The Rules That Govern 501(c)(4)s

October 30, 2012

Share

Nearly a century ago, Congress created the complicated legal framework that governs these tax-exempt nonprofits, also known as 501(c)(4)s for the part of the tax code they fall under. That rule said they were supposed to operate “exclusively for the promotion of social welfare” — a definition that includes groups ranging from local fire departments to the Sierra Club to the National Right to Life Committee.

While these nonprofits have always been allowed to lobby for change, in 1959, regulators opened the door to political activity by interpreting “exclusively” to mean that groups had to be “primarily” engaged in social welfare and helping the community.

But regulators never defined exactly how they would measure this balance. Part of the reason, said Marcus Owens, a former head of the IRS division overseeing nonprofits, is because the IRS didn’t want to limit what it could evaluate in deciding what was political activity.

However, the lack of clarity has created a unique type of organization when it comes to politics — chief among those differences being what the public must be told about these nonprofits’ donors.

Why Don’t 501(c)(4)s Have to Disclose Their Donors?

Social welfare nonprofits don’t fall under the Federal Election Commission’s standard definition of a political committee, which, under FEC guidelines, must disclose its donors. Because 501(c)(4)s say their primary purpose is social welfare, they can keep their donors secret. The only exception is if someone gives them money and specifically states the funds are for a political ad.

And unlike political committees, social welfare nonprofits have a legal right to keep their donors secret. That stems from the landmark 1958 Supreme Court case, NAACP v. Alabama, which held the NAACP didn’t have to identify its members because disclosure could lead to harassment.

Fast forward to the post-Citizens United world of campaign finance where outside groups can now spend unlimited amounts of money to influence elections so long as they are independent of candidates. Seeing the advantages offered by groups that can engage in political activity while keeping their donors secret, both Democrats and Republicans have seized onto this opening in the tax code.

That’s why in recent years, many new 501(c)(4)s have popped up right before the election season, focusing heavily on television advertising, usually attacking, though sometimes promoting, candidates running for office.

These nonprofits do have to report some of their activities to the FEC. When they run ads directly advocating for the election or defeat of a candidate, they have to tell regulators how much and what they spend money on — but not where the money comes from.

Since they can’t make these types of ads their sole activity, many 501(c)(4)s focus on so-called issue ads, which they only have to report to the FEC in defined windows before an election.

The Debate Over “Issue Ads”

But what exactly defines an issue ad?

