REPORTED BY

Martin Smith

NARRATOR: This is a story about a bet that went bad. Like all stories about Wall Street, it starts with the pursuit of profits and the risks of getting it wrong.

It’s one of the latest in a stream of missteps, meltdowns and scandals that blow up, it seems, every few months.

NEWSCASTER: Two mortgage companies under government control—

NEWSCASTER: The Federal Reserve is bailing out Bear Stearns—

NARRATOR: It’s a familiar cycle. Customers are outraged. Lawmakers promise change.

NEWSCASTER: —are calling for tougher standards—

NARRATOR: Then it happens again.

NEWSCASTER: MF Global down almost 39 percent—

NEWSCASTER: An increasing number of investors are betting the stock has farther to fall—

WILLIAM D. COHAN, Author, Money & Power: Of all of the collapses that occurred during this financial crisis, the collapse of MF Global, in my mind, is the most egregious. This did not have to happen.

AZAM AHMED, The New York Times: It is a Wall Street morality tale, in some ways. How can something like this be allowed to happen? How can one individual completely shape the destiny of this firm, and ultimately, its demise?

NARRATOR: This is the story of Jon Corzine, the collapse of his company, and why no one stopped him until it was too late.

WILLIAM D. COHAN: He is a fiercely ambitious and an aggressive risk-taker. And that’s the part that never comes across when you talk to him in person. You get this sort of avuncular feeling that totally masks what is a highly aggressive and ambitious guy who takes these huge risks with other people’s money.

NARRATOR: Corzine had an impressive resume— a high school quarterback, a Marine, and then a rapid rise through the ranks at Goldman Sachs.

AARON LUCCHETTI, The Wall Street Journal: Corzine, importantly, grew up in the government bond trading business at Goldman Sachs, where he became such a star and well-respected figure there, he was able to make huge money off of moves in currencies and interest rates and bonds.

NARRATOR: By age 47, he was the youngest CEO in the company’s history. But his management style led to conflicts with another Goldman partner, Hank Paulson. In 1999, Corzine was ousted. It didn’t slow him down.

WILLIAM D. COHAN: Hank Paulson said to him, you know, “What are you going to do now, Jon?” And Corzine said, “Either I’m going to,” you know— you know, “have my own hedge fund and be worth billions, or I’m going to be president of the United States.”

NARRATOR: Corzine would aggressively embrace politics. In 2000, he spent a record $62 million of his own money to become a senator from New Jersey. In 2006, he spent another $43 million to become governor.

CLERGYMAN: Gracious God, we ask your blessing upon Jon, that you would fill him with positive vision that he might inspire others.

Vice Pres. JOE BIDEN: The reason why we call Jon is because we knew he knew about the custody.

NARRATOR: By 2008, Corzine had become a trusted adviser to Barack Obama. It was once rumored that he might even replace Tim Geithner as treasury secretary. But then in 2010, New Jersey voters ended his political career and returned him to Wall Street.

NEWSCASTER: Former New Jersey governor Jon Corzine is returning to the private sector—

NEWSCASTER: He has taken the helm of MF Global—

NARRATOR: But Corzine’s choice of MF Global was puzzling.

CHRISTOPHER WHALEN, Investment Banker: I think it was a little surprising that he went to such a small firm. You know, if you think about it, Goldman partner, Goldman CEO, confidante of the president of the United States, former New Jersey governor, senator— why wasn’t he running a bigger firm, I guess is the real question.

BETHANY McLEAN, Co-Author, All the Devils Are Here: Ninety-nine percent of people would look at his resume and say, “I was a senior partner at Goldman Sachs, I was the governor of New Jersey, I’m, you know, past 60, over and out, I’m going to— I’m going to go have fun.” But he looks at his resume and says, “I was kicked out of Goldman Sachs. I was kicked out of being the governor. I still have something to prove.”

WILLIAM COHAN: And he wanted to come back to Wall Street and prove that his partners had been wrong about getting rid of him at Goldman Sachs. And he was going to show them.

JON CORZINE, MF Global CEO: I’m really excited about the opportunity to lead MF Global.

RICH ILCZYSZYN, Former Broker, MF Global: I thought it was great. The stock price jumped, and Corzine was a dynamic character.

[www.pbs.org: Watch on line]

JON CORZINE: We’re going to work very hard to get the earnings back on track—

RICH ILCZYSZYN: From the military to Goldman Sachs to governor— I mean, I get it, you know? He’s going to have political connections. This is going to be great for the company, you know? So I was sipping the Kool-Aid at that time.

NARRATOR: MF Global was a well established commodities brokerage, a spin-off from the old British powerhouse Man Financial.

WILLIAM COHAN: It was basically a commodities and futures trading and investing firm. Clients would come there saying they want to make trades in the commodities industry or the futures industry, buy pork bellies, buy oil futures, buy gold futures, silver, you know, palladium, whatever it is.

AZAM AHMED, The New York Times: MF Global was basically the middleman in these transactions. You put in a trade through them, they put it in through the exchange. And they took a small commission for it.

NEWSCASTER: I’m looking at commodities right now, and basically, the price of wheat—

NARRATOR: Many of MF Global’s customers were from Main Street. Steve Meyers used MF Global to trade futures on behalf of scores of farmers and ranchers in the Midwest.

STEVE R. MEYERS, Grainbelt Commodities: Many people cleared through MF Global because they were the world’s largest. So it gives you some comfort in the fact that you’re always going to have that liquidity. You’re dealing with somebody that’s everywhere in the world.

NARRATOR: But when Corzine took over MF Global, the firm was in deep trouble. Revenue from commissions wasn’t covering expenses. The firm was losing money.

AARON LUCCHETTI, The Wall Street Journal: When Corzine first came in, the ratings agencies told him, “Look, you stepped into a firm that has a lot of problems, so you don’t have unlimited time.” The ratings on this firm are fairly low for a firm in its business, and the buy system moved them lower. And so that put more pressure on Corzine than he would have otherwise faced.

JON CORZINE: We’re transforming from sort of an old-line brokerage firm into an investment bank.

NARRATOR: Corzine set about cutting costs and replacing old-line traders with more aggressive hires from Goldman Sachs.

JON CORZINE: And we want to take an intermediate risk, a broker-dealer—

WILLIAM COHAN: He was going to bring in a new team. He was going to have it take more risk. They weren’t taking enough risk, he told me.

JON CORZINE: I do believe we can take more principal risk than some of the businesses that are involved.

WILLIAM COHAN: So he was swinging for the fences from day one.

JON CORZINE: —internally generated capital—

AARON LUCCHETTI: The message was, “We’re building an operation that can make a consistent profit through prop trading, taking bets.”

JON CORZINE: —and the proper deployment of your capital into the right places—

AARON LUCCHETTI: What didn’t come across to anyone until later was that Corzine himself was the chief trader and that he was making one very out-sized bet.

NEWSCASTER: Sovereign debt fears are spreading, and investors are just really worried that—

NARRATOR: It was a large proprietary bet on European government bonds—

NEWSCASTER: —downgrading Portugal’s credit rating—

NARRATOR: —betting that they were selling cheap and would go up in value.

NEWSCASTER: If there is some kind of disorderly default, they fear some kind of banking crisis would erupt in Europe—

AARON LUCCHETTI: Corzine sees this and says, “This is an opportunity. Europe will get this done. They’re not going let various parts of the euro zone default, fall off the edge.”

Prof. SIMON JOHNSON, Economist, M.I.T.: Jon Corzine was betting on a bailout. He was betting that the relatively risky parts of Europe would become less risky, not more risky.

NEWSCASTER: The fragile Greek government is at a stalemate, and the debt crisis—

WILLIAM COHAN: Jon Corzine has always been a gambling man. This is what he does. Why do scorpions sting? Because that’s what they do.

AARON LUCCHETTI: And so he bought billions of dollars worth of these bonds in a way that seemed to hearken back to his days at Goldman. He basically made a Goldman-sized bet at a firm that was only a sliver of Goldman Sachs.

NARRATOR: They were structured as large derivative deals that allowed MF Global to book profits immediately in order to right its balance sheet.

AZAM AHMED: The way that this particular thing was structured, it’s a really obscure and complicated transaction, where, essentially, you can book the profits on the front end.

AARON LUCCHETTI: When I make an investment, I have to wait to see how it turns out before I can book the profits. But the way these— these accounting rules worked, and they were— they were the way it was supposed to work— if you booked a trade in that way, you got the revenues right up front.

NARRATOR: As a result of these proprietary trades, MF Global for the first time in 18 months began to look healthy.

MARTIN SMITH, Correspondent: Were you aware of what the company was doing with the cash on hand that was in the proprietary accounts?

STEVE R. MEYERS, Grainbelt Commodities: Never. I never knew before that they could invest money in overseas markets or sovereign debt.

MARTIN SMITH: You had no knowledge that they were buying sovereign bonds.

STEVE R. MEYERS: Had I known that, I— I would have pulled out immediately.

AZAM AHMED: There was actually a debate internally at MF Global about whether to disclose this. And their auditors ultimately encouraged them, you know, “You guys have to tell people. This is a really sizable bet, and it is material. You need to let customers and shareholders know about this.”

NARRATOR: But they held off informing investors and customers for months.

AZAM AHMED: As it started to grow, people began getting increasingly uncomfortable with it. And some people would confront him and say, you know, “Jon, I don’t think having this much money bet in this particular way is a sound thing. The market could really react badly to it.”

And so it began to get contentious, and a lot of people, including one of the chief risk officers there, said, “Look, I— I can’t support this anymore. I don’t think this is a good bet.”

NARRATOR: Corzine continued his trades. But where was he getting the money?

CHRISTOPHER WHALEN: I don’t think he ever had enough capital to really support the strategy that he was taking. He was taking a lot more risk, much more complex trades, bigger numbers, but it’s still the same old firm. And that’s the problem. I think customer money was supporting a lot of this activity long before the firm failed.

NARRATOR: That is speculation. There is no clear evidence that customer money was used in the trades. But Corzine was using a financial strategy called internal repo — whereby a brokerage can borrow cash internally from another part of the firm.

In Washington, in the summer of 2011, regulators at the Commodity Futures Trading Commission, the CFTC, were debating whether to ban internal repo transactions.

AZAM AHMED: The CFTC was potentially going to say, “No more doing internal repo.” And for a lot of companies, it was an important way to certain operational needs. Corzine, you know, got wind of this, so he begins to lobby in Washington.

BART CHILTON, Commissioner, CFTC: Senator Corzine was one of the more prominent individuals who came in and told us what a drastic mistake it would be to curtail the use of these internal repurchasing agreements, and that they were doing everything appropriate with regard to these internal repos, and that we shouldn’t worry about them and that we shouldn’t touch them.

NARRATOR: Corzine visited the CFTC and met with commissioners on three different occasions.

BART CHILTON: He’s an impressive man and he made a good case. And when he told me that we were making a big mistake, it certainly put some doubt into my mind for a little bit there as to whether or not we were going down the right course. But certainly, somebody that had his stature was somebody who had, you know, added respect, in my view.

NARRATOR: The regulators backed off. Internal repos were not banned.

CHRISTOPHER WHALEN: When somebody can show up and just wave their hand and say that they’re the former governor of New Jersey and they worked for Goldman Sachs, and then show up and start lobbying the agency for even more leniency— I mean, what’s the point? We might as well not have the regulator.

NARRATOR: By mid-2011, with a pass from regulators, Corzine’s bet on European sovereign debt rose from $1.5 billion to $4 billion to over $6 billion. Finally, it was all too much.

AARON LUCCHETTI, The Wall Street Journal: The trades stopped happening in the summer of 2011 because, eventually, they were too big for the board and for the risk officers. And the message was, “Enough. Leave them at $6 billion. You can keep them, but don’t build them up any higher than that.”

NARRATOR: With no ability to continue his trades, profits plummeted. The news that MF Global could be in trouble hit The Wall Street Journal in the fall. The story was a blow Corzine could not withstand.

AARON LUCCHETTI: When we report that MF Global has a $6 billion position in European bonds, it was very concerning to the market and it set off the panic.

NEWSCASTER: MF Global absolutely getting annihilated here, down almost 39 percent.

NEWSCASTER: Moody’s has downgraded MF Global.

NEWSCASTER: The fear is that they could downgrade them—

NEWSCASTER: The stock is in real trouble right here—

MARTIN SMITH: So this is like a “What was he thinking” kind of deal.

AARON LUCCHETTI: I remember having a conversation with someone at MF Global when I first heard about the position. And so I said to the person, “Are we talking about millions or billions here?” And I’m— I thought it was millions because I didn’t— I had assumed that if it was that big, it would have been talked about a fair amount. And they said, “No, it’s billions.”

WILLIAM COHAN: I think people saw the magnitude of the bet that Corzine made on— on— and how leveraged it was on a little sliver of equity, and they said, “You know what? When you’re leveraged 40 to 1, you know, the value of the asset goes down, you know, 1 or 2 percent, you’ve wiped out your equity account.”

AZAM AHMED: Ultimately, the bet he took was extraordinarily large and was maybe more than an investment bank would take. I mean, if you’re at a Goldman Sachs and it’s a huge institution, it can weather the waves of the market like a big ship. He was in a rowboat doing the same sort of things, and it— you know, it— it just capsized.

NEWSCASTER: It has been a rough week for MF Global—

NEWSCASTER: The firm’s credit rating was cut to junk—

RICH ILCZYSZYN, Former Broker, MF Global: Customers were frantic. Nobody knew anything. You know, my reputation’s on the line, right? I’ve done this for 15 years, stellar record, never any problems, that kind of thing. And now people are going, “Well, what’s going on?”

[www.pbs.org: A broker’s story]

NARRATOR: Steve Meyers, who had over $5 million dollars of client money invested at MF Global, couldn’t get the money out.

STEVE R. MEYERS: I tried numerous times to phone my rep in Chicago, finding out later he had already left the ship. So I knew that— that we were in trouble at this point and nobody was going to look out for us.

NEWSCASTER: MF Global is said to be looking to seek a buyer within days—

NARRATOR: In a last-ditch effort to salvage the company, Corzine put MF Global up for sale.

NEWSCASTER: Does MF Global now need a white knight?

NARRATOR: It was then that auditors discovered customer money was missing.

AARON LUCCHETTI: It became clear that there was a big hole somewhere between $500 million and a billion dollars in MF Global’s customer accounts.

NEWSCASTER: Regulators are now saying that the shortfall is around $593 million—

AARON LUCCHETTI: At that point, MF Global was different than Lehman, it was different than AIG or any of the firms that failed because at this point, customer money was missing.

BETHANY McLEAN, Vanity Fair: The core rule of this business was this thing known as customer segregation of assets, meaning that the firm kept its money in assets and its customers’ money in assets separate. They weren’t supposed to get mixed up. Well, guess what? They did.

MARTIN SMITH, Correspondent: What we hear from some people close to MF Global is that the— we don’t know what happened to the customer money because the last days were too chaotic, was too much confusion. Do you buy that?

CHRISTOPHER WHALEN, Sr. Managing Director, Tangent Capital: No. In our industry, putting your hands on customer funds takes some deliberate actions. You have to make an active decision to convert those funds. And I think that’s what happened.

MARTIN SMITH: How much money is still missing?

CHRISTOPHER WHALEN: I think it’s a little over $1.5 billion. And it’s not missing, it’s at JPMorgan. I mean, we know where the money is.

NARRATOR: JPMorgan was MF Global’s banker. Investigators are now trying to determine if in those last desperate days, MF Global executives intentionally transferred customer money to JPMorgan to meet a margin call from the bank.

MARTIN SMITH: Is it legal for them to take the money from the customer account to meet their margin calls?

CHRISTOPHER WHALEN: No, definitely not.

MARTIN SMITH: I mean, that’s different than internal repo.

CHRISTOPHER WHALEN: It is different from internal repo, and I would argue it’s actually an act of fraud.

MARTIN SMITH: An act of fraud.

CHRISTOPHER WHALEN: Yes. I think it could be prosecuted.

[www.pbs.org: More on customer money]

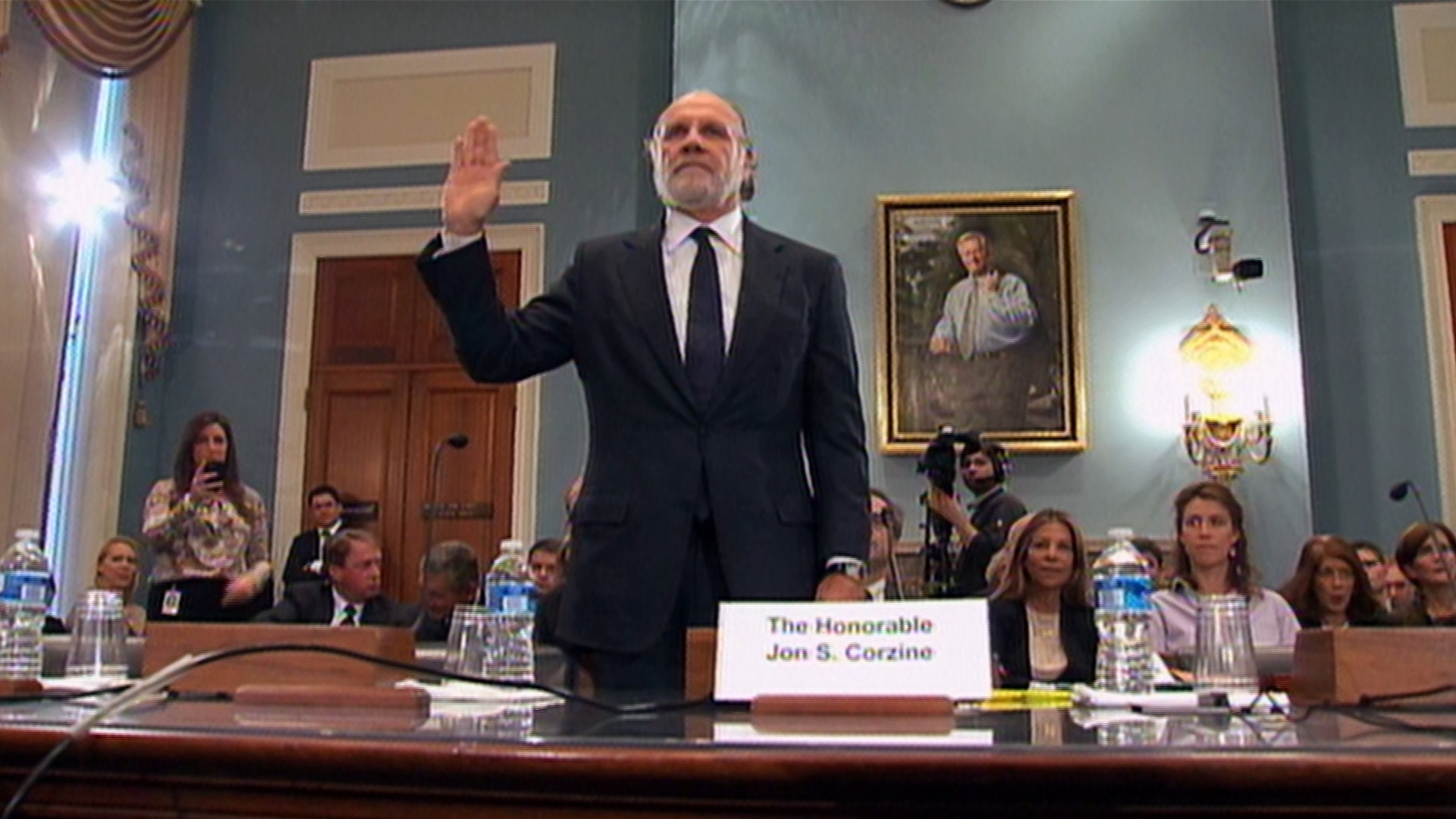

NARRATOR: Corzine says he did not order the transfers. But he insists he will cooperate with investigators to find out what happened.

COMMITTEE CHAIR: Do you solemnly swear that the testimony you are about to give before this committee is the truth, the whole truth—

NARRATOR: His only public comments came at Congressional hearings last December.

JON CORZINE: I remain deeply concerned about the impact that the unreconciled and frozen funds have on MF Global’s customers.

BART CHILTON, Commissioner, CFTC: This is a big bucket full of cold water in regulators’ face.

JON CORZINE: I simply do not know where the money is or why the accounts have not been reconciled to date.

BART CHILTON: It’s a wake-up call that says, “You’ve got to take a fresh look at what’s going on in the markets. You’ve got to better protect for customers’ interests. You’ve got to look at these guys because they’re always not going to be straight with you.”

Rep. COLLIN PETERSON (D-MN), Agriculture Committee: Who had the authority to move customer funds from segregated accounts?

JON CORZINE: Without looking at records, it’s very hard to try to reconstruct—

CONGRESSMAN: Did you authorize the transfer of funds from the segregated accounts to—

STEVE R. MEYERS: I blame all parties, everybody in power, whether it’s a politician, the regulators, Jon Corzine.

JON CORZINE: —people who handle the transfer of funds—

STEVE R. MEYERS: MF Global is just a microcosm, the tip of the iceberg, the cockroach theory, if you will. There’s never one cockroach. And it represents the start of systematic failure. The system has failed us, and it’ll only continue to grow.

NEWSCASTER: This is about Jon Corzine’s legacy, his firm, a lot of people invested in it because it had—

NARRATOR: The MF Global affair is unresolved. A half dozen investigations are under way, but so far, no one has been charged. The company has gone bankrupt.

Meanwhile, in December 2011, the CFTC finally banned internal repos.

BART CHILTON: The minute I saw the MF circumstance happen, I said, “We’ve got to pass that rule.” You know, enough is enough. You know, Monday morning quarterbacking would have had us do it months before. But that’s Monday morning quarterbacking.