 20 percent of that goal. Or if you look at how much money has been spent, just a small tiny fraction, maybe 6 percent of the original $50 billion, on par with what credit card companies got.

So you’re sort of left here, almost four years after the bailout, with this tremendous amount of effort and money going to save the banks but all the other goals, really important Main Street goals to help everyone else, just abandoned.

What do you say, though, to those who argue that while the bailouts may not be popular, they did stabilize the banks, as well as the auto sector, for far less money than first feared?

It’s undoubtedly good news that the losses are less than we originally intended. … But again, even the saving, or stabilizing the financial system — to what end? What we’ve done is essentially preserve a fundamentally broken status quo that led to the financial crisis in 2008, and we took a lot of problems in the system and in some ways made them worse.

One of your biggest disappointments was with the Home Affordable Modification Program (HAMP). That was an effort to help people stay in their homes. Why did it fall short?

It was cursed from the beginning. As I detailed in the book, it was rushed out before they were ready. I had [a meeting] in February, on a Friday, where I was told they were weeks away from having anything to announce, and then that same night I heard the president was announcing the program in a few days, and they never really caught up. The put the program on backs of mortgage servicers who never had the infrastructure in place to run the program …

“Tim Geithner is as much the symptom of the disease as the actual disease.”Fundamentally, though, the program was cursed by a lack of commitment by Treasury to use the program to help homeowners as opposed to another way of bailing out the banks. When Secretary Geithner told a group of us in 2009 when he was pressed on how this program [was] ever going to help homeowners, he portrayed what the program was really about. He said that the program was going to “foam the runaway” for the banks. He mentioned that the banks could handle a certain number of millions of foreclosures over certain periods of time and that this would help. In essence what we took that comment [to mean] was this was going to help extend out the foreclosure crisis for the benefit of the banks. They wouldn’t be hit with all of that at the same time.

Unfortunately the way Treasury ran the program, that foam was really supplied by the bodies of wrecked homeowners who may have provided a soft landing for the banks, but got absolutely crushed under the weight of this broken program.

Are there any aspects of TARP you do consider a success?

It’s a counter-factual. People say, “Oh we could have been fine without it.” I mean, we’ll never know for sure, but I do know based on my time down there that just about everyone was pretty strongly convinced that this could have been an epic Great Depression had we not done this.

I think that’s an accomplishment. I think the execution of it, though, was absolutely horrible and shortsighted and so focused on the banks with such little focus on everyone else that we’re feeling the results of that, and ultimately it may end up setting the groundwork for an even bigger financial crisis in the future.

Your book is just as much about dysfunction in Washington as it is about TARP. What did you find are the implications of that dysfunction when it comes to effective oversight?

It’s pretty hopeless. Unless you recognize the flaws of our system and how fundamentally broken our system of regulation is, it’s going to remain hopeless. …

Fundamentally we have, on the one hand, the corrupting influence of the megabanks, which have to be broken up. They have such a corrupting influence because of the power, their size, their economic might and also because of the corruption of ideology because of the revolving door. So many of the Treasury officials come from the Wall Street banks they’re supposedly regulating. So that’s part of the fundamental problem.

On the Washington side, in addition to that, you have the problems of regulators who often have incentives not to be really good regulators. The curse there again is partly the revolving door. I was told point blank in 2010 that if I didn’t change the harshness of my tone on Wall Street, as well as on the administration, that I was going to be doing me and my family real harm because I wasn’t going to have this job forever. If I wanted to get a job on Wall Street or advance within the administration, I needed to soften my tone. I was told that if I did soften my tone, very good things could potentially [follow].

I obviously didn’t take that advice, as this book clearly demonstrates, but that’s the decision that’s facing a lot of our regulators. You either have people who made their millions on Wall Street and come into government … or you have folks who look at their bosses who made that money and want to be them. And the path to being like that is rarely by being a tough, effective regulator. It’s by rolling with the punches — rolling over, really, and pulling your punches and trying to get that big job. That’s not to say that all regulators do that but that’s our incentives and we need to change the incentive structure for regulators.

You had a rocky relationship with Treasury Secretary Tim Geithner. One of your criticisms of him is also one that emerged in our film, Money, Power and Wall Street: that he was too close to the banks. In your view, was he then, and is he still, the right man for the job?

First of all, this gets lost sometimes: Tim Geithner is as much the symptom of the disease as the actual disease. And he is just yet another example of a captured government official who, because of fundamentally flawed ideology, puts the interest of Wall Street and a handful of banks over that of Main Street and the broader economy. But he’s not alone. He’s far from alone.

Do I think he did a good job as Treasury secretary? No. I think he did a horrible job as Treasury secretary. Again, all you have to do is look at where we are as an economy and look how TARP was essentially hijacked by the interests of Wall Street and failed to fulfill Main Street. The fact that he believed that HAMP was more about helping the banks than it was helping homeowners should have been disqualifying for that job, in my view.

His behavior today is entirely consistent with that broken ideology. He’s the head of a Financial Stability Oversight Council that has done absolutely nothing to rein in the power of the giant banks. There’s been no effort to break them up. He led the effort against a bipartisan Senate effort in 2010 that would have broken up the banks and limited their power. At every critical juncture, he’s chosen the side of the banks over that of homeowners and Main Street, so I don’t think he’s done a good job and I don’t think he should still be there.

You wrote “Dodd-Frank may have inadvertently sowed the seeds for the next financial crisis.” How so?

If you look at some of the different causes of the last financial crisis, to me a lot of it comes back to the incentives and perversions of the market and normal capitalism that comes with the presumption of “too big to fail.”

Too big to fail, and by that I mean the presumption of bailouts, the market’s general presumption that if one of these large banks gets into trouble again — or got into trouble beforehand, it was certainly alive and well before the crisis — the government would bail them out. That results in a complete perversion of capitalism, and what it does is it creates incentives for these large institutions and their executives to pile on risk. It’s a very simple “Heads I win, tails the taxpayer bails me out,” and it creates incentives for short-term profits, short-term bonuses, and the collection of risk in different areas. And ultimately the bigger the bank, the bigger the incentives are for that risk, and the bigger the danger is and the need for bailout if they get into trouble lest they bring down the entire financial system.

“[Megabanks] don’t operate by the regular rules because they know, and the regulators know, that any type of severe punishment against them will never happen.”All you have to do is look at the recent headlines and see that those problems are very, very much still alive, and appear to be getting worse. Because on the one hand you see it through the recent $6 billion loss for JPMorgan Chase, where again, capitalizing and profiting off the government guarantee. They took hundreds of billions of dollars of deposits backed by the United States government and made incredibly risky bets that blew up. That’s a direct function of too big to fail.

Similarly, you look at the different scandals, whether it’s LIBOR, whether it’s HSBC ignoring money-laundering laws, whether it’s Citi’s recent settlement … these are all symptoms of the banks that are also too big to jail. They don’t operate by the regular rules because they know and the regulators know that any type of severe punishment against them will never happen because if you indict one of these banks, again you risk bringing down the entire financial system with them and that puts them above the law. They play by a different set of rules, so you have this combination of incentives to take risks and this complete lack of accountability because of their size and it’s a toxic cocktail. We saw it with Fannie and Freddie. We saw it with the too-big-to-fail banks in 2008, and I’m sorry it’s just the height of foolishness to think you leave those fundamental incentives in place and think we’re not going to have a repeat and another financial crisis.

What kind of reforms would make you feel safe about the health of the financial system?

It’s very simple. You have to remove the presumption in the market that the banks are too big to fail, which means that they don’t play by a different set of rules any more.

I think there are a lot of potential things that can be done. Breaking up the banks, whether it’s through re-enactment of Glass-Steagall, which is a good idea, whether it’s through size caps, which was the basis of the SAFE Act, which was proposed by Senators [Sherrod] Brown (D-Ohio) and [Ted] Kaufman (D-Del.), which had bipartisan support before it was defeated by Geithner and the administration, that’s a good idea. Remarkably higher capital levels, not the levels that are currently under discussion, but maybe two times that. Really, really going after the problem of leverage. That will help make the banks safer, make it so that it’s the shareholders and their executives who bear the losses, not the taxpayers, and take away some of the advantage. All those things are, I think, would be an important part of the necessary reforms.

Former Digital Editor

Related Documentaries

Latest Documentaries

Related Stories

Money, Power and Wall Street

Related Stories

Money, Power and Wall Street

Explore

Policies

Teacher Center

![]()

Jon and Jo Ann Hagler on behalf of the Jon L. Hagler Foundation

Corey David Sauer

Koo and Patricia Yuen

FRONTLINE is a registered trademark of WGBH Educational Foundation. Web Site Copyright ©1995-2025 WGBH Educational Foundation. PBS is a 501(c)(3) not-for-profit organization.

Funding for FRONTLINE is provided through the support of PBS viewers and by the Corporation for Public Broadcasting, with major support from Ford Foundation, and Fialkow Family Foundation. Additional funding is provided the Abrams Foundation, Park Foundation, John D. and Catherine T. MacArthur Foundation, Heising-Simons Foundation, and the FRONTLINE Trust, with major support from Jon and Jo Ann Hagler on behalf of the Jon L. Hagler Foundation, and Corey David Sauer, and additional support from Koo and Patricia Yuen. FRONTLINE is a registered trademark of WGBH Educational Foundation. Web Site Copyright ©1995-2026 WGBH Educational Foundation. PBS is a 501(c)(3) not-for-profit organization.