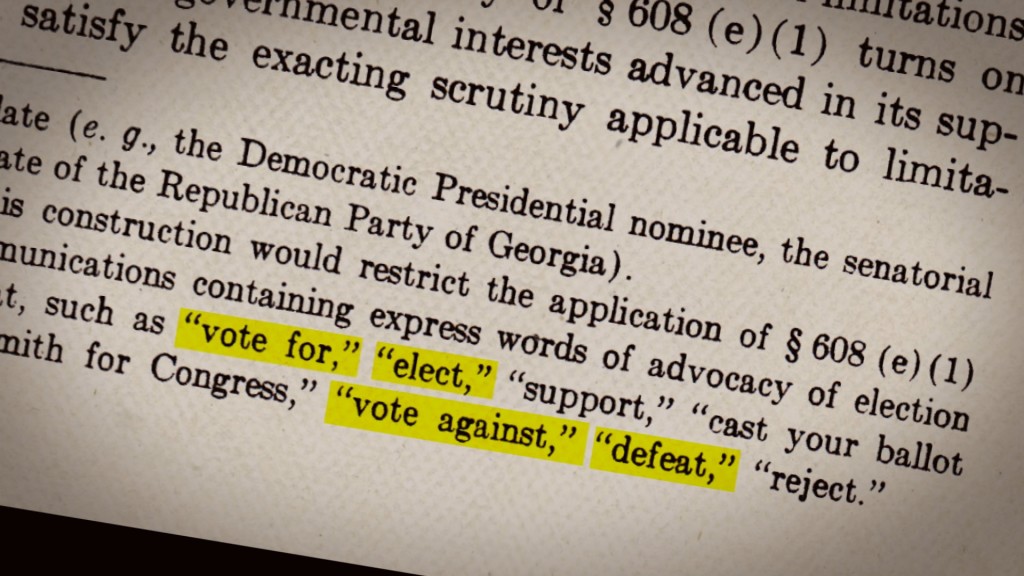

The key starting point is a 1976 Supreme Court case, Buckley v. Valeo, in which the court speculated in a footnote that if certain words were used in an ad, it was clearly a campaign ad. The eight phrases listed in the footnote –“vote for,” “elect,” “support,” “cast your ballot for,” “Smith for Congress,” “vote against,” “defeat,” and “reject” — became known as the “magic words” and for decades served as a bright line test between an issue ad and a campaign ad.

But many campaign finance reformers saw that distinction as a sham, especially as increasing amounts of federal campaign dollars headed to political parties where the soft money loophole allowed unlimited money to be spent on issue ads. While avoiding the magic words, these issue ads typically focused on one candidate running for office and ran just before an election. In other words, the reformers argued, they were clearly trying to influence elections.

The reformers tried to address this loophole in the Bipartisan Campaign Finance Reform Act of 2002, otherwise known as the McCain-Feingold bill. In a 2003 case, McConnell v. FEC, the Supreme Court appeared to agree, saying that the magic words were “functionally meaningless.”

But the decision didn’t bar states from using the magic words and the court has since backed away from its earlier stance. And so legal debate continues. For instance, earlier this year, the Colorado Supreme Court upheld the magic words test as the bright line between issue ads and direct campaign ads.

Today, both the FEC and the IRS use tests broader than just the magic words to determine what counts as an issue ad. The FEC says that any ad that mentions a candidate during defined windows before an election must be disclosed, even if it doesn’t include the magic words. The IRS looks at what it calls “the facts and circumstances” surrounding an ad. Tax experts say that many of the issue ads that fall outside FEC reporting windows would be considered political by the IRS.

But the reality on the ground for groups like 501(c)(4)s is less clear: Because three of the FEC commissioners sympathize with the magic words test they have “refused to apply the broader test in recent years,” says Paul Ryan, senior counsel at the Campaign Legal Center, a group that pushes for more campaign finance reforms.

And some outside groups are trying to keep it that way.

What that means for 501(c)(4)s is this: by avoiding the magic words, social welfare nonprofits have a better chance of convincing regulators they are focused on issues and not politics.

Of course, the IRS could revoke a nonprofit’s tax-exempt status if it engages in too much political activity. In practice, that hasn’t happened much. But the IRS has indicated it is starting to look into some of these groups and recently sent a letter (pdf) to Congress saying it had more than 70 “ongoing examinations” of 501(c)(4)s.

Whatever it does, the IRS remains limited in what it can do to watch over these groups. As a recent ProPublica investigation found: “One reason the IRS struggles is that it can’t match the speed of politics.” In other words, by the time these groups submit tax returns, they have often stopped operating or created new groups under new names.

Producer & Reporter

Related Documentaries

Latest Documentaries

Related Stories

Big Sky, Big Money

Related Stories

Big Sky, Big Money

Explore

Policies

Teacher Center

![]()

Jon and Jo Ann Hagler on behalf of the Jon L. Hagler Foundation

Corey David Sauer

Koo and Patricia Yuen

FRONTLINE is a registered trademark of WGBH Educational Foundation. Web Site Copyright ©1995-2025 WGBH Educational Foundation. PBS is a 501(c)(3) not-for-profit organization.

Funding for FRONTLINE is provided through the support of PBS viewers and by the Corporation for Public Broadcasting, with major support from Ford Foundation, and The Fialkow Family Foundation. Additional funding is provided the Abrams Foundation, Park Foundation, John D. and Catherine T. MacArthur Foundation, Heising-Simons Foundation, and the FRONTLINE Trust, with major support from Jon and Jo Ann Hagler on behalf of the Jon L. Hagler Foundation, and Corey David Sauer, and additional support from Koo and Patricia Yuen. FRONTLINE is a registered trademark of WGBH Educational Foundation. Web Site Copyright ©1995-2026 WGBH Educational Foundation. PBS is a 501(c)(3) not-for-profit organization